StockResearch Intelligence Weekly #10

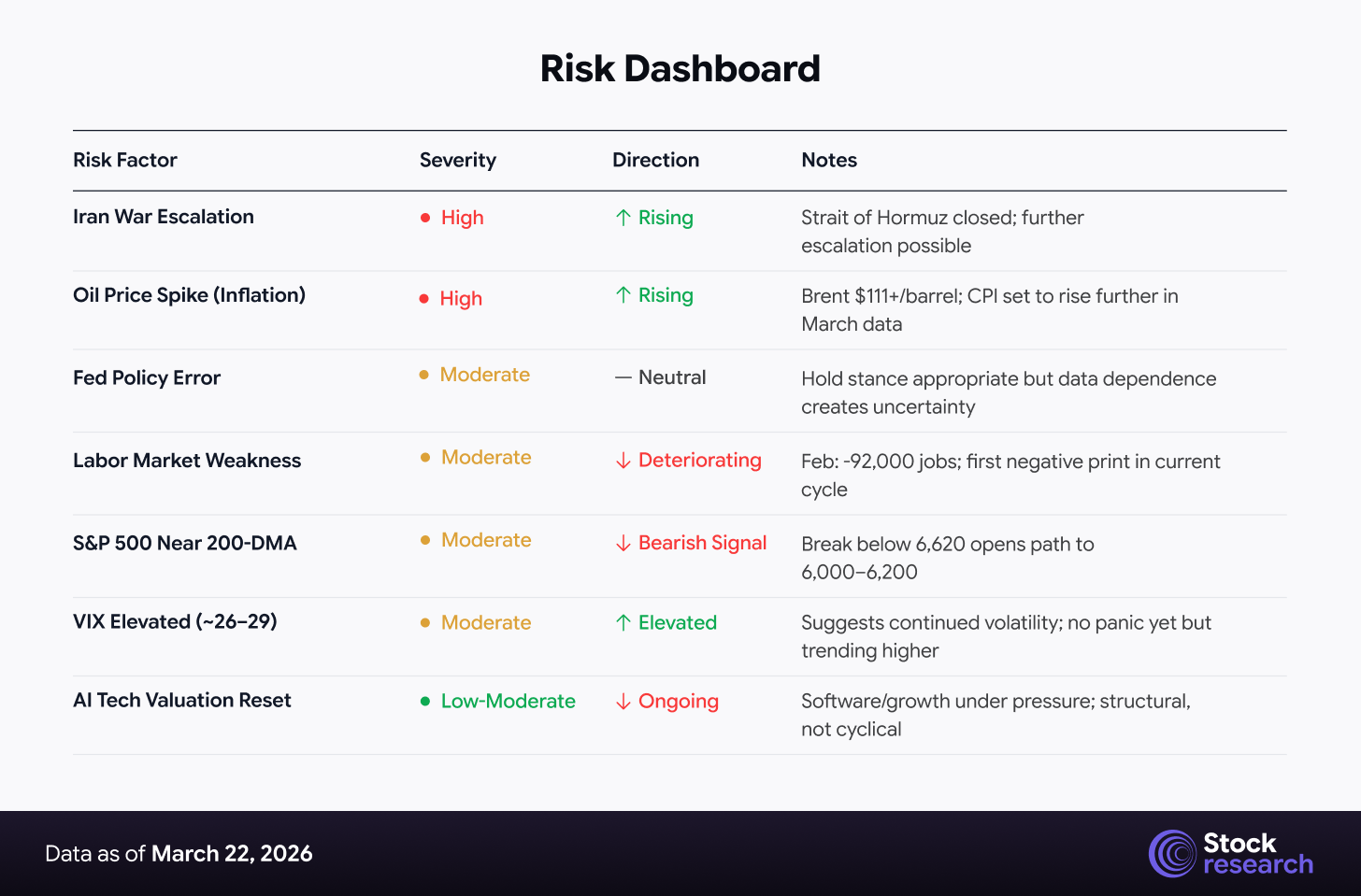

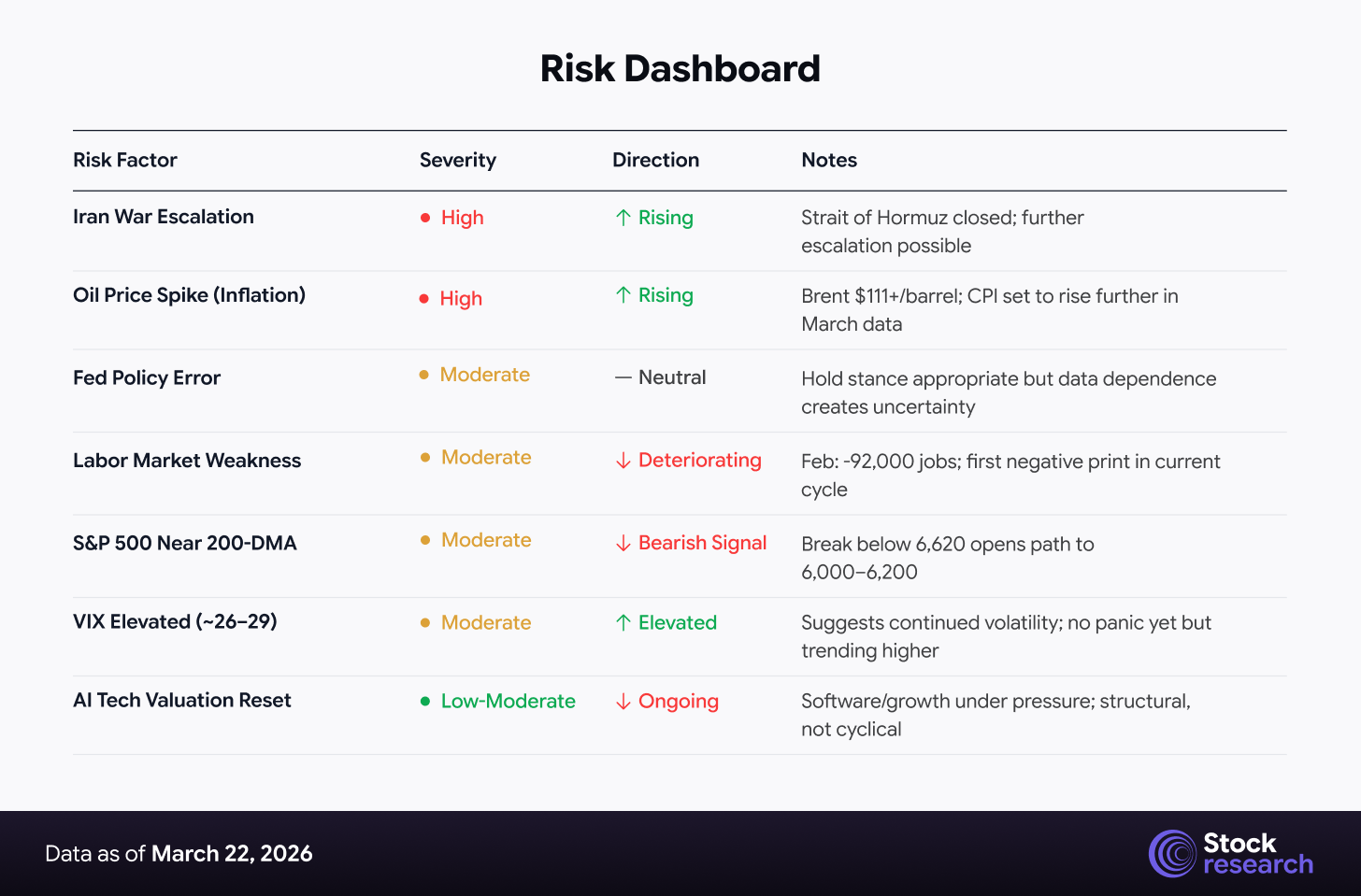

U.S. equities limped into the week ending March 22, 2026, as the Iran war, surging oil prices, and a cautious Federal Reserve combined to keep risk appetite on the defensive. The S&P 500 fell back toward the 6,500 level, logging a fourth straight weekly loss, while the Nasdaq and Dow also slipped and the VIX stayed elevated in the mid‑20s, signaling persistent stress rather than outright panic. What started as a sharp, jobs‑data‑driven break earlier in the month has now evolved into a grinding risk‑off tape, with investors forced to price not only a sustained energy shock and sticky inflation, but also a Fed that is reluctant to cut into geopolitical uncertainty and an AI trade that is rotating from high‑multiple software into cash‑generative energy and defense leaders.

Strengths

-

Energy and defense still providing a floor: The combination of Brent holding above 110 dollars and ongoing Iran‑related tensions kept energy and defense shares comparatively resilient, with cash‑generative oil majors and prime contractors absorbing some of the selling pressure hitting the broader indices.

-

Quality and cash‑flow leadership: Balance‑sheet strength, free‑cash‑flow visibility, and dividend support remained key differentiators, with high‑quality large caps in staples, healthcare, and select industrials outperforming high‑beta growth as investors prioritized durability over optionality.

-

AI infrastructure winners breaking away from generic tech: Within technology, names tied directly to AI infrastructure – memory, semis, and data‑center power – continued to show relative strength versus broad software, suggesting investors are refining AI exposure rather than abandoning the theme outright.

Weaknesses

-

Persistent stagflation overhang: The combination of elevated oil prices, a prior negative payrolls print, and a Fed that opted to hold rather than hint at imminent cuts kept stagflation fears front and center, limiting risk appetite even on days when indices attempted to bounce.

-

Broadening equity drawdown and fragile sentiment: The S&P 500’s fourth straight weekly loss, an elevated VIX in the mid‑20s, and renewed underperformance in small caps and cyclicals all pointed to a market that is shifting from a narrow tech correction to a more broad‑based de‑risking phase.

-

Policy and geopolitical tail‑risk still unresolved: With no clear path to de‑escalation in the Iran conflict and only cautious, data‑dependent messaging from the Fed, both the macro and geopolitical backdrop remain sources of downside tail‑risk, keeping high‑multiple growth, leveraged balance sheets, and long‑duration assets vulnerable to further de‑rating.

Market Recap

Sector Rotation in Focus

The defining theme of 2026 has been a dramatic rotation from growth to value, and the Iran war has only intensified it.

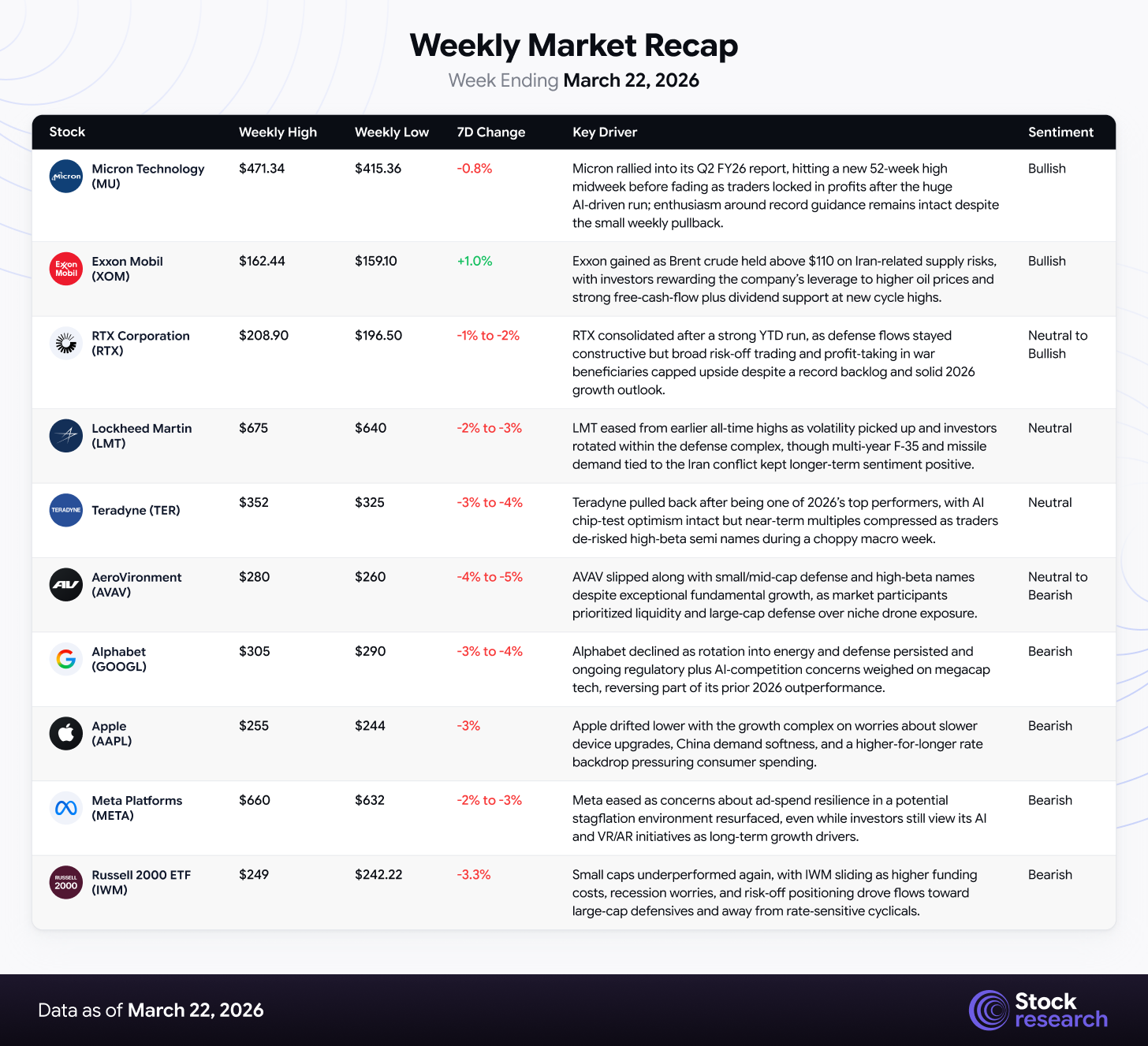

Energy (+32.8% YTD) remains the unchallenged sector leader, powered by oil price tailwinds from the Strait of Hormuz disruption. Defense (within Industrials) has surged as global military spending accelerates, Lockheed Martin hit an all-time high of $692 in early March, RTX’s backlog swelled to a record $268 billion, and Northrop Grumman gained +6% in a single session. Consumer staples outperformed consumer discretionary by nearly 15% YTD, reflecting the flight to defensives.

The tech and growth trade continues to unwind. Software stocks remain under heavy AI disruption pressure following the “Citrini Scare Trade” narrative, while the Nasdaq’s steep YTD decline reflects investor skepticism about premium valuations in a rising-rate, high-uncertainty environment.

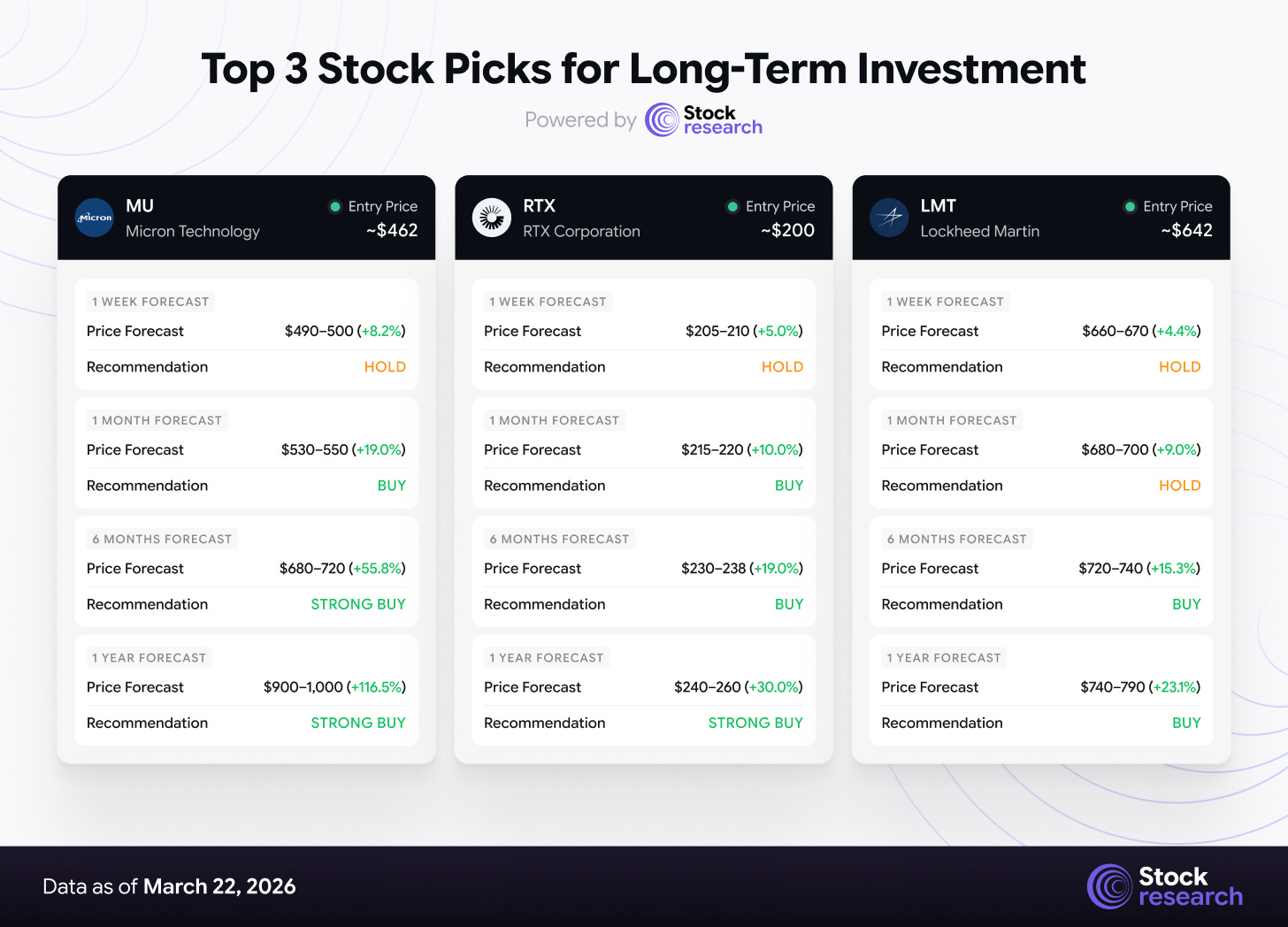

Top 3 Stock Picks for Long-Term Investment

Micron Technology (MU)

NASDAQ: MU | Sector: Semiconductors (Memory) | Theme: AI Memory Supercycle

Thesis: Micron is at the epicenter of the AI memory supercycle. The company just delivered the most explosive earnings beat in its history, Q2 FY2026 EPS of $12.20 versus the $8.79 consensus estimate (a 38.8% beat), with revenue of $23.86 billion (+196% YoY). More importantly, Q3 FY2026 guidance of $33.5 billion in revenue, nearly 47% above the $24.29 billion Wall Street consensus, signals that the HBM (High Bandwidth Memory) supercycle is accelerating, not peaking. Gross margin is guided at 81%, a level unprecedented in the company’s history.

The catalyst is structural: AI models are requiring exponentially more memory per compute cycle, driving a supply shortage across DRAM and NAND. Clients are committing to long-term data center capacity contracts, and Micron is investing over $25 billion in capex in FY2026 to meet the demand, with a new manufacturing facility expanding DRAM wafer output from H2 2027.

Key Risks: Cyclicality of the semiconductor industry; potential AI capex slowdown if macro deteriorates further; initial aftermarket stock drop (-5%) on capex increase announcement.

Analyst consensus: Average 12-month target $286–453 (pre-Q2 beat); post-guidance, high-end targets of $500–$1,200 have been published.

RTX Corporation (RTX)

NYSE: RTX | Sector: Aerospace & Defense | Theme: Defense Spending Surge / Iran War Beneficiary

Thesis: RTX (formerly Raytheon Technologies) is the premier diversified defense and aerospace play in the current geopolitical environment. With a record $268 billion backlog and surging demand from both the Iran conflict and the broader NATO and allied rearmament trend, RTX is a direct beneficiary of what is shaping up to be a multi-year defense spending supercycle. The company’s Raytheon defense division makes air and missile defense systems, precisely the hardware most in demand when adversaries are deploying ballistic missiles at Gulf infrastructure.

RTX is up approximately 38% YTD and was trading around $198–204 by the week’s close. Revenue forecasts for FY2026 stand at $94.29 billion (+6.41% YoY), while EPS is projected to surge 39.1% to $6.90 per share. Analyst consensus is a clear Buy, with Citigroup maintaining a $238 price target. The median analyst target stands at $225, implying ~10% upside from current levels even after the YTD run.

Key Risks: Diplomatic resolution to Iran conflict could trigger a sharp pullback in defense names; supply chain constraints on missile production; broader market selloff pressure.

Analyst range: $179–$240; Buy consensus from JPMorgan ($215), RBC Capital ($230), Citigroup ($238)

Lockheed Martin (LMT)

NYSE: LMT | Sector: Aerospace & Defense | Theme: Defense AI + Geopolitical Tailwind

Thesis: Lockheed Martin is the world’s largest defense contractor and the gold standard in high-technology military platforms. The Iran conflict has turbo-charged demand for its F-35 fighter jets, missile defense systems, and hypersonic weapons programs. LMT touched an all-time high of $692 on March 2, 2026 before pulling back with the broader market, now trading around $642, offering a potential re-entry opportunity after a 7% pullback from the ATH.

Truist upgraded LMT to Buy in January 2026 with a $605 target, citing improving program execution, declining estimated acquisition costs (EACs), and attractive valuation. At current levels, LMT trades at approximately 22x forward earnings, modest for a defense prime in a war cycle. The company’s $194 billion backlog provides years of revenue visibility, and Palantir’s recent defense AI contract wins, absorbing vacated Anthropic government contracts, may accelerate the Department of Defense’s integration of AI-enhanced platforms across Lockheed’s product suite.

Key Risks: Margin compression from fixed-price contracts if input costs rise further; political pressure on defense spending if conflict resolution is faster than expected; high absolute stock price creates entry friction.

Analyst consensus: Median $660, high $756; 12 Buy, 13 Hold, 1 Sell.

Low-Cap Stock Opportunities: Undiscovered Value

The following three stocks represent overlooked opportunities in the sub-$10 billion market cap space, each benefiting from structural tailwinds that the geopolitical shock has now amplified.

AeroVironment

NASDAQ: AVAV | Market Cap: ~$3–4B (Small-Mid Cap) | Sector: Defense Technology / Drones

Overview: AeroVironment is a pure-play drone and unmanned systems company that has been catapulted into the spotlight by the Iran conflict. The company designs and manufactures small unmanned aircraft systems (UAS), tactical missile systems, and high-altitude pseudo-satellite vehicles for the US military and allied governments.

Why Now: AeroVironment reported revenue of $472.5 million in its most recent quarter, a jaw-dropping 150.7% increase year-over-year. The drone warfare dimension of the Iran conflict has massively validated demand for AVAV’s product lines, including the Switchblade loitering munition and Puma AE reconnaissance drone. Cantor Fitzgerald recently described AVAV as having “the best growth outlook among small and mid-cap defense technology companies in approximately 20 years”, citing upcoming catalysts in drones, directed energy, and laser communications.

Valuation Angle: Despite the top-line explosion, AVAV has been trading well below analyst targets due to a brief EPS miss caused by upfront investment costs, not a structural issue. The stock was recently around $197–285, while the analyst consensus target is $305–378 and Needham holds a $450 price target. At the lower end of the range, AVAV offers a 54%+ potential upside to median analyst targets. Analyst sentiment: Strong Buy (8.6/10), 16 Buy, 2 Hold, 1 Sell.

Catalyst Ahead: Budget appropriation mechanics suggest significant near-term catalysts in drones, directed energy, and laser communications. FY2026 EPS guidance of $3.40–$3.55 reflects growing profitability as scale kicks in.

Teradyne

NASDAQ: TER | Market Cap: ~$20–25B (Mid-Cap) | Sector: Semiconductor Test Equipment

Overview: Teradyne makes automated test equipment (ATE) used to test semiconductor chips, including the AI accelerators powering the data center boom. It’s the critical quality-control infrastructure layer that every chip must pass through before reaching its destination.

Why Now: Teradyne’s Q4 2025 revenue hit $1.08 billion (+44% YoY), and the company is up approximately 59.8% YTD, the second-best performing stock in the entire S&P 500 in 2026. AI demand now accounts for 60%+ of revenue, and CEO Greg Smith expects this figure to exceed 70% in Q1 2026. The semiconductor test market, approximately $9 billion in 2025, is projected to grow to $12–14 billion as AI compute complexity drives higher test intensity per chip.

Unique Catalyst: Teradyne is on track for tester qualification in merchant GPUs, with production revenue expected in H2 2026. This positions TER to capture share in the fast-growing GPU testing market, currently dominated by captive test solutions from Nvidia’s key partners. At Morgan Stanley’s TMT Conference, management highlighted over 50% market share in wafer stack testing and a growing presence in HDD/SSD markets.

Valuation: At ~$320–357, TER trades at a premium but is a Strong Buy consensus with the company still in the early stages of a multi-year AI-driven ATE upgrade cycle. Revenue target of $6 billion (from $3.5B in 2025) underscores the multi-year runway.

Generac Holdings

NYSE: GNRC | Market Cap: ~$11.7B (Mid-Cap) | Sector: Power Generation / Energy Technology

Overview: Generac Holdings designs and manufactures power generation equipment, backup generators, energy storage systems, and grid services technology. The company is undergoing a strategic transformation from a “hurricane season” business into a critical infrastructure partner for hyperscale AI data centers.

Why Now: Management has guided for approximately 30% growth in its Commercial & Industrial (C&I) segment in 2026, driven primarily by hyperscale data center demand. The AI revolution’s physical requirement, an insatiable need for uninterruptible backup power, has made Generac’s products essential to every new data center being built. As AI models grow more sophisticated, data center uptime requirements become more stringent, making reliable backup power non-negotiable.

GNRC surged ~18% in a single day in February 2026 after its Q4 earnings, despite missing consensus estimates, because investors looked through the weather-related weakness and embraced the 2026 data center guidance. The stock has rallied 42–64% YTD to around $199–200.

Valuation & Risk/Reward: GNRC’s fair value is estimated at approximately $203.41 by the most-followed analyst narrative, suggesting the stock is roughly fairly valued at current levels, but undervalued relative to the multi-year data center infrastructure buildout that is just beginning. Structural improvements in gross margins, supply chain efficiencies, and cost management are driving EBITDA margin expansion to 18–19%, sustainable through 2026 and beyond. The market cap of $11.69 billion gives it significant room to grow into a $20–30B franchise if the data center power narrative plays out.

Strategic Recap & Forward Outlook

Markets enter the new week in a fragile state, with the S&P 500 bouncing off key support levels and the next leg of movement heavily dependent on Iran conflict headlines. Key things to watch:

-

Geopolitical: Any ceasefire signals or diplomatic openings in the US-Iran conflict could trigger a sharp relief rally in risk assets. Conversely, reports of additional US troop deployments could accelerate the current selloff.

-

Oil Prices: Brent crude and WTI movement will dictate intraday market direction. A sustained close below $100 in Brent would be the first meaningful bullish macro signal in weeks.

-

Fed Speakers: Multiple Fed officials scheduled to speak this week; any dovish pivot signals on the back of deteriorating labor data could support markets.

-

Micron Follow-Through: Post-earnings analyst upgrades and target revisions for MU will be the key corporate catalyst to watch. The magnitude of the Q3 guidance beat ($33.5B vs. $24.29B est.) will likely drive significant consensus revisions.

-

JPMorgan S&P 500 Watch: With JPMorgan’s revised year-end target at 7,200 and commentary about recession risk, institutional positioning changes could create additional selling pressure if macro data disappoints.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.