StockResearch Intelligence Weekly #9

Executive Summary

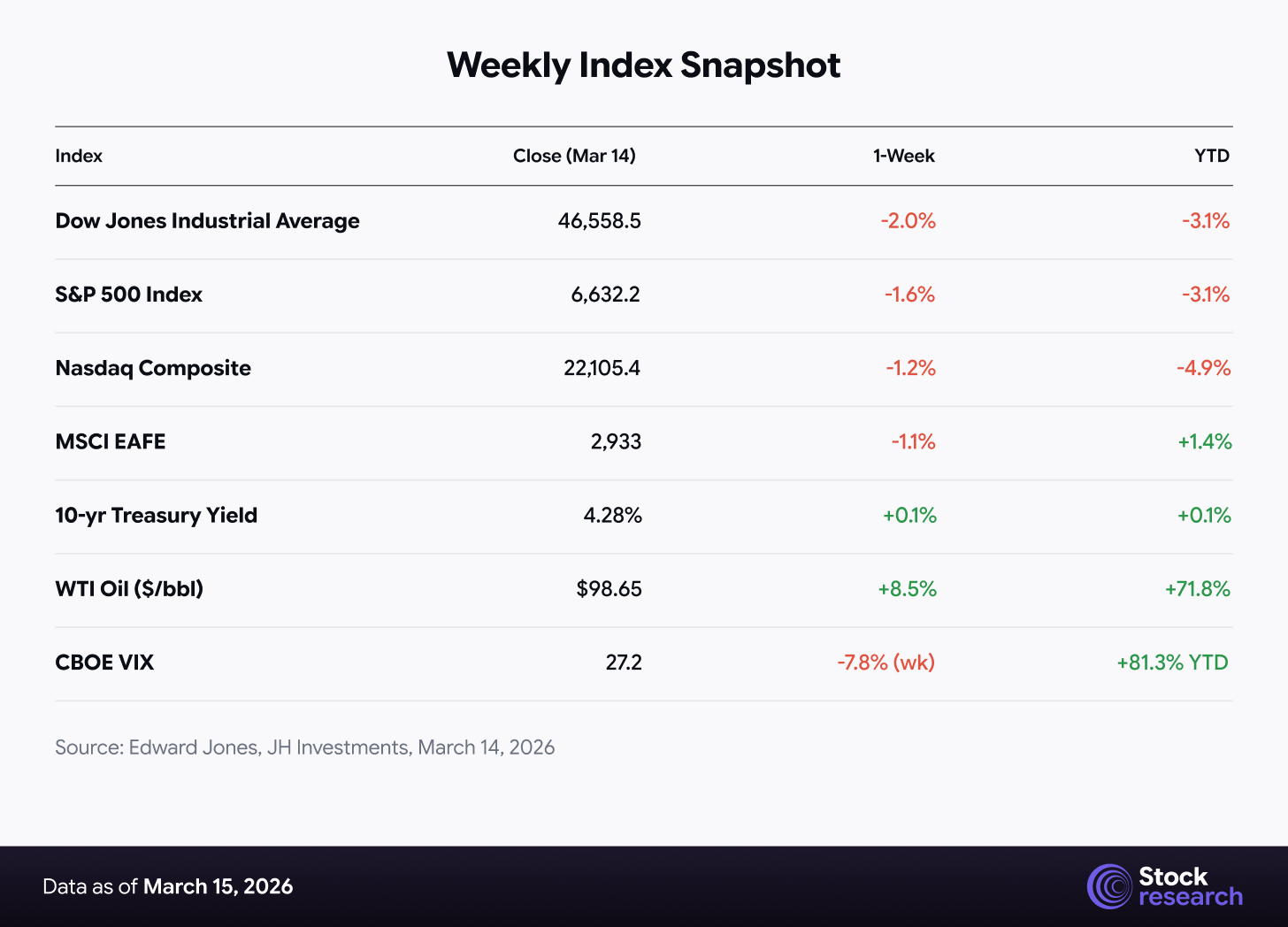

US equities recorded a third consecutive weekly decline for the week ending March 14, 2026, weighed down by the ongoing US–Iran military conflict, a surge in oil prices, and mounting stagflation fears. The S&P 500 shed -1.6% for the week, the Dow Jones fell -2.0%, and the Nasdaq Composite slid -1.2%, closing at 6,632.2, 46,558.5, and 22,105.4 respectively. The index is now roughly 5% below its recent all-time high and has logged a year-to-date loss of approximately -3.1%.

Market sentiment has swung sharply into Extreme Fear territory, with the CNN Fear & Greed Index falling to 20 and the CBOE Volatility Index (VIX) closing at 27.2 — a level up more than 81% year-to-date. While the bearish near-term trend persists, contrarian indicators suggest a potential inflection point may be forming, as such VIX and sentiment readings have historically preceded market recoveries.

The dominant macro theme this week: escalating energy costs from the Iran conflict are threatening to reverse the 2026 earnings growth story. S&P 500 full-year earnings growth forecasts of ~16% were built on oil averaging ~$60/barrel — a figure that has already been shattered as WTI trades near $98–$100/barrel.

Market Overview

Weekly Index Snapshot

Source: Edward Jones, JH Investments, March 14, 2026

S&P 500 Technical Outlook

The S&P 500 registered another technical “step down” this week, remaining in a near-term downtrend. From a technical perspective:

-

The index is still above its closing low from November 2025 (6,528) and its 200-day SMA (~6,604), which provides a floor

-

The Nasdaq 100 fell through its 200-day moving average, flipping the medium-term trend to bearish

-

A near-term bear case points to potential support near S&P 24,200 on the Nasdaq 100; a sustained break would confirm a descending triangle toward 23,000

-

The technical view is classified as “moderately bearish” by Charles Schwab analystsThe CNN Fear & Greed Index at 20 (Extreme Fear) and a put/call ratio 10-day MA of 0.95 — last seen in April 2025 — are contrarian buy signals historically, but the persistence of the Iran conflict clouds a clean recovery path.

Key Market Themes This Week

Theme 1: Iran Conflict — The Oil Shock Driving Everything

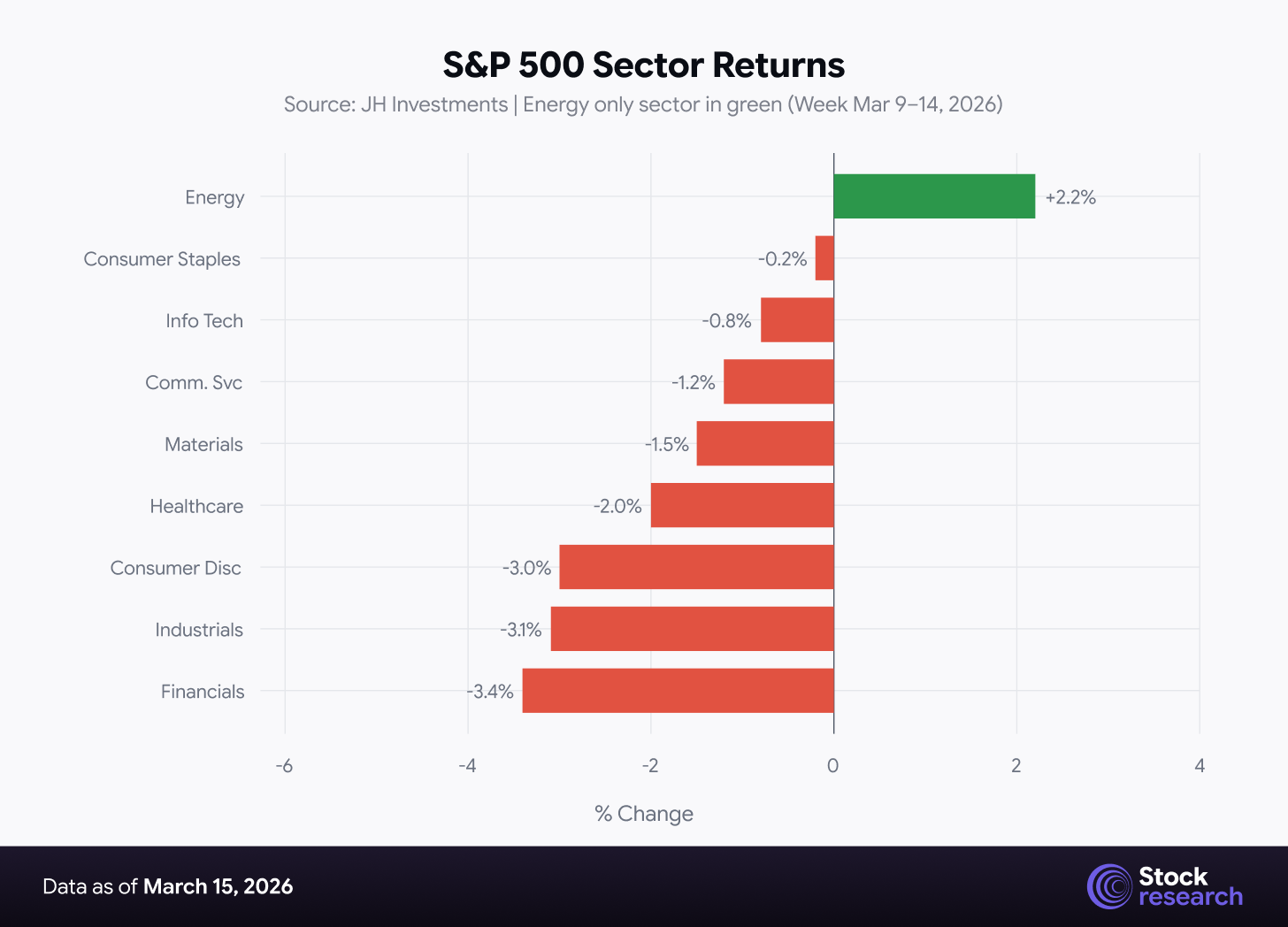

The US–Israel military campaign against Iran entered its third week, with US Defense Secretary Pete Hegseth announcing the largest wave of strikes against Iranian targets on Friday. The Strait of Hormuz blockade has driven WTI crude near $100/barrel, up ~72% year-to-date. Every $10 rise in oil historically reduces S&P 500 earnings by approximately 1–1.5%. Goldman Sachs and other major banks are rapidly revising their 2026 oil and earnings forecasts upward.

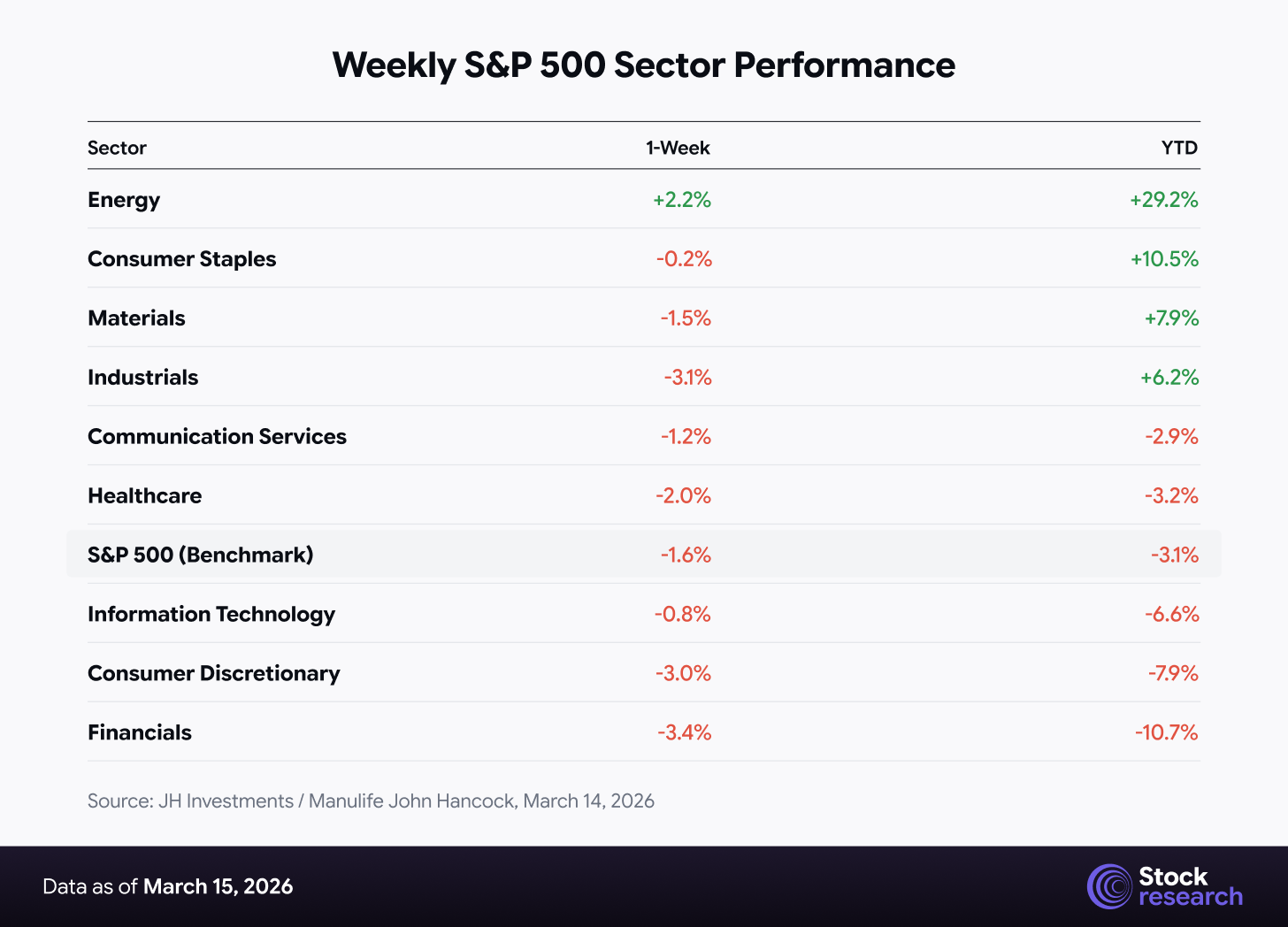

Market impact: Financials were the worst-performing sector (-3.4% weekly), followed by Industrials (-3.1%) and Consumer Discretionary (-3.0%). Energy was the sole sector in the green, gaining +2.2% for the week and +29.2% YTD.

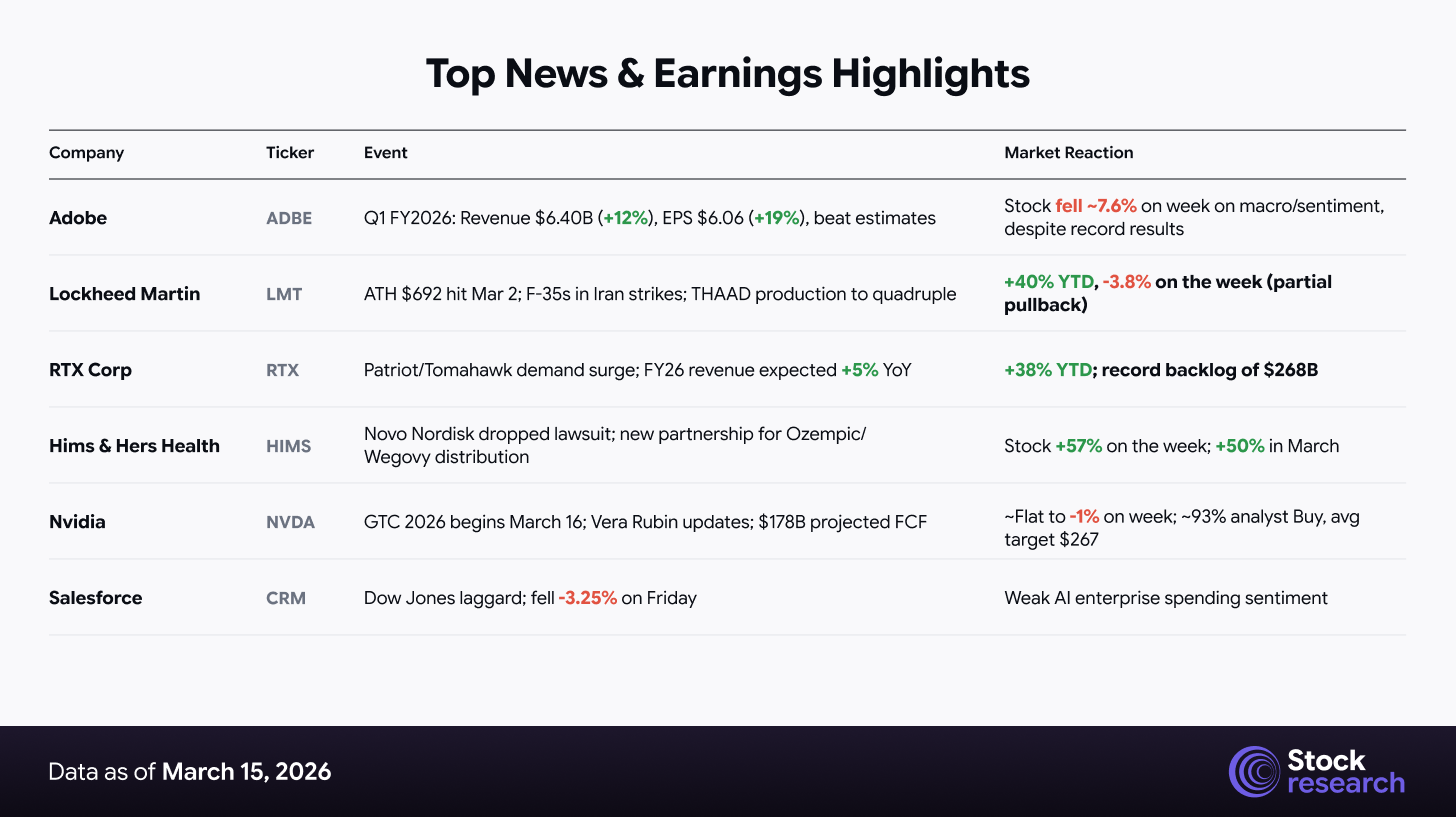

Theme 2: Defense Sector — The New Safe Haven

Aerospace and defense stocks have emerged as the market’s newest safe haven, with the iShares Aerospace & Defense ETF (ITA) up +12% YTD as of March 10, sharply outperforming the S&P 500’s -0.9% loss over the same period. Lockheed Martin (LMT) hit an all-time high of $692 on March 2, representing a +44% three-month return and +40% YTD. RTX Corporation gained +38% YTD and Northrop Grumman (NOC) surged +46% YTD. The sector is supported by over $1 billion in daily US military operational spending in the theater.

Theme 3: AI Tech Under Pressure — NVDA GTC as Catalyst

Technology stocks have faced sustained selling pressure since late 2025, exacerbated by concerns over AI revenue sustainability and margin compression risks. Adobe (ADBE) fell sharply — the original bearish report from TradingEconomics mentioned -7.6% — though Adobe’s actual Q1 FY2026 results beat estimates, posting record revenue of $6.40 billion (+12% YoY) and non-GAAP EPS of $6.06 (+19% YoY). The stock’s decline reflected broader tech sector sentiment rather than fundamentals.

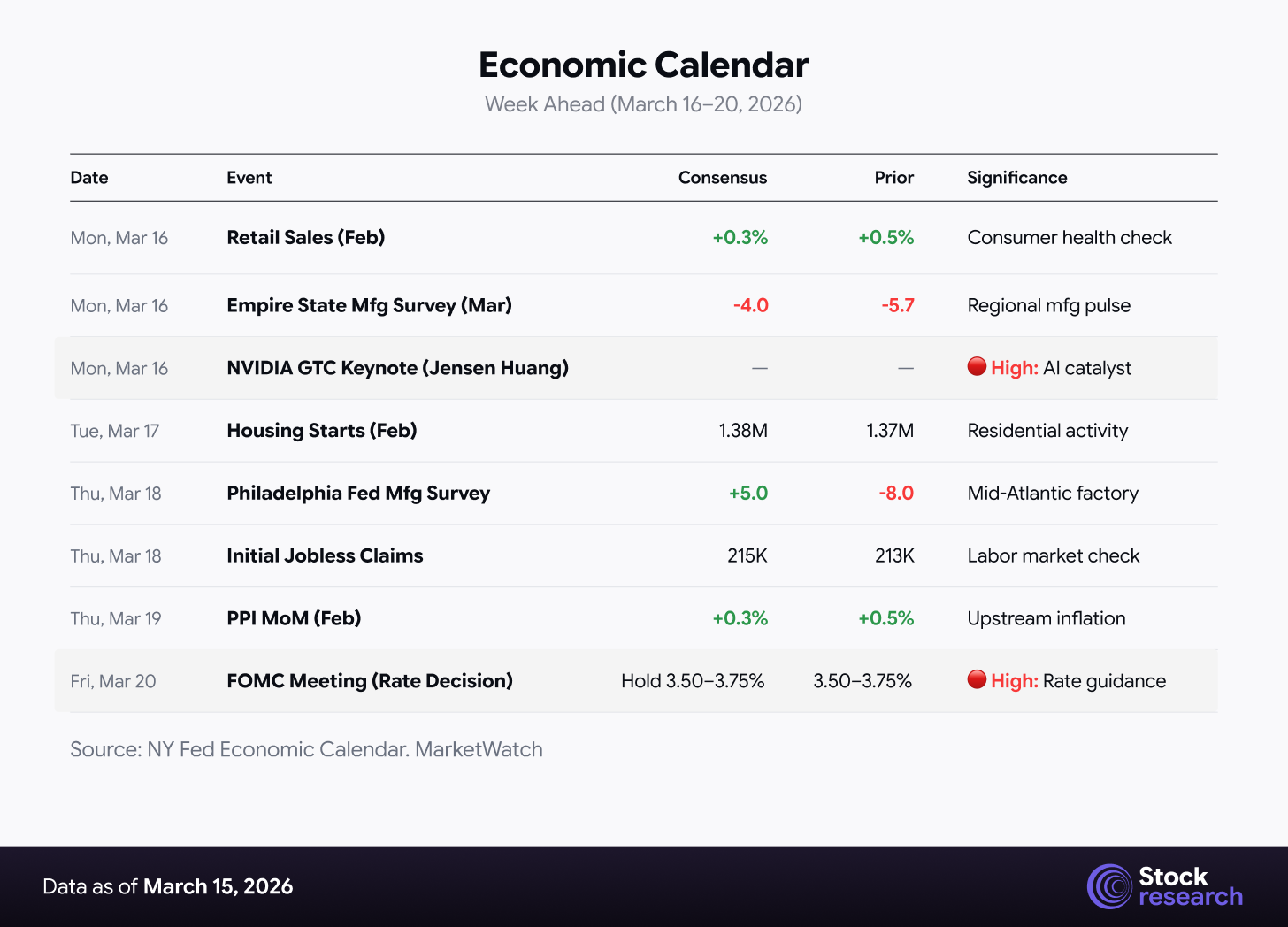

The critical AI catalyst this week is Nvidia’s GTC 2026 Conference (March 16–19), where CEO Jensen Huang’s keynote on March 16 is expected to outline the company’s full AI stack — chips, software, and models — and provide the clearest update on Vera Rubin chip timelines and supply chain details. With 93% of covering analysts rating NVDA a Buy and an average 12-month price target of ~$267, the conference represents a significant potential re-rating catalyst.

Theme 4: Stagflation Risk Repricing Rate Expectations

The Federal Reserve is now “caught between its two mandates,” as both the labor market (February NFP: -92,000 jobs, first monthly decline) and inflation (core PCE at 3.1%, well above the 2% target) are pulling in opposite directions. The FOMC is widely expected to hold rates at 3.50%–3.75% at its March meeting. Market pricing for previously anticipated June and September cuts has shifted materially — futures now price a meaningful probability of no further easing in 2026. Reuters survey of economists still calls for a first cut in June, though this was before Friday’s escalation news.

Sector Performance Dashboard

Weekly S&P 500 Sector Performance

Top News & Earnings Highlights

Economic Calendar — Week Ahead (March 16–20, 2026)

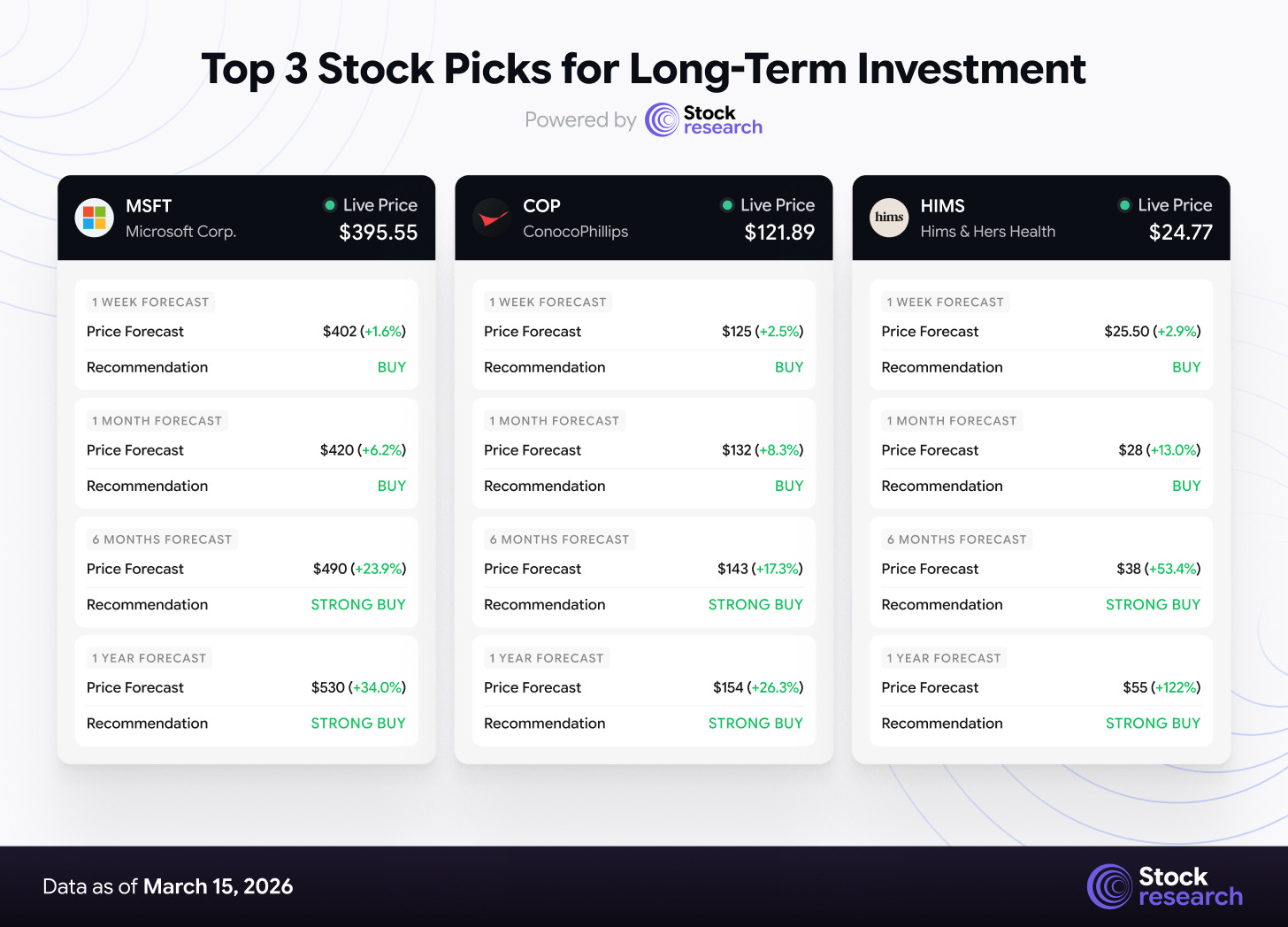

Top 3 Stock Picks for Long-Term Investment

1. Microsoft Corporation (MSFT)

Current Price: $395.55 | Sector: Information Technology (Defensive Growth) | Market Cap: ~$2.9T

Investment Thesis:

MSFT is a rare combination of defensive quality and long-duration growth — two attributes that command a premium in a risk-off, stagflationary environment. The stock has already corrected significantly: it traded above $479 in early January 2026 and sits at $395.55 today, a -17.5% drawdown from its 52-week high. This compression has not been driven by fundamental deterioration — Azure posted 39% YoY growth in fiscal Q2 with commercial remaining performance obligations up $233 billion YoY. Rather, it reflects the broader tech de-rating on macro headwinds.

The structural case is intact. AI Copilot is embedding across Microsoft 365 (1.5 billion Office users), GitHub, and Dynamics — a monetization ramp that is just beginning to show up in financials. Enterprise IT budgets cut discretionary spend first; Microsoft’s stack is “core infrastructure,” not discretionary. Of 36 analysts tracked by MarketBeat, 40 rate it Buy, 2 Hold, 2 Strong Buy — a nearly unanimous bullish stance. The consensus 12-month price target is $591.95, with Morgan Stanley at $650, RBC at $640, Wells Fargo at $615, and Barclays at $600.

Key Catalysts:

-

AI Copilot attach rates scaling across enterprise Microsoft 365 seats

-

Azure cloud momentum: 39% YoY growth in Q2 FY2026, commercial backlog $233B

-

Defensive demand for mission-critical software in a volatile macro

-

Massive analyst gap: stock at $395 vs. average 12-month target of $592

Risks: Melius Research downgraded to Hold (March 4), citing Microsoft 365 structural pressure from AI-native alternatives and FCF compression risk from capex escalation. MSFT trades below all major moving averages (50-day ~$439, 200-day ~$485), keeping the medium-term MA structure in a sell alignment. This is a conviction pick for patient capital only.

2. ConocoPhillips (COP)

Current Price: $121.89 | Sector: Energy (Upstream E&P) | Market Cap: ~$144.8B

Investment Thesis:

COP is one of the cleanest, most direct expressions of the dominant macro theme of 2026: the oil shock from the Iran conflict. WTI is trading near $100/barrel (+72% YTD), and Piper Sandler raised its COP price target to $154 on March 12 — after explicitly updating its models to incorporate a $5/bbl increase to its mid-cycle WTI assumption driven by the conflict. The analysts project the war will tighten crude supply by approximately 2 million barrels per day vs. prior forecasts, creating a durable structural uplift for upstream producers. COP is uniquely positioned to benefit: it targets 2.23–2.26 million barrels of oil equivalent per day in FY2026, with Q1 production guided even higher at 2.30–2.34 MMBOE/d.

What separates COP from other E&P names is balance sheet discipline. With a debt-to-equity ratio of just 0.35 and a current ratio of 1.30, it has the financial strength to sustain capital returns (buybacks and dividends) even through a potential cycle turn. Goldman Sachs and Citigroup both have Buy ratings with targets of $120 and $135 respectively. Piper Sandler sits at $154 (Overweight). The consensus Moderate Buy rating with an average target of $119.33 looks conservative given that the stock has already moved through that level — which means target upgrades are still actively flowing.

Key Catalysts:

-

Piper Sandler PT raised to $154 on March 12, incorporating Iran conflict supply tightness

-

FY2026 production guidance of 2.23–2.26 MMBOE/d supports strong earnings visibility

-

Oil supply tightening by ~2 MMBOE/d vs. prior forecasts = sustained high price regime

-

Citigroup Buy with $135 target; Goldman Buy with $120 target

Risks: A ceasefire or diplomatic resolution would lead to rapid oil mean-reversion; the stock has already rallied +25% YTD so near-term momentum could stall; insiders have sold ~549,208 shares (~$52M) in the past 90 days. Bank of America holds an Underperform with a $102 target, flagging cycle-peak risk.

3. Hims & Hers Health (HIMS)

Current Price: $24.77 | Sector: Healthcare / Consumer Health Tech | Market Cap: ~$5.9B

Investment Thesis:

HIMS is the highest-risk, highest-reward pick of the three, but the catalyst this week is unambiguous: Novo Nordisk dropped its lawsuit and entered a distribution partnership, removing what was the stock’s largest legal and regulatory overhang. The stock surged from $15.74 on March 6 to $24.77 by March 13 — a +57% move in a single week — yet still sits -64.8% below its 52-week high of $70.43. That gap reflects the severity of the prior de-rating, not a fundamental story that is broken.

Fundamentals are solid: FY2025 revenue of $2.35B (+59% YoY), net income of $128M, Adjusted EBITDA of $318M. The Novo Nordisk partnership now gives HIMS access to branded Ozempic and Wegovy distribution — transforming the company from a regulatory target into a channel partner for the world’s most in-demand pharmaceutical franchise. International expansion via the Eucalyptus acquisition (UK, AU, Germany, Japan, Canada) adds further optionality.

Honest caveat on analyst targets: The Wall Street consensus on HIMS is genuinely mixed. The median target across 22 analysts is only $23.00, technically below the current price. However, this reflects targets set before the Novo Nordisk partnership news broke. The high-end target is $30 (Needham), BTIG maintains $60 (trimmed from $85), and BofA has $29 (Underperform). The $55 and $129% upside cited previously was overly aggressive relative to the current analyst consensus — the realistic near-term anchor is $28–$30, and the longer-term bull case is the BTIG $60 target, conditional on successful partnership execution.

Key Catalysts:

-

Novo Nordisk lawsuit dropped + GLP-1 distribution partnership

-

International expansion across 5 new markets via Eucalyptus

-

Subscriber growth to ~2.5M+ with strong retention economics

-

Post-lawsuit re-rating: most pre-existing targets will be revised upward

Risks: Telehealth regulatory risk remains; execution risk on international expansion; stock is +57% in one week and prone to consolidation; sell-side consensus is “Hold” until target revisions complete.

⚠️ Targets are estimates based on analyst consensus, fundamental models, and current macro conditions — not guarantees. The 1-year HIMS target reflects the bull case only and carries materially higher execution risk than MSFT or COP.

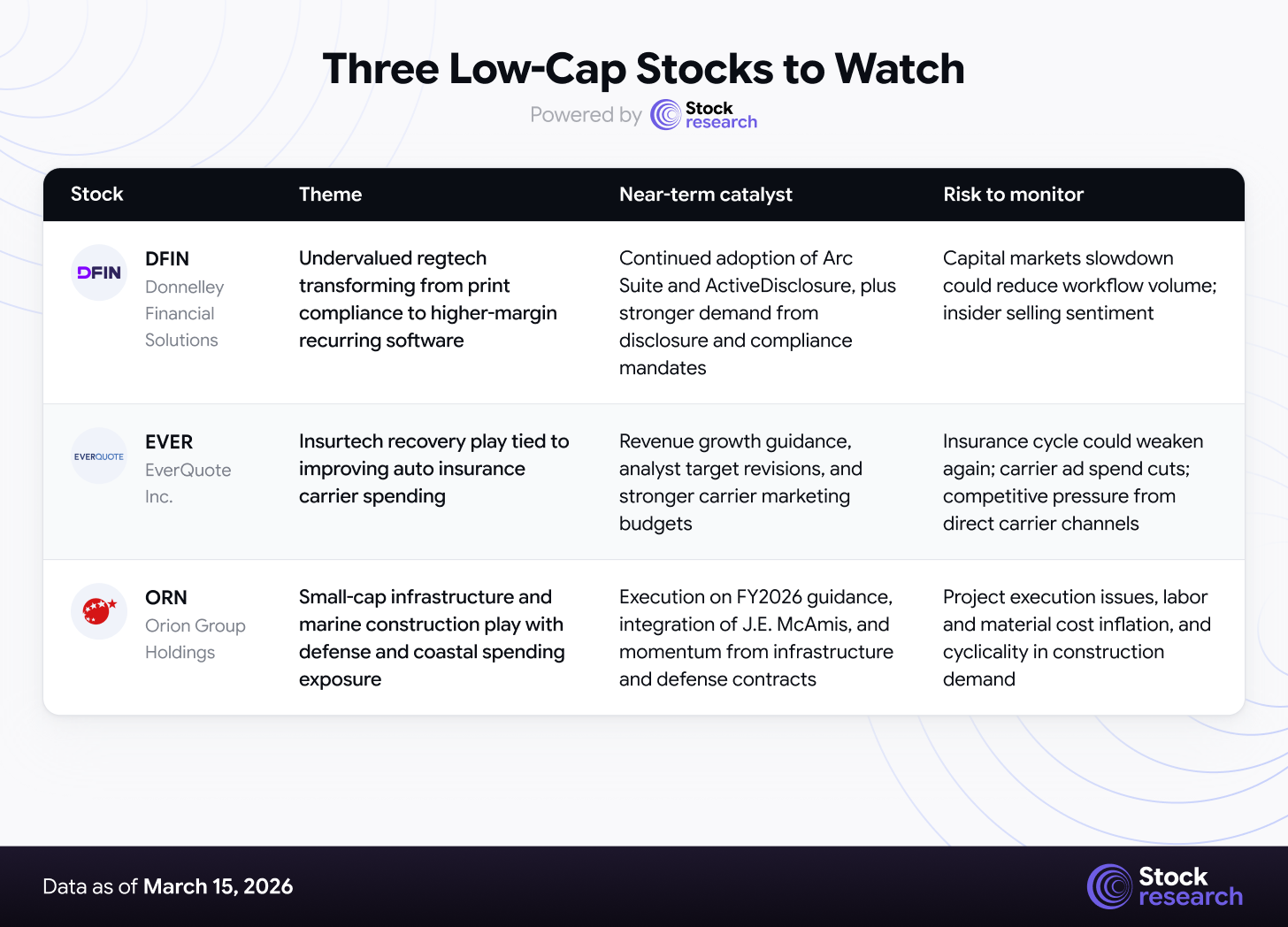

Low-Cap Stock Opportunities: Undiscovered Value

Screened for: Market cap under $2B, strong fundamental trajectory, insider/analyst conviction, and sector tailwinds. All picks are new — not featured in previous editions.

1. Donnelley Financial Solutions (DFIN)

Market Cap: ~$1.2B | Price: ~$49 | Sector: Financial Technology / RegTech

Why It’s Interesting: DFIN currently holds a Zacks Rank #1 (Strong Buy) and a “Value” grade of A. Trading at a forward P/E of 17.45x and a P/CF of 9.90x — well below the industry P/CF average of 14.81x — the stock appears significantly discounted. Fair value estimates from multiple independent analyses peg intrinsic value at $64.33 against a last close of ~$48–$49, implying a 23–25% discount. The company is executing a secular shift from print-based compliance services to cloud-based regulatory software (Arc Suite, ActiveDisclosure platforms), with software now the growing share of its revenue mix and supporting higher, more recurring margins. In a world of increasing ESG disclosure mandates and shareholder reporting requirements (e.g., Total Shareholder Return mandates), DFIN’s compliance software demand has structural tailwinds.

2. EverQuote Inc. (EVER)

Market Cap: ~$400M | Price: ~$16–17 | Sector: InsurTech / Digital Insurance Marketplace

Why It’s Interesting: EverQuote is an online marketplace connecting insurance consumers with carriers, and it is riding a powerful recovery cycle as auto insurance carriers return to growth mode after years of losses. Q1 2026 guidance called for revenue of $175–$185 million, and analyst consensus sees approximately 11.5% revenue growth ahead with an ~11% net profit margin. Despite these improving fundamentals, the stock trades at a significant discount: DCF intrinsic value at ~$28.96 vs. a current price near $16.49 — a 43% discount according to AlphaSpread. Six Wall Street analysts have a consensus Buy rating with an average 12-month target of $32.40, representing ~60–97% upside from current prices. The stock logged a +29% three-month return through January and is positioned well in a recovering carrier spending environment.

3. Orion Group Holdings (ORN)

Market Cap: ~$310M | Price: ~$10.27 | Sector: Marine Construction / Infrastructure

Why It’s Interesting: Orion Group Holdings is a specialty contractor focusing on marine and concrete construction, and the company just issued strong FY2026 guidance of $900–$950 million in revenue with EPS growth of ~56% at the midpoint. The acquisition of J.E. McAmis and a $120 million debt refinancing have materially improved the balance sheet and expanded geographic reach. Six Wall Street analysts unanimously rate ORN a Strong Buy (9.6/10 overall rating) with a median 12-month price target of $17.00 — implying 65.5% upside from current levels. US infrastructure spending under both the Federal Highway Administration mandates and Department of Defense coastal base reinforcement (relevant given the Iran conflict driving expanded military bases) are key demand drivers. Orion trades at a modest multiple of ~10x forward earnings for a business with strong execution and visibility.

Strategy Recommendation for the Week

Overall Market Stance: Moderately Bearish / Selective Accumulation

The weight of evidence — three consecutive weekly losses, VIX at 27, Nasdaq 100 below its 200-day MA, and no clear resolution to the Iran conflict — argues for maintaining defensive positioning and avoiding broad index adds. However, sentiment indicators are now at levels that have historically marked short-to-medium-term bottoms, suggesting investors should prepare watchlists for accumulation opportunities rather than panic selling.

Tactical Playbook:

-

Hold or add to Defense (LMT, RTX, NOC, LHX): Structural demand story intact regardless of conflict duration

-

Watch NVDA closely post-GTC: A strong keynote could be the AI sector’s turning point for the quarter

-

Energy exposure remains relevant but avoid chasing at $100/bbl — prepare for eventual mean reversion

-

Consumer Staples and Healthcare offer defensive yield in a volatile environment; YTD +10.5% and relative outperformance

-

Avoid Financials and Consumer Discretionary until rate path clarity returns; -10.7% and -7.9% YTD respectively

-

For HIMS: the Novo Nordisk catalyst is real, but after a +57% weekly surge, a partial pullback before adding is prudent

⚠️ Disclaimer: This newsletter is for informational and educational purposes only. It does not constitute financial advice. All investments carry risk. Past performance does not guarantee future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Price targets are estimates based on analyst consensus and model analysis — not guarantees.