StockResearch Intelligence Weekly #8

During March 2–6, 2026, U.S. equities finally cracked under the weight of the macro and geopolitical pressures that had been building for weeks, as the Iran war, an oil price shock, and a shockingly weak jobs report converged into a full‑blown risk‑off episode. The S&P 500 slid 2.0 percent to 6,740.02, the Nasdaq fell 1.2 percent to 22,387.70, and the Dow dropped 2.9 percent to 47,501.60, while the VIX spiked toward the 30 level, its highest reading since early 2025. What began as a “contained” Middle East conflict morphed into a direct threat to global energy supply via the Strait of Hormuz, just as February nonfarm payrolls printed negative and long‑term yields pushed higher, leaving investors suddenly having to price not just sticky inflation and AI‑driven capex cycles, but also an oil‑driven stagflation scare.

Strengths

-

Energy and hard-asset leadership: Energy extended its outperformance as crude ripped through the 90‑dollar level and Brent broke above 100, putting integrated majors, upstream producers, and select refiners firmly in the driver’s seat while gold and other hard assets benefited from a renewed bid for real‑asset hedges.

-

Defense supercycle gaining momentum: Aerospace and defense names such as Lockheed Martin, Northrop Grumman, and missile‑systems suppliers continued to grind higher on rising order books, multi‑year budget visibility, and fresh demand linked to the Iran conflict and broader re‑armament trends.

-

Factor and style diversification beneath the surface: Despite headline index weakness, equal‑weight benchmarks and small‑cap value continued to hold up better than mega‑cap growth, suggesting that positioning is no longer as one‑sided and that investors are selectively rotating rather than indiscriminately liquidating risk.

Weaknesses

-

Stagflation risk: oil shock meets softening labor data: The combination of a negative February payrolls print, a rising unemployment rate, and a double‑digit percentage spike in crude prices has resurrected stagflation concerns, narrowing the Fed’s room for manoeuvre and raising the odds of a growth scare without rapid disinflation.

-

Geopolitical tail‑risk around the Strait of Hormuz: The widening Iran conflict and explicit threats to shipping in and around the Strait of Hormuz have turned a regional war into a global supply‑chain and energy‑security problem, increasing the probability of further commodity volatility and episodic air‑pockets in risk assets.

-

Tighter financial conditions and fragile risk sentiment: Higher long‑end yields, a bid for the U.S. dollar, and a VIX pushing toward 30 have tightened financial conditions at the same time that equity drawdowns are broadening, leaving high‑multiple growth, unprofitable tech, and highly levered balance sheets particularly exposed to further de‑rating.

Market Recap

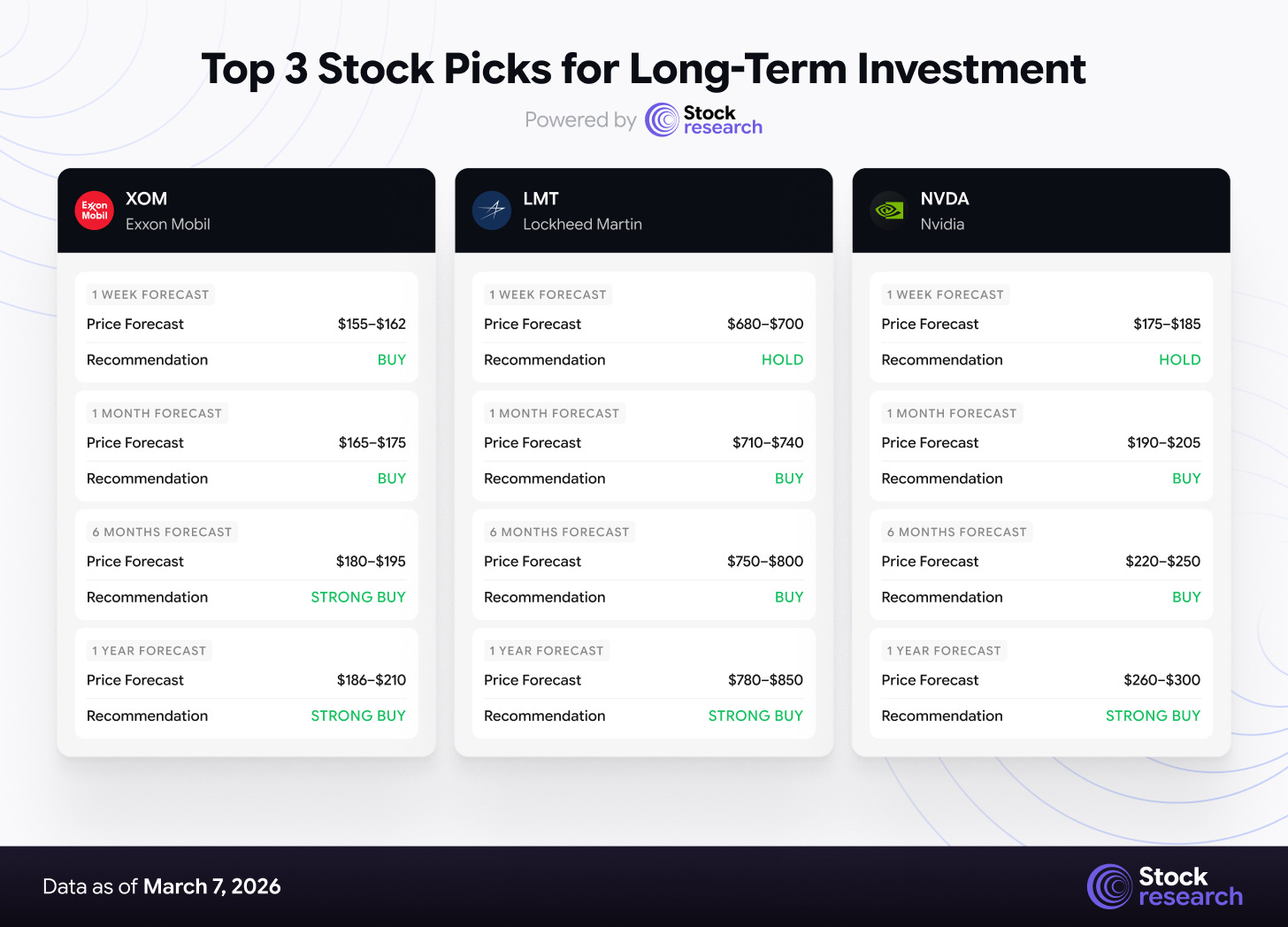

Top 3 Stock Picks for Long-Term Investment

1. Exxon Mobil (XOM)

The Oil Supercycle Beneficiary

Why XOM Now (Again): Exxon Mobil is the premier beneficiary of the current oil shock. The company produced 4.7 million barrels in Q4 2025 and posted $6.5 billion in earnings on $82.3 billion revenue. With WTI now surging past $90 and Brent exceeding $107, XOM’s earnings leverage to crude prices is extraordinary. JPMorgan raised its price target to $133 in January (now well exceeded), and the stock trades at a P/E of 22.57 with a 2.7% dividend yield.

The structural case is compelling: the energy sector has the lowest valuation in the S&P 500 despite being the top performer YTD (+25%). Historical data from Bespoke Investment Group shows that in the last three instances where the energy sector gained at least 10% through mid-February, it subsequently gained at least 15% more for the rest of the year. The Strait of Hormuz disruption could persist for months, and OPEC supply constraints add further tailwinds.

Key Risks: Ceasefire or diplomatic resolution lowering oil prices; demand destruction from recession; potential strategic petroleum reserve releases.

2. Lockheed Martin (LMT)

Defense Spending Supercycle

Why LMT Now: Lockheed Martin hit an all-time high of $692 earlier in the week (March 2) as defense stocks rallied on Iran strikes. The stock has gained over 41% in the past 12 months. The analyst consensus price target is $565, but this was set before the current conflict escalation — Citigroup’s $673 target (issued February 5) has already been breached.

The defense spending supercycle is structural, not cyclical. NATO allies are accelerating toward 2%+ GDP defense spending commitments, the US defense budget continues to grow, and the Iran conflict has created urgent demand for missile systems, fighter jets, and missile defense. The company’s technical indicators show a strong bullish trend with SMA20 above SMA60.

Key Risks: Conflict de-escalation reducing defense urgency; margin pressure from supply chain issues; valuation stretched at current levels (Morningstar fair value at $355 — though this appears to underweight the new geopolitical paradigm).

3. NVIDIA (NVDA) — The Beaten-Down AI King

Why NVDA Now (And again): NVIDIA has pulled back 26% from its all-time highs, creating a compelling entry point for long-term investors. The company reported $68.1 billion in Q4 FY2026 revenue with significant year-over-year acceleration. CLSA maintains a “high-conviction” Outperform rating with a $300 price target, citing “exponential token growth, buoyant earnings, and attractive valuations”.

The forward P/E has dropped to ~36x — comparable to Costco and Walmart — despite 50%+ projected earnings growth. The Rubin architecture launching in late 2026 will trigger a fresh upgrade cycle, and NVIDIA’s $5 billion investment in Intel for 2028 chip co-manufacturing strengthens its supply chain moat. The current selloff is driven by macro fears (oil, geopolitics) rather than fundamental deterioration — revenue guidance of $65 billion for Q4 FY2026 was a blowout beat.

Key Risks: Further AI chip export restrictions (Trump admin drafting new rules); hyperscaler capex slowdown; continued multiple compression in a rising rate environment; broader tech selloff deepening.

Low-Cap Stock Opportunities: Undiscovered Value

The following three stocks represent overlooked opportunities in the sub-$10 billion market cap space, each benefiting from structural tailwinds that the geopolitical shock has now amplified.

1. Argan, Inc. (AGX)

AI Power Plant Builder

-

Price: ~$110 (March 2026) | Market Cap: ~$2.1B | Sector: Industrials — Construction

Argan is a direct play on the explosive demand for power infrastructure driven by AI data centers. The company specializes in designing and constructing power plants, primarily natural gas facilities, and has built a record $3 billion project backlog. It recently won two large Texas contracts to build power plants specifically supplying electricity to AI data center workloads.

The Power Industry Services segment generates 83% of revenue, and the company’s “energy-agnostic” capabilities allow it to build gas plants, solar farms, and battery storage. Argan’s share price has gained 35.70% YTD and 25.13% in the past 30 days. Morgan Stanley projects AI-related power demand will grow 70% annually through 2027, and Argan sits at the nexus of this structural trend.

Catalyst: Continued data center power demand announcements; rising natural gas prices from the oil/energy shock benefiting power plant construction urgency.

2. NANO Nuclear Energy (NNE)

Microreactor Pioneer

-

Price: ~$23.54 | Market Cap: ~$1.23B | Sector: Energy — Nuclear

NANO Nuclear Energy is developing the KRONOS MMR, a high-temperature gas-cooled microreactor designed for remote and specialized applications including AI data center power. The company has $577.5 million in cash after a successful $400 million private placement in October 2025.

NNE recently signed an MOU with EHC Investment LLC to advance micro modular reactor deployment in the UAE, and its projected revenue trajectory shows growth from under $10 million in FY2026 to nearly $4 billion by FY2037 (73.2% CAGR). With an analyst consensus target of $29.50 (25.3% upside), NNE represents speculative but high-conviction exposure to the intersection of nuclear energy and AI infrastructure.

Catalyst: Regulatory milestones for KRONOS MMR; additional international deployment agreements; rising power demand narrative from the energy crisis.

3. Consolidated Water Co. (CWCO)

Defensive Water Utility

-

Price: ~$38 | Market Cap: ~$562M | Sector: Utilities — Water

In a market dominated by geopolitical fear and energy volatility, Consolidated Water offers a defensive anchor. The company provides water utility services and water-related infrastructure, serving the Caribbean and US markets. It trades at a reasonable valuation with a 1.5% dividend yield.

Water utilities are one of the most recession-resistant sectors, and CWCO’s exposure to desalination technology gives it a structural growth angle as climate-driven water scarcity intensifies globally. With the VIX at 29.5 and a potential recession signal from the -92K jobs print, defensive positioning in essential services becomes increasingly attractive.

Catalyst: Rotation into defensive/utility sectors during market turmoil; potential infrastructure spending legislation; climate-driven water demand growth.

Strategic Recap & Forward Outlook

Forward Outlook (Week Ending March 14, 2026)

The coming week sits at the intersection of three forces that now fully define the 2026 tape: an open‑ended Iran war and ongoing threats to the Strait of Hormuz, an oil shock that has pushed Brent through 90 dollars and toward the 100‑dollar conversation, and a labor market that just printed negative payrolls for the first time in the current cycle. With the VIX hovering near 30 and long‑end yields grinding higher, every incremental data point on inflation and growth will feed directly into how aggressively investors price stagflation risk versus the probability that the Fed will still be able to ease in the second half of the year.

Three variables will determine near‑term market direction:

-

Strait of Hormuz, oil path, and inflation expectations:

If U.S. and allied efforts to provide military and insurance escorts succeed in partially reopening tanker routes over the next couple of weeks, the parabolic move in crude could stall below 100 dollars and inflation expectations may stabilize, allowing equities to find a trading floor above the recent lows. A prolonged or renewed shutdown, especially if accompanied by further strikes on Gulf infrastructure, would keep Brent above 90–100 dollars, add several tenths to projected inflation, and force markets to price a higher terminal inflation path and a slower, later Fed easing cycle. -

Depth and duration of the Iran conflict:

Markets can digest short, clearly bounded operations but struggle when rhetoric hardens and timelines blur, and recent commentary from Washington and Tehran points toward an extended campaign rather than a quick de‑escalation. Evidence that back‑channel diplomacy is gaining traction or that shipping protections are working would support a relief rally in cyclicals and high‑beta tech, while any fresh attacks on U.S. assets or allies, or clear signs that the war is expanding geographically, would likely entrench the current risk‑off regime and further entrench the outperformance of Energy, Defense, Utilities, and gold. -

Inflation data, growth signals, and Fed reaction function:

Next Wednesday’s CPI release is now the most important macro event on the calendar, not because it fully captures the latest oil spike—it will not—but because it will tell investors whether underlying core inflation was already re‑accelerating before the conflict. If CPI and subsequent PCE data surprise to the upside while oil remains elevated, the Fed will have very little room to validate current rate‑cut hopes, increasing recession odds and arguing for a more defensive equity stance; softer‑than‑feared prints, especially on core measures, would reopen the path to second‑half cuts and could trigger a sharp short‑covering rally from depressed sentiment levels.

Positioning guidance:

-

Stay overweight Energy and Defense; selectively add hard‑asset plays:

As long as Hormuz remains a live risk and oil trades with a war premium, integrated majors, upstream producers, and midstream infrastructure offer one of the clearest fundamental backdrops in the market, while defense primes and missile‑system suppliers sit at the center of a multi‑year re‑armament cycle. Positions can be legged into on pullbacks rather than chased after gap‑up days, but the strategic tilt toward energy security and defense budgets is unlikely to reverse quickly even if risk sentiment temporarily improves. -

Favor real‑world AI infrastructure over long‑duration AI narratives:

The macro regime now rewards companies tied to power, connectivity, and physical compute capacity—utilities, grid modernizers, power‑plant builders, foundries, and AI hardware—more than high‑multiple, story‑driven software names whose cash flows sit furthest in the future. Within tech, that argues for maintaining or building exposure to high‑quality semiconductor, networking, and infrastructure names on weakness while remaining cautious on unprofitable or richly valued software until expectations and valuations have reset to the new rate and risk environment. -

Lean into defense, utilities, and quality balance sheets as stagflation hedges:

With stagflation risk now a central scenario rather than a tail, sectors with regulated pricing power, inelastic demand, and strong free‑cash‑flow support—Utilities, Consumer Staples, select Healthcare—are positioned to outperform broad indices if growth slows while prices stay firm. Large‑cap companies with net cash balance sheets, high interest coverage, and proven ability to support buybacks and dividends through downturns should form the core of equity exposure while credit spreads remain well‑behaved but vulnerable to a further risk‑off leg. -

Use volatility to average into structural winners, not to chase short squeezes:

A VIX near 30 and persistent headline risk mean gap moves and intraday reversals are likely to remain the norm, making staggered, time‑diversified entries more attractive than single‑day deployments. For investors with multi‑year horizons, the priority should be gradually accumulating positions in businesses that sit at the nexus of enduring themes—energy security, AI compute and power, defense, and critical infrastructure—while keeping some dry powder in cash and short‑duration fixed income to take advantage of any capitulation events that might still lie ahead.

Periods where war risk, inflation anxiety, and growth fears collide are uncomfortable but historically have created some of the best forward return opportunities for patient capital willing to separate cyclical drawdowns from structural winners. The key in this phase is not to predict each headline, but to ensure portfolios are aligned with the world that is actually emerging—more volatile, more energy‑constrained, and more capital‑intensive—rather than the low‑inflation, zero‑rate world that priced so much of the last cycle’s growth trade.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.