StockResearch Intelligence Weekly #7

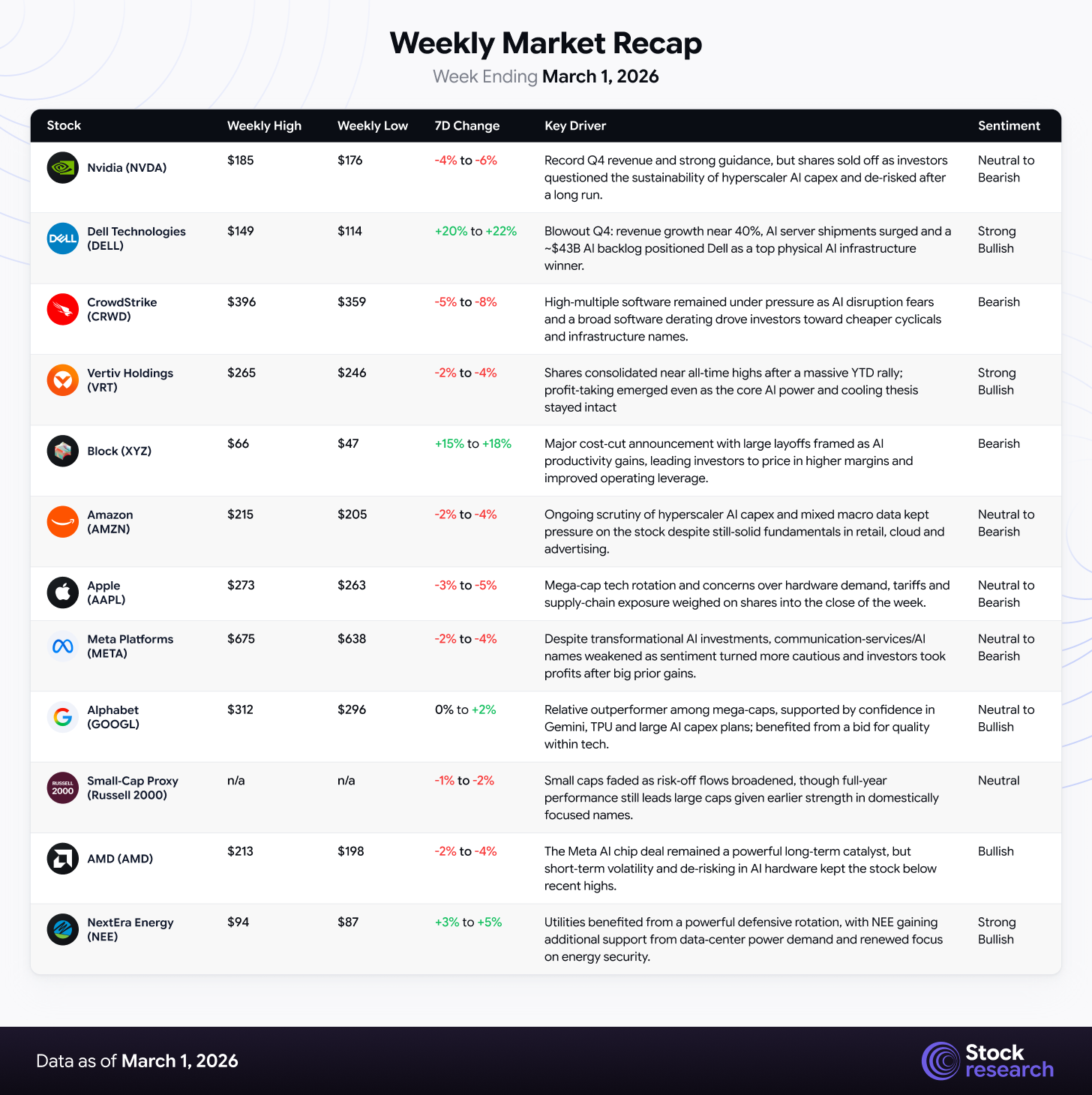

During February 24–28, 2026, U.S. equities slipped into a cautious, risk‑off posture as a fragile macro backdrop of hot inflation and AI disruption fears collided with a major geopolitical shock at the very end of the week. The S&P 500 fell 0.4 percent to 6,878.88, the Nasdaq lost 0.9 percent to 22,668.21, and the Dow dropped 1.3 percent to 48,977.92, while the VIX climbed to 19.86. Before markets closed on Friday, the narrative was already challenging, with the Nasdaq suffering its worst month since March 2025, software under heavy pressure, and the PCE inflation gauge re‑accelerating; over the weekend, the U.S. and Israel then launched Operation Epic Fury against Iran, triggering a sharp jump in oil, a surge in gold and a slide in U.S. equity futures.

The result is a market now facing a triple threat: structurally higher AI capex that investors are struggling to value, an inflation trajectory that has turned higher again, and an active kinetic conflict in the Middle East that threatens global energy supply through the Strait of Hormuz. Defensive sectors such as Utilities, Consumer Staples, Energy and Defense outperformed through February and are now positioned to benefit further from the new geopolitical risk premium, while high‑multiple software and long‑duration growth stocks remain under pressure.

Strengths

-

Energy and defense leadership: Energy has become the best performing sector year to date with gains near 24 percent, supported by firm oil prices even before the weekend strikes; defense names such as Lockheed Martin and Northrop Grumman hit fresh highs in February on record backlogs and rising global security spending.

-

Corporate balance‑sheet strength and buybacks: Large‑cap U.S. companies collectively announced more than 230 billion dollars of share repurchases during February, providing a stabilizing force under indices even as valuations in certain pockets compressed.

-

Flight to quality benefits U.S. dollar and Treasuries: The Iran shock produced classic safe‑haven flows into the U.S. dollar and long‑dated Treasuries, keeping U.S. funding conditions relatively orderly for now despite higher inflation readings.

Weaknesses

-

Hot inflation with new oil shock risk: The December PCE price index accelerated to 2.9 percent year over year and core PCE to 3.0 percent, and analysts now estimate that a sustained disruption in the Strait of Hormuz could add 0.6–0.7 percentage points to global inflation, making rate cuts significantly less likely in 2026.

-

Geopolitical escalation and energy supply risk: Operation Epic Fury has already halted most tanker traffic through the Strait of Hormuz, pushed oil prices higher by more than 8 percent in weekend trading, and opened the door to a potential move toward 100 dollars per barrel for Brent if hostilities persist.

-

Policy uncertainty on tariffs and trade: The Supreme Court’s ruling against IEEPA‑based tariffs forced the administration to pivot toward Section 122 and Section 301 authorities, creating uncertainty over the future level and structure of U.S. tariffs at the same time that attention is now diverted to the Middle East conflict.

Market Recap

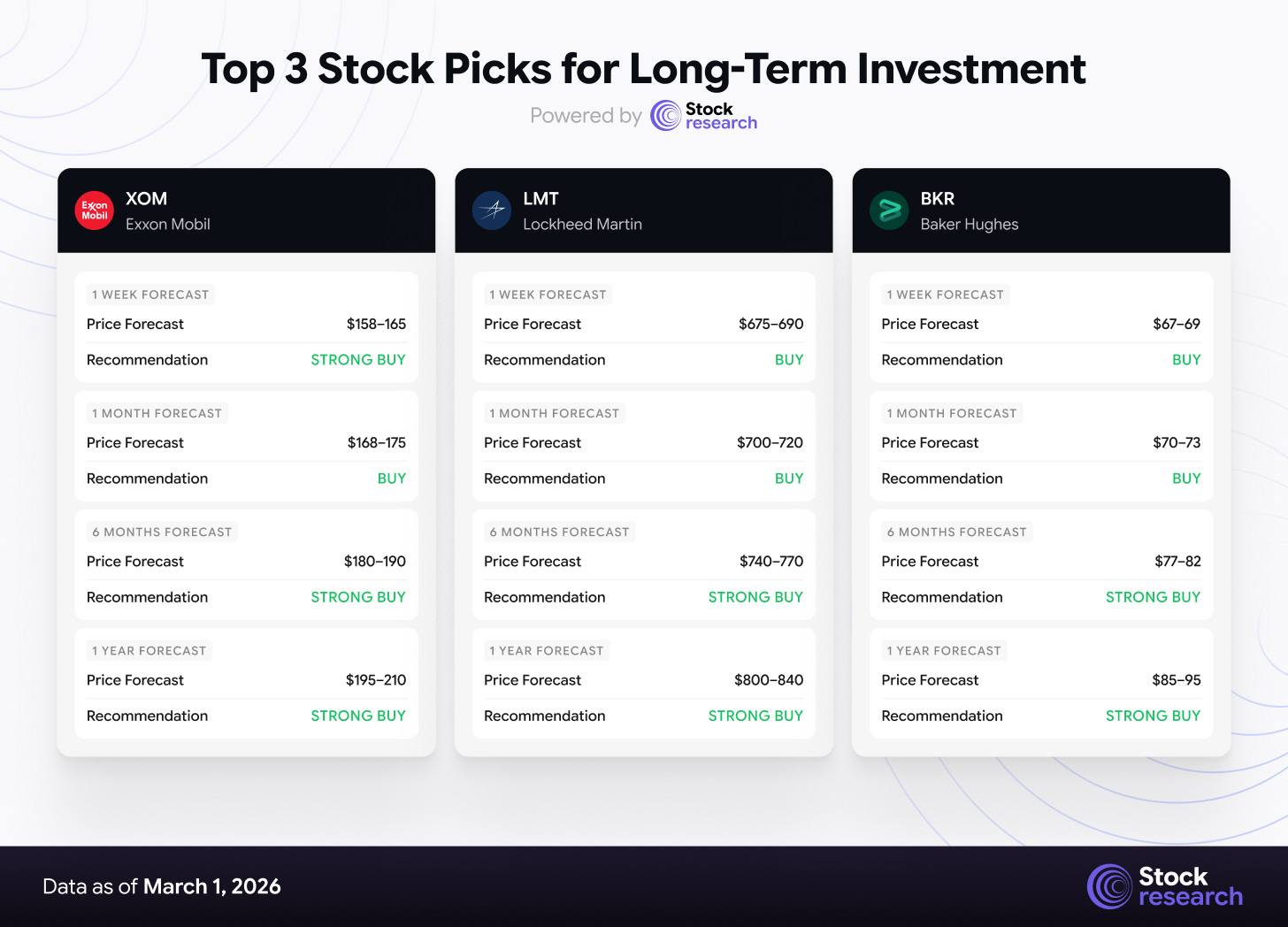

Top 3 Stock Picks for Long-Term Investment

1. Exxon Mobil (XOM) | Direct Beneficiary of Oil Risk Premium

Investment Horizon Recommendation:

-

1 Week: STRONG BUY (158–165 dollars; oil risk premium from Hormuz disruption likely to persist, energy inflows accelerating).

-

1 Month: BUY (168–175 dollars; Brent stabilizing above 85–90 dollars supports earnings revisions upward).

-

6 Months: STRONG BUY (180–190 dollars; sustained higher free cash flow and buybacks if geopolitical tension lingers).

-

1 Year: STRONG BUY (195–210 dollars; potential structural rerating if oil holds above 90 dollars and capital discipline remains intact).

Thesis: Exxon is the most direct large-cap U.S. beneficiary of the Iran–Hormuz crisis. Roughly 20 percent of global oil flows through the Strait of Hormuz, and even partial disruption introduces a structural risk premium into crude pricing.

Unlike many mid-cap energy names, Exxon combines:

-

Upstream exposure to higher realized prices

-

Downstream integration that protects margins

-

A fortress balance sheet

-

Aggressive buybacks and dividend support

At ~152 dollars, Exxon trades at a reasonable forward multiple relative to expected free cash flow expansion if Brent sustains 85–95 dollars. Every 5–10 dollar increase in crude meaningfully expands operating cash flow, which management has historically returned via buybacks.

Importantly, Exxon is not dependent on consumer discretionary demand. In a stagflationary scenario (higher oil + slower growth), energy majors often outperform the broader S&P 500.

Catalysts:

-

Sustained oil above 85–90 dollars due to Hormuz instability.

-

Institutional rotation into energy as AI trades cool.

-

Accelerated buybacks from elevated free cash flow.

-

Upward earnings revisions if Q1 reflects higher realized pricing.

Risks:

-

Rapid de-escalation in the Middle East that removes oil premium.

-

Demand destruction if oil spikes above 110 dollars.

-

Political pressure (windfall tax rhetoric).

-

Broader equity selloff dragging cyclicals temporarily lower.

2. Lockheed Martin (LMT) | Geopolitical Hedge With Cash Flow Visibility

Investment Horizon Recommendation:

-

1 Week: BUY (675–690 dollars; defense bid likely to strengthen as war headlines dominate).

-

1 Month: BUY (700–720 dollars; Pentagon budget revisions and missile defense demand support near-term momentum).

-

6 Months: STRONG BUY (740–770 dollars; multi-year defense spending acceleration cycle).

-

1 Year: STRONG BUY (800–840 dollars; backlog growth and sustained global rearmament trend).

Thesis: Lockheed is the cleanest large-cap U.S. defense exposure during geopolitical escalation. The Iran conflict reinforces a broader global rearmament theme that has been building since 2022.

LMT’s advantages:

-

Massive backlog with multi-year revenue visibility.

-

Exposure to missile defense systems and advanced fighter platforms.

-

Strong dividend yield (~2.7% range).

-

Government contracts largely insulated from consumer slowdown.

Unlike high-multiple tech stocks, Lockheed trades on a moderate earnings multiple relative to predictable cash flows. In a risk-off environment, defense often acts as a quasi-defensive growth sector.

If the Iran conflict expands, NATO and regional allies are likely to accelerate procurement — particularly missile interception systems, surveillance, and air superiority programs.

Catalysts:

-

Supplemental U.S. defense spending tied to Middle East operations.

-

NATO allies increasing procurement commitments.

-

New missile defense contracts.

-

Upward backlog guidance in future earnings calls.

Risks:

-

Political shifts leading to budget constraints.

-

Cost overruns on major programs.

-

Rapid ceasefire reducing perceived urgency.

-

Market rotation back into high-beta tech reducing relative appeal.

3. Baker Hughes (BKR) | High Beta Play on Energy Capex Cycle

Investment Horizon Recommendation:

-

1 Week: BUY (67–69 dollars; oil services rotation as drilling expectations rise).

-

1 Month: BUY (70–73 dollars; LNG and international contracts support momentum).

-

6 Months: STRONG BUY (77–82 dollars; energy capex acceleration and LNG buildout).

-

1 Year: STRONG BUY (85–95 dollars; margin expansion and structural LNG demand).

Thesis: Baker Hughes is a leveraged play on the second-order effect of higher oil prices: capital expenditure.

When oil rises, integrated majors like Exxon benefit first. The next phase is increased drilling activity, LNG investment, and infrastructure expansion — that’s where BKR comes in.

Key advantages:

-

Strong LNG turbine exposure.

-

Carbon capture and energy transition optionality.

-

International footprint.

-

Margin recovery story from prior cycle lows.

At ~$65, BKR is still well below historical peak cycle multiples relative to free cash flow potential if global drilling accelerates.

Unlike Exxon, BKR has more beta. If oil stays elevated for multiple quarters, services names tend to outperform producers on a percentage basis.

Catalysts:

-

Rising global rig counts.

-

LNG expansion projects (U.S., Qatar, Europe).

-

Contract wins in offshore and Middle East projects.

-

Improved margins in upcoming earnings cycles.

Risks:

-

Oil price spike followed by sharp correction.

-

Capex discipline from majors limiting drilling expansion.

-

Global recession reducing energy demand.

-

Execution risk on LNG and carbon capture projects.

Low-Cap Stock Opportunities: Undiscovered Value

The following three stocks represent overlooked opportunities in the sub-$10 billion market cap space, each benefiting from structural tailwinds that the geopolitical shock has now amplified.

Fluor Corporation (FLR)

Current Price: $52.31 | Market Cap: $7.67B | Sector: Industrials — Engineering & Construction

Fluor is widely mischaracterized as a traditional construction company, but its current positioning tells a different story. The company holds a ~39% stake in NuScale Power, the only U.S. company with an NRC-approved small modular reactor design. This stake, potentially worth $1–$2 billion upon monetization by mid-2026, could fund aggressive share buybacks. Fluor has transformed its risk profile by shifting 80–97% of new contracts to reimbursable terms, protecting margins from inflation risk.

The Iran conflict has supercharged the bull case. The prospect of prolonged Strait of Hormuz disruption and $80–$100 oil makes domestic energy infrastructure — particularly nuclear — a national security priority. Fluor serves as an EPC partner for hyperscale data center facilities requiring massive power infrastructure, and the nuclear renaissance driven by hyperscaler power purchase agreements, Trump’s pro-nuclear executive orders, and now energy security urgency positions the company as the essential “shovel in the boom”.

Why Now: Iran conflict accelerates domestic nuclear and energy infrastructure investment, NuScale monetization provides near-term catalyst, and $3B cash provides balance sheet strength in a risk-off environment.

Credo Technology Group (CRDO)

Current Price: $112.27 | Market Cap: $20.3B | Sector: Technology — Communication Equipment

Credo Technology provides the essential connectivity “plumbing” for AI data centers through its Active Electrical Cables (AECs) and SerDes chiplets. As AI clusters scale to hundreds of thousands of GPUs, network reliability, signal integrity, and power efficiency become critical bottlenecks — precisely the problems Credo’s products solve. The company’s ZeroFlap AECs offer reliability up to 1,000 times better than legacy interconnect solutions while consuming ~50% less power.

Revenue growth is explosive: analysts project Q3 FY2026 revenue of $406 million, a 51.5% quarter-over-quarter increase, driven by AEC demand from multiple hyperscalers. Gross margins stand at a robust 67%. The stock has pulled back ~47% from its 52-week high of $213.80, creating a potential entry point for investors willing to look past near-term sector volatility. Unlike consumer-facing tech, data center infrastructure spending is committed via multi-year contracts and is unlikely to be derailed by geopolitical events.

Why Now: Severe pullback from highs despite accelerating fundamentals, explosive revenue growth trajectory, and essential role in AI infrastructure that transcends geopolitical cycles.

TTM Technologies (TTMI)

Current Price: ~$98.77 | Market Cap: ~$9.94B | Sector: Technology — Electronic Components

TTM Technologies manufactures advanced printed circuit boards (PCBs) that serve as the hardware backbone of AI data centers, defense systems, and networking infrastructure. When hyperscalers like Alphabet commit $175–$185 billion in AI capex, companies like TTM provide the physical interconnect layer that makes GPU clusters function. Q4 CY2025 revenue grew 18.9% YoY to $774.3 million, beating estimates, and Q1 CY2026 guidance of $790 million was 7% above consensus.

TTM’s dual exposure to AI data centers and defense electronics makes it uniquely positioned for the current environment. The $924.7 billion NDAA for fiscal 2026 and the operational tempo of Operation Epic Fury will drive incremental demand for precision electronics in missile systems, radar, and communication equipment. The company is expanding manufacturing capacity with a new 750,000 sq ft facility in Wisconsin and additional capacity in Penang, Malaysia, specifically to serve AI PCB demand.

Why Now: Dual AI + defense tailwind uniquely suited for the current geopolitical environment, strong Q1 guidance, and expanding manufacturing capacity to capture both structural growth themes simultaneously.

Strategic Recap & Forward Outlook

Forward Outlook (Week Ending March 7, 2026)

The coming week will be dominated by a single variable: the trajectory of Operation Epic Fury and its impact on the Strait of Hormuz and global energy prices. Equity investors will also have to digest important macro data on growth and employment that will shape expectations for Federal Reserve policy in a world where oil has just staged a sudden spike.

Three variables will determine near‑term market direction:

-

Strait of Hormuz and oil prices:

If tanker traffic through the Strait resumes in the next several days and insurance markets stabilize, the weekend spike in WTI and Brent could retrace, easing fears of a 100‑dollar oil scenario and reducing the additional inflation premium priced into bonds. A prolonged shutdown, especially if accompanied by further strikes on Gulf oil infrastructure, would likely send Brent toward or above 100 dollars, push global inflation higher by up to 0.7 percentage points and force investors to price in a much more hawkish Fed path. -

Scope and duration of military operations:

Markets can sometimes look through short, contained conflicts but struggle with open‑ended engagements. If evidence emerges that Operation Epic Fury is transitioning from an intense first phase to a negotiated framework, risk assets could stabilize and sectors like technology might see a relief rally. Conversely, signs of broader regional escalation or direct attacks on additional U.S. assets would likely sustain or deepen the risk‑off tone, supporting Energy, Defense, Utilities and gold at the expense of growth equities. -

Macro data and Fed expectations:

This week’s ISM manufacturing and services surveys, ADP employment report and, most importantly, Friday’s Non‑Farm Payrolls release will either confirm or challenge the current view that the labor market is cooling only gradually while inflation remains above target. Any upside surprises on wages or employment would further complicate rate‑cut hopes in a world of higher oil, while weaker data could revive growth fears and strengthen the case for a more defensive equity posture.

Positioning guidance:

-

Overweight Energy and Defense; upgrade Utilities and Infrastructure:

Maintain or increase exposure to integrated oil, midstream and select refiners that benefit from higher crude prices, and to defense primes with large, visible backlogs and potential incremental demand from allies reacting to the conflict. Utilities and infrastructure names with stable cash flows, including NextEra, are increasingly attractive as yield plus growth vehicles in a volatile environment. -

Favor tangible AI infrastructure over speculative AI narratives:

Continue to focus on companies with clear, near‑term AI revenue such as Dell, AMD and select hardware, connectivity and PCB suppliers rather than on software names whose business models may be undermined by AI agents. The selloff in high‑multiple software should be treated with caution until valuations and expectations reset further. -

Use volatility to scale into quality over time, not all at once:

Elevated weekend risk and headline sensitivity argue for staggered entries rather than aggressive, single‑day deployments. Investors with multi‑year horizons can gradually build positions in structurally advantaged names like Dell, NextEra, AMD, Fluor, Credo and TTM, while maintaining some cash and short‑duration fixed income as dry powder.

Sentiment has shifted decisively away from complacency as AI euphoria, inflation anxiety and now war risks intersect, but periods of fear have historically created attractive entry points into high‑quality assets for patient capital. The key in the current environment is to distinguish between companies that sit at the heart of enduring trends, such as AI compute, power and security, and those whose growth was more a function of cheap capital and narrative momentum. The former can be accumulated selectively on weakness; the latter may remain under pressure for some time.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.