StockResearch Intelligence Weekly #6

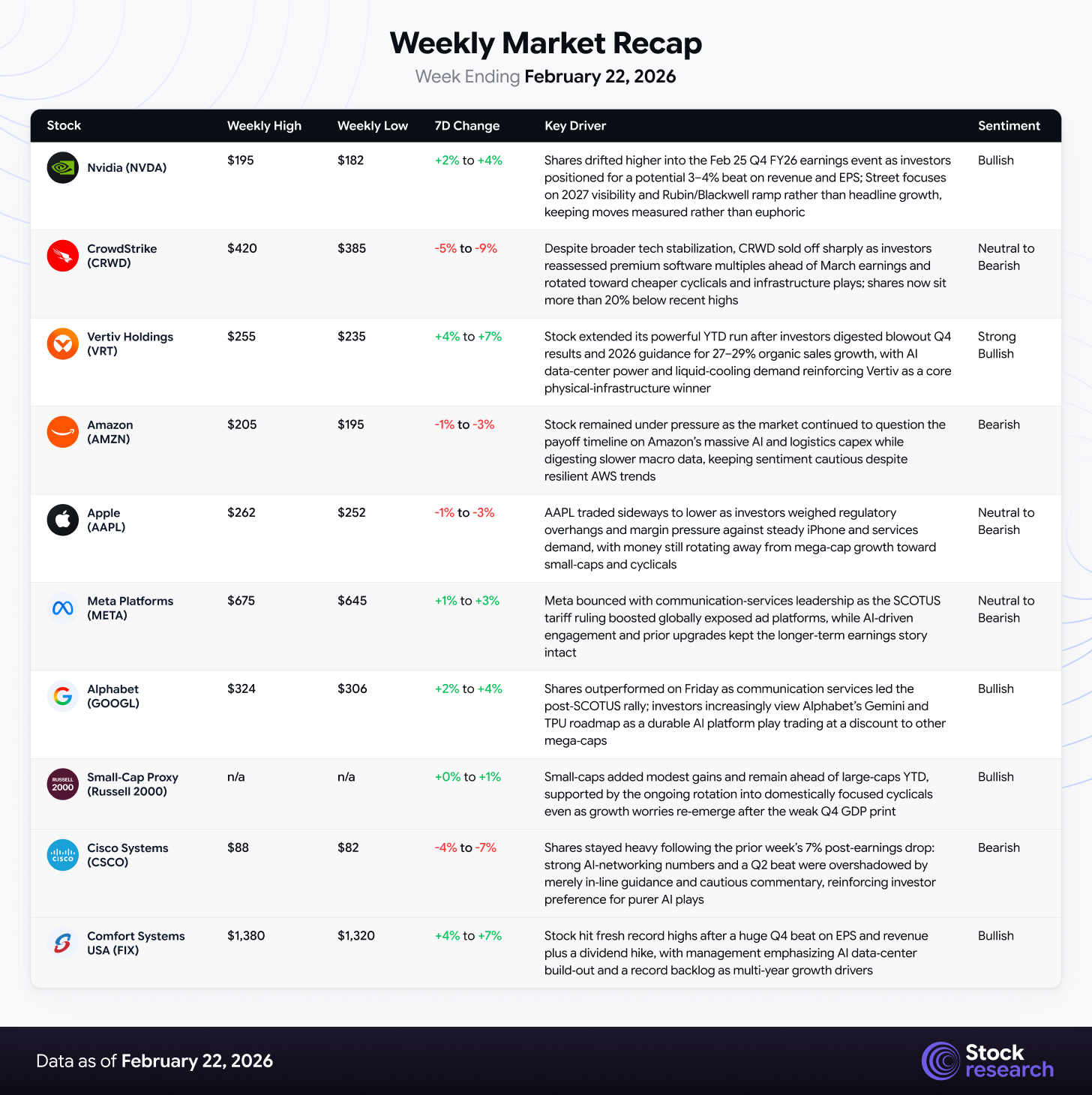

During February 17–21, 2026, U.S. equities staged a meaningful recovery in a shortened holiday week, with the S&P 500 gaining 1.08% to close at 6,909.51, the Nasdaq snapping its five-week losing streak with a 1.51% advance to 22,886.07, and the Dow adding 0.25% to 49,625.97. Three crosscurrents defined the week: the Supreme Court’s landmark 6-3 ruling striking down IEEPA tariffs on Friday, a deeply disappointing Q4 2025 GDP print of just 1.4% annualized, badly missing the 2.5% consensus, and cyclical sector rotation that lifted Industrials, Energy, and Financials each more than 1.5%.

The rally was constructive but selective. Mega-cap tech stabilized after weeks of selling, with the PHLX Semiconductor Index gaining 1.5% and the Vanguard Mega Cap Growth ETF rising 1.5% on the week. However, the iShares Expanded Tech-Software ETF fell another 2.4%, confirming the market’s ongoing bifurcation between hardware/infrastructure winners and software companies facing AI disruption headwinds. The CNN Fear & Greed Index improved to 43 (Fear) from 37 the prior week, while the VIX dipped below the critical 20 level for the first time in two weeks.

Strengths

-

SCOTUS tariff relief: 6–3 ruling strikes down IEEPA tariffs, sparking a relief rally in trade‑sensitive and communication‑services names, before Trump’s Section 122 pivot caps gains.

-

Cyclical rotation broadens breadth: Industrials, Energy, and Financials each gain ~1.6–1.7% on the week, while equal‑weight indices outperform, confirming rotation away from mega‑cap tech concentration.

-

Comfort Systems USA blowout: FIX posts a huge Q4 beat (EPS $9.37 vs $6.75, revenue +41.7% YoY) and raises its dividend, underscoring accelerating AI data‑center construction demand.

Weaknesses

-

GDP growth disappoints: Q4 2025 GDP slows to 1.4% vs 2.5% expected (from 4.4% in Q3), with the government shutdown shaving ~1.5ppt off growth and raising slowdown concerns.

-

Sticky PCE inflation: Headline PCE at 2.9% and core at 3.0% keep inflation above the Fed’s 2% target, tempering rate‑cut hopes despite prior CPI relief.

-

High‑multiple software under pressure: CrowdStrike slides to ~22% below its high and ~18% YTD down as investors question premium software valuations in an AI‑disruption environment.

Market Recap

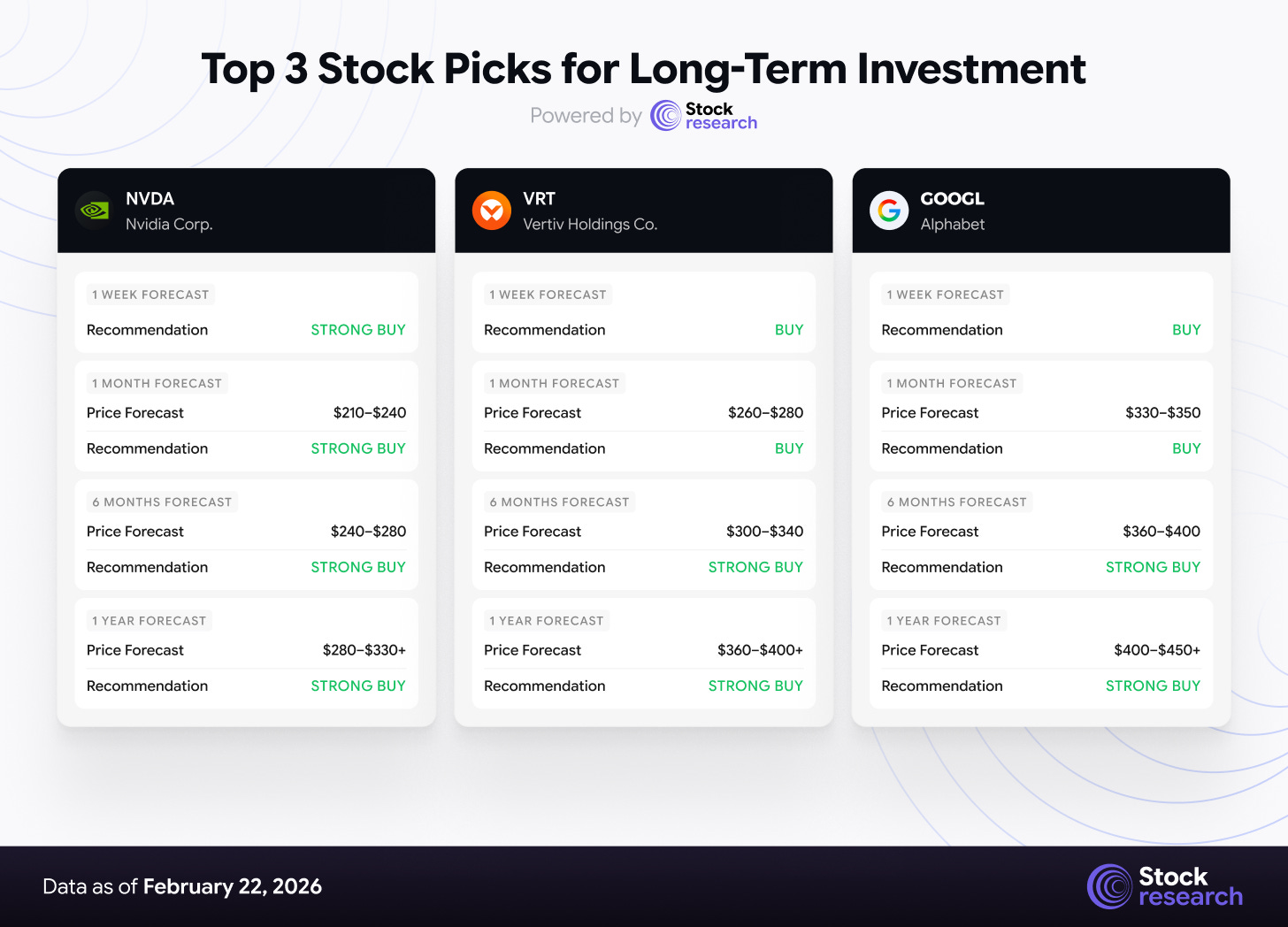

Top 3 Stock Picks for Long-Term Investment

1. Nvidia (NVDA) | The Earnings Catalyst at the AI Epicenter

Investment Horizon Recommendation:

-

1 Week: STRONG BUY (pre-earnings positioning; Feb 25 Q4 FY2026 report is the most important event of the quarter)

-

1 Month: STRONG BUY ($210–$240; beat-and-raise cycle expected to reignite AI infrastructure optimism)

-

6 Months: STRONG BUY ($240–$280; Blackwell/Rubin revenue acceleration plus GTC 2026 catalysts)

-

1 Year: STRONG BUY ($280–$330+; structural beneficiary of $600B+ annual hyperscaler AI capex)

Thesis: Nvidia enters its most consequential earnings week of the year trading at $189.82, up 3.55% over the past four weeks but still approximately 10.5% below its 52-week high of $212.19. The February 25 Q4 FY2026 earnings report is consensus-expected to show EPS of $1.52 (+71% YoY) and revenue of $65.47 billion (+66.5% YoY). Goldman Sachs analyst Jim Schneider projects revenue closer to $67.3 billion, above the Street, citing steady demand signals from chip suppliers and elevated hyperscaler capex plans. RBC Capital expects a 3–4% beat-and-raise and anticipates management will increase the prior $500B+ backlog figure.

The critical differentiator this quarter is that investors are looking past 2026 and demanding visibility into 2027, specifically Rubin ramp timing, China contribution, non-hyperscaler customer traction, and sustainable margin expansion. Nvidia’s P/E of 47x trailing earnings is elevated but justified by the structural growth trajectory, with Q3 FY2026 already delivering record revenue of $57 billion (+62% YoY) and data center revenue of $51.2 billion.

Catalysts:

-

Q4 FY2026 earnings on February 25, consensus expects a significant beat-and-raise

-

GPU Technology Conference (GTC) 2026 expected to showcase Rubin architecture details

-

Hyperscaler AI capex commitments exceeding $500B in 2026 from Google, Amazon, Meta, and Microsoft

-

Blackwell-trained frontier model launches expanding inference demand

Risks: Post-earnings “sell the news” reaction given elevated expectations; China export control uncertainty; margin compression from surging memory prices (though RBC believes Nvidia has locked in 2026 HBM pricing); competitive pressure from custom ASICs at Google and Amazon.

2. Vertiv Holdings (VRT) | Physical AI Infrastructure Powerhouse Extending Its Lead

Investment Horizon Recommendation:

-

1 Week: BUY ($243.75 entry; post-earnings consolidation with strong support at $235)

-

1 Month: BUY ($260–$280; record backlog conversion accelerating into Q1 2026 revenue)

-

6 Months: STRONG BUY ($300–$340; 2026 guidance of 27–29% organic growth executing ahead of plan)

-

1 Year: STRONG BUY ($360–$400+; multi-year data center power/cooling demand cycle extending)

Thesis: Vertiv has been the standout performer of early 2026, surging 48% year-to-date to $243.75 as the market increasingly recognizes that AI’s physical infrastructure layer cannot be disrupted, only expanded. The stock has rallied from $164.69 at the start of the year to record levels above $255 intraweek, propelled by Q4 2025 results that delivered organic orders growth of 252%, adjusted operating margin of 23.2%, and adjusted EPS of $1.36.

The 2026 guidance is where the thesis truly accelerates: net sales of $13.25–$13.75 billion (27–29% organic growth), adjusted diluted EPS of $5.97–$6.07, and adjusted free cash flow of $2.2 billion. With AI-specific data center clusters requiring 120–150kW per rack (up from 10–15kW just three years ago), Vertiv’s power distribution, thermal management, and liquid cooling solutions sit at the critical bottleneck of the entire AI infrastructure buildout.

Vertiv’s market capitalization has reached approximately $93 billion, reflecting an enormous re-rating from $42.6 billion a year ago. While the valuation is no longer cheap, the growth trajectory justifies the premium, particularly with the Americas segment growing 46% organically, the highest-margin geography in the portfolio.

Catalysts:

-

Record backlog converting to production revenue throughout 2026–2027

-

Liquid cooling and AI-specific thermal solutions commanding premium pricing

-

Capacity expansion to meet surging hyperscaler and enterprise demand

-

Potential upward earnings revisions as 2026 unfolds

Risks: Premium valuation leaves limited margin for error; execution risk on capacity expansion and supply chain bottlenecks; concentration risk around hyperscaler customers; EMEA weakness could persist; consensus analyst target of $216.87 sits below the current price, implying the stock has run ahead of most analysts.

3. Alphabet (GOOGL) | The AI Platform Giant at an Inflection Point

Investment Horizon Recommendation:

-

1 Week: BUY (SCOTUS tariff ruling tailwind; communication services led Friday’s rally)

-

1 Month: BUY ($330–$350; search/cloud AI integration deepening; undervalued relative to mega-cap peers)

-

6 Months: STRONG BUY ($360–$400; Gemini 2.0 monetization ramping; YouTube and Cloud accelerating)

-

1 Year: STRONG BUY ($400–$450+; dominant position across search, cloud, and AI model development)

Thesis: Alphabet closed the week as one of Friday’s top performers, gaining 3.9% on the session as communication services led the market’s post-SCOTUS rally. The stock has shown remarkable resilience during the recent tech selloff, with Alphabet uniquely positioned as both an AI infrastructure investor (through Google Cloud and TPU development) and an AI application beneficiary (through Search, YouTube, and Gemini).

Unlike peers facing AI disruption risk, Alphabet’s core search business is being strengthened by AI through Search Generative Experience and Gemini integration, not threatened by it. Google Cloud continues to gain market share with AI-driven enterprise workloads, and YouTube’s advertising revenue benefits from AI-driven content recommendation improvements. At approximately $314, the stock trades at a reasonable valuation relative to its growth profile and massive free cash flow generation.

The SCOTUS tariff ruling provides a near-term catalyst, as Alphabet’s global advertising business benefits from reduced trade friction. The company’s position as the leading developer of both AI models (Gemini) and custom AI silicon (TPU) gives it a structural advantage that few competitors can match.

Catalysts:

-

Post-SCOTUS tariff relief benefiting global advertising revenue

-

Gemini 2.0 integration across Google products driving engagement and monetization

-

Google Cloud AI services accelerating enterprise adoption

-

YouTube premium and advertising revenue growth from AI-enhanced recommendations

Risks: Regulatory pressure from DOJ antitrust case and global competition authorities; potential ad market slowdown if economic deceleration deepens; competition from OpenAI/Microsoft in AI model development; capital intensity of AI infrastructure investments pressuring free cash flow margins.

Low-Cap Stock Opportunities: Undiscovered Value

The Physical Infrastructure & AI Data Rotation: Finding Alpha in Overlooked Names

The market’s recovery week further cemented the rotation into physical-world assets and companies with tangible infrastructure moats. The Nasdaq’s five-week losing streak snapped not because software rebounded, the tech-software ETF fell another 2.4%, but because semiconductor, industrial, and energy stocks caught bids. Three structural forces continue to support selective positioning in smaller-cap names:

-

AI Power Demand Is Becoming the Binding Constraint: McKinsey projects U.S. data center electricity consumption will rise from 147 terawatt-hours to over 600 TWh by 2030. Companies that provide power generation, fuel cells, and grid solutions for data centers are experiencing secular demand acceleration that traditional utility investors never anticipated.

-

GDP Deceleration Favors Companies With Non-Cyclical Demand Drivers: With Q4 GDP at just 1.4% and consumer sentiment weakening, companies whose revenue growth is tied to structural AI infrastructure spending rather than consumer discretionary are increasingly attractive.

-

Small/Mid-Cap Valuation Gap Persists: The Russell 2000 remains up 7.3% year-to-date versus the S&P 500’s 0.9%, and earnings growth projections for small caps continue to significantly exceed large-cap forecasts. JPMorgan continues to call this “the best stockpicking era” for smaller companies.

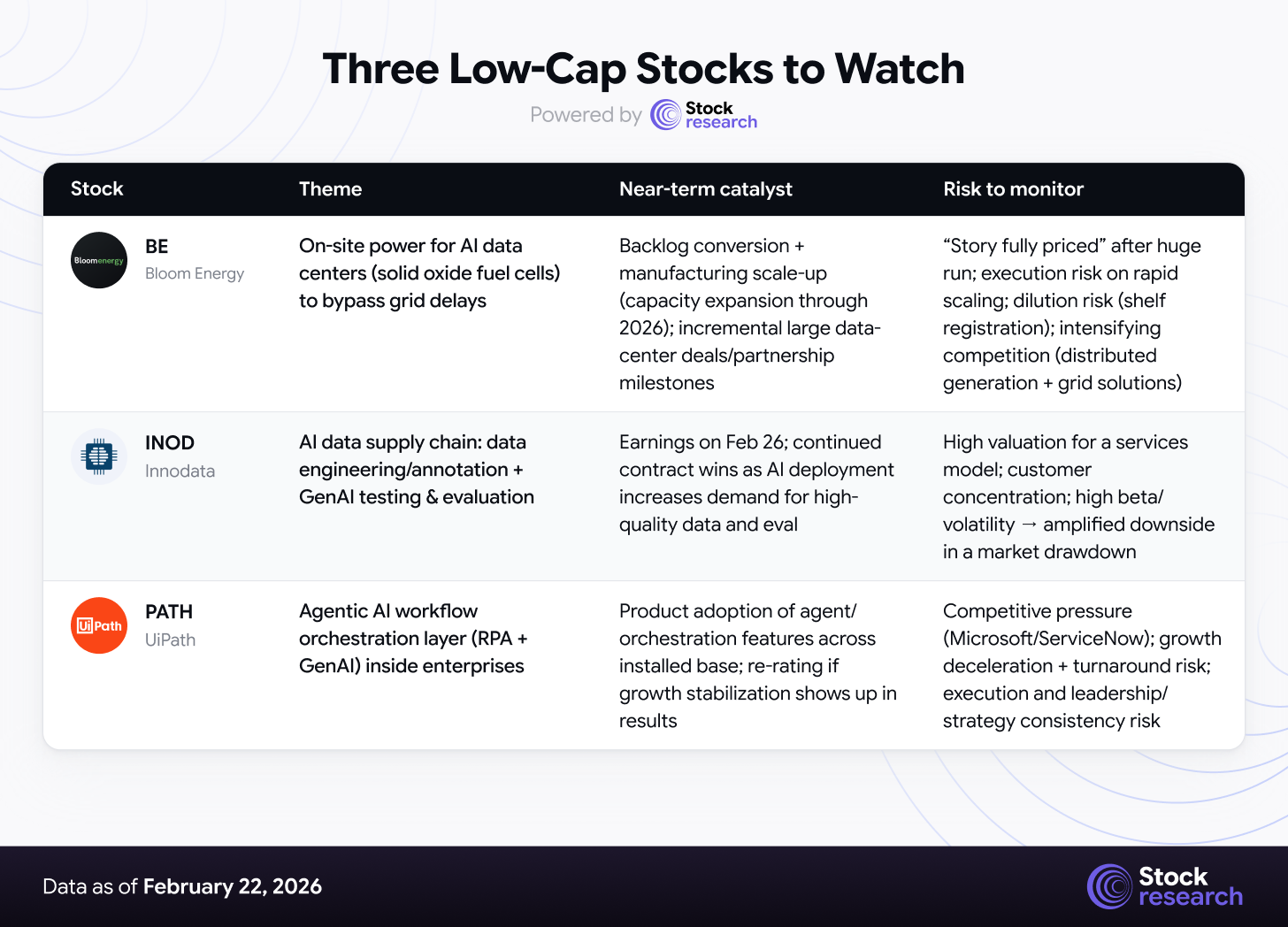

Three Low-Cap Stocks to Watch

1. Bloom Energy (BE) | ~$23B Market Cap

On-site power generation company specializing in solid oxide fuel cell technology, rapidly becoming the go-to provider for data center power solutions that bypass traditional utility grid delays. Bloom Energy closed at $147.55, up 49.5% year-to-date and 510.5% over the past 12 months.

Why it matters: Bloom Energy sits at the intersection of the two most powerful investment themes of 2026: AI data center power demand and energy infrastructure independence. The company has secured a multibillion-dollar partnership with Brookfield Asset Management, an Oracle partnership for on-site data center power, and collaboration with American Electric Power to expand distributed generation capacity. With a reported $20 billion backlog and plans to double manufacturing capacity by end of 2026, Bloom is transitioning from a niche fuel cell company to a critical infrastructure provider for the AI economy.

The company guided 2026 revenue of $3.1–$3.3 billion and has returned to profitability, validating its business model at scale. A key January catalyst was the approval of a 900 MW fuel cell project in Wyoming, which analysts characterized as a “major” revenue addition.

Key risks: The stock has already experienced a massive rally (510% in 12 months), and some analysts maintain Underperform ratings, suggesting the AI data center story may be fully priced in at current levels. Execution risk on capacity doubling is significant. Competition from Caterpillar’s distributed generation, Siemens Energy’s grid solutions, and hydrogen-focused peers is intensifying. A $2.13 billion shelf registration raises dilution concerns.

2. Innodata (INOD) | ~$1.4B Market Cap

Data engineering and AI services provider that has positioned itself as a critical partner in the AI supply chain, offering high-quality data annotation, preparation, and testing services for training advanced language models. Shares trade near $44.50, with a consensus “Strong Buy” rating and an average price target of $91.67, implying over 100% upside.

Why it matters: While the market obsesses over AI chip makers and infrastructure providers, Innodata addresses an equally critical bottleneck: the data quality required to train and fine-tune large language models. The company has delivered extraordinary revenue growth of 73.6% year-over-year (trailing twelve months), reaching $238.5 million, while maintaining profitability with $33.6 million in net income. Its GenAI Test and Evaluation Platform, built using Nvidia microservices, enables testing for hallucinations, adversarial prompts, and reliability assessments, a capability that becomes more valuable as AI agent deployment accelerates.

Innodata reports earnings on February 26, creating a near-term catalyst. With a market cap of just $1.4 billion and a beta of 2.42, this is a high-volatility name, but the structural demand for AI data services is undeniable as every new foundation model and enterprise AI deployment requires massive amounts of curated, annotated data.

Key risks: Elevated valuation (P/E ~57x) for what remains a services business with competitive pressure from larger IT service providers. Revenue concentration risk around a small number of large tech clients. The stock has declined from its 52-week high of $93.85, indicating profit-taking. High beta means amplified downside in a broad market selloff.

3. UiPath (PATH) | ~$7.5B Market Cap

Enterprise automation platform provider that is integrating generative AI and agentic AI capabilities into its robotic process automation (RPA) suite, positioning itself as the orchestration layer between AI agents and enterprise workflows. UiPath carries a Zacks Rank #1 (Strong Buy) and is highlighted by multiple analysts as an undervalued mid-cap AI infrastructure play.

Why it matters: As the AI narrative evolves from “AI replaces software” to “AI agents need orchestration,” UiPath is emerging as a potential beneficiary rather than a victim of AI disruption. The company’s platform orchestrates automated workflows across enterprise applications, and its new generative AI features, including specialized LLMs (DocPATH, CommPATH) and Context Grounding capabilities, position it as the middleware between autonomous AI agents and legacy enterprise systems.

The “AI agent orchestration” theme is nascent but potentially transformative. Every autonomous AI agent deployed across finance, healthcare, legal, and consulting needs a platform to manage workflows, ensure compliance, and integrate with existing business systems. UiPath’s installed base of enterprise automation customers provides a natural distribution channel for these capabilities.

Key risks: UiPath has struggled with growth deceleration and management turnover in recent quarters. Competition from Microsoft Power Automate, ServiceNow, and other enterprise automation players is intense. The stock underperformed significantly in 2025, and a turnaround is not guaranteed. Revenue growth must reaccelerate to justify the current valuation.

Strategic Recap & Forward Outlook

Forward Outlook (Week Ending February 28, 2026)

The coming week is dominated by a single event: Nvidia’s Q4 FY2026 earnings on Tuesday, February 25. The report will serve as a litmus test not just for Nvidia but for the entire AI infrastructure investment thesis. Goldman Sachs projects revenue of $67.3 billion (above the $65.47B consensus), and the market is pricing in a beat-and-raise cycle. The critical variable is not the Q4 numbers themselves but the forward guidance, specifically management’s visibility into 2027 revenue trajectories, Rubin architecture ramp timing, and non-hyperscaler customer diversification.

Three variables will determine near-term market direction:

-

Nvidia’s Post-Earnings Reaction: A strong beat with confident 2027 guidance could reignite risk appetite across the entire AI complex and push the S&P 500 toward the 6,960 all-time high resistance zone. A disappointing guide or a “sell the news” reaction would reinforce the cautious rotation away from mega-cap tech and likely push the VIX back above 20.

-

Section 122 Tariff Implementation (Feb 24): Trump’s 15% global tariff takes effect Monday under Section 122 authority, creating immediate uncertainty for importers and trade-sensitive sectors. The 150-day statutory cap limits the scope, but the near-term impact on supply chains and consumer prices could be significant. Markets have not yet fully priced this pivot.

-

Inflation Trajectory: With core PCE at 3.0% and the Cleveland Fed nowcasting February core PCE at 2.74%, the disinflation narrative is under pressure. Any further upside inflation surprises would push rate-cut expectations further into the future, challenging the bull case for rate-sensitive sectors and growth stocks.

Positioning guidance: Continue favoring AI infrastructure hardware and physical-layer providers (NVDA, VRT, BE) over software companies facing disruption risk. The Comfort Systems USA blowout and Vertiv’s sustained rally confirm that the physical buildout is accelerating. Cybersecurity leaders (CRWD, PANW) remain structurally attractive but face near-term valuation compression. Maintain elevated cash positions to deploy into any post-Nvidia earnings volatility and to capitalize on the inevitable market dislocations as Section 122 tariffs take effect.

Sentiment remains in “Fear” territory (CNN Fear & Greed Index at 43), which has historically coincided with tactical buying opportunities in fundamentally strong names. The VIX’s move below 20 suggests the panic floor has held, but the combination of stagflationary macro data and tariff uncertainty means volatility is far from over.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.