StockResearch Intelligence Weekly #4

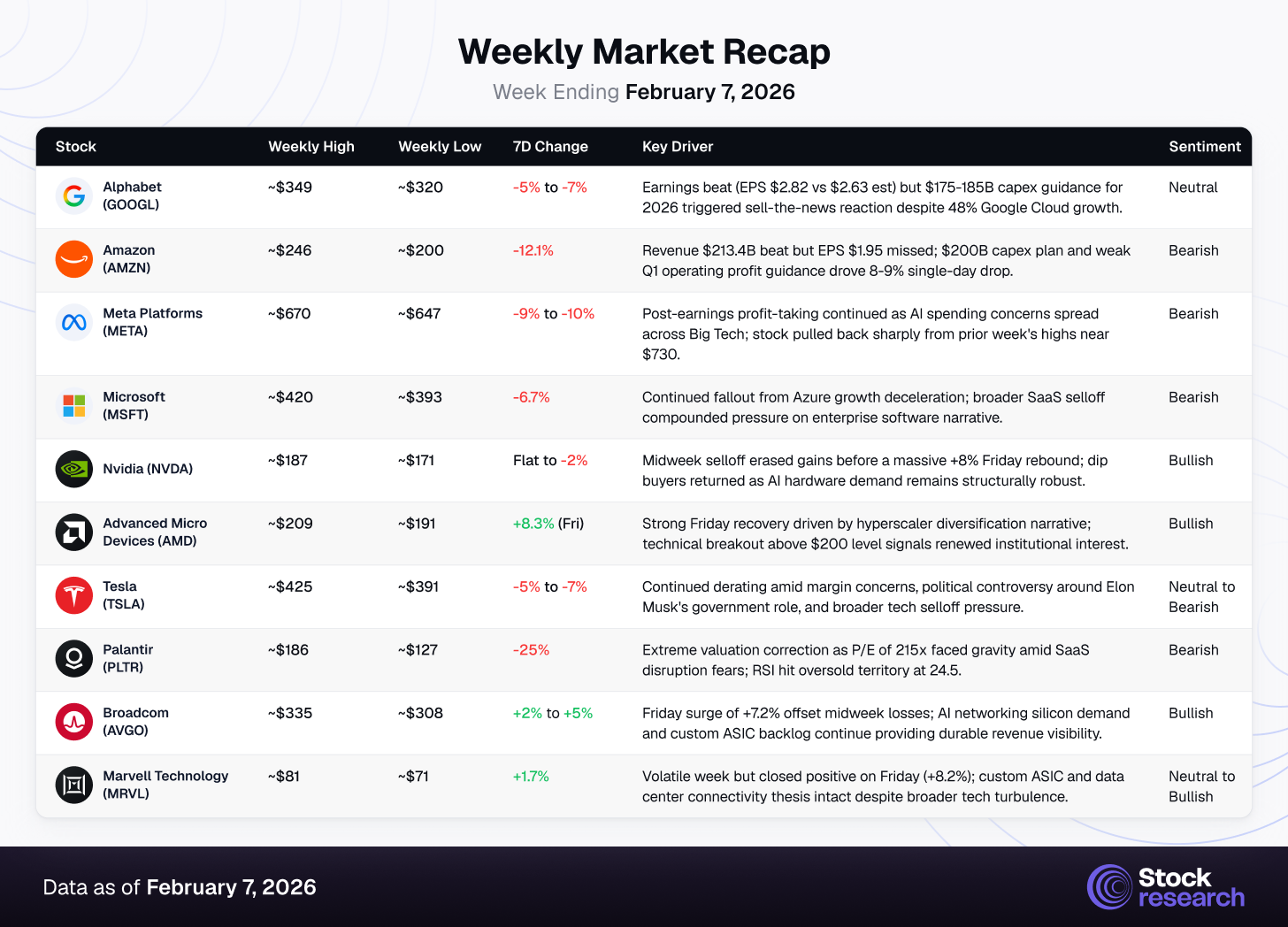

During the week of February 3–7, 2026, the US equity market experienced one of its most pronounced bifurcations in recent memory. The Dow Jones Industrial Average surged 2.5% to close above 50,000 for the first time in history at 50,116, driven by cyclical and value rotation into industrials, financials, and energy names. In stark contrast, the tech-heavy Nasdaq fell 1.8% on the week, battered by a cascading selloff in enterprise software stocks triggered by Anthropic’s Claude Cowork AI agent platform, which investors fear will render traditional SaaS business models obsolete. The S&P 500 finished effectively flat at 6,932, down just 0.1%, masking intense sector-level dispersion beneath the surface. The week was bookended by pivotal earnings from Alphabet and Amazon—both beat on revenue but alarmed investors with combined 2026 AI capital expenditure guidance exceeding $375 billion—and a Friday relief rally led by semiconductors, with Nvidia, AMD, and Broadcom each surging over 7%. The January jobs report showed 143K nonfarm payrolls (below the 170K consensus) with unemployment falling to 4.0%, reinforcing a “soft but not collapsing” labor narrative that keeps the Fed in wait-and-see mode. Market leadership decisively favored old-economy Dow components and defensive sectors, while high-multiple software, mega-cap tech guidance risk, and AI disruption fears dominated selling pressure.

Strengths

-

Dow Breaks Historic 50,000 Barrier: The Dow’s first-ever close above 50,000 signals sustained institutional rotation into value, cyclicals, and quality industrials—with Caterpillar (+7.1%), Goldman Sachs (+4.3%), and 3M (+4.5%) leading Friday’s rally.

-

Semiconductor Resilience Confirmed: Despite a brutal midweek selloff, Nvidia (+8%), AMD (+8.3%), and Broadcom (+7.2%) staged powerful Friday recoveries, confirming that AI infrastructure hardware demand remains structurally intact even as software faces disruption fears.

-

Google Cloud Growth Accelerating: Alphabet’s Google Cloud revenue surged 48% year-over-year to $17.7 billion, significantly beating estimates, with backlog doubling YoY to $240 billion—validating that enterprise AI adoption is accelerating beyond expectations.

Weaknesses

-

“SaaSpocalypse” Rattles Enterprise Software: Anthropic’s Claude Cowork plugins demonstrated autonomous AI agents capable of replacing traditional SaaS workflows, triggering a trillion-dollar selloff across the software sector. ServiceNow fell 7.6% to 52-week lows, and the Goldman Sachs Software Index (IGV) is now down 30% from October 2025 highs.

-

Amazon’s $200B Capex Plan Spooks Investors: Despite strong AWS growth of 24% and revenue of $213.4 billion, Amazon shares plunged ~12% on the week after the company announced approximately $200 billion in 2026 capital expenditure, raising concerns about free cash flow compression and return on invested capital.

-

Labor Market Softening Adds Uncertainty: January nonfarm payrolls of 143K fell below the 170K consensus, and ISM Services Employment dipped to 50.3 from 51.7, suggesting the labor market continues to cool—though upward revisions of +100K to prior months partially offset the headline miss.

Market Recap

The week highlighted a tectonic shift in market psychology: the era of “AI as copilot” is giving way to “AI as pilot,” where autonomous AI agents threaten to bypass—not enhance—traditional enterprise software platforms. This narrative shift triggered the most violent SaaS selloff since 2022, while simultaneously reinforcing the investment case for AI infrastructure hardware providers (semiconductors, networking silicon) and the hyperscalers building the physical compute layer. The Dow’s historic breach of 50,000 underscored that capital is rotating aggressively toward old-economy quality and value amid the tech disruption.

Top 3 Stock Picks for Long-Term Investment

Powered by StockResearch AI

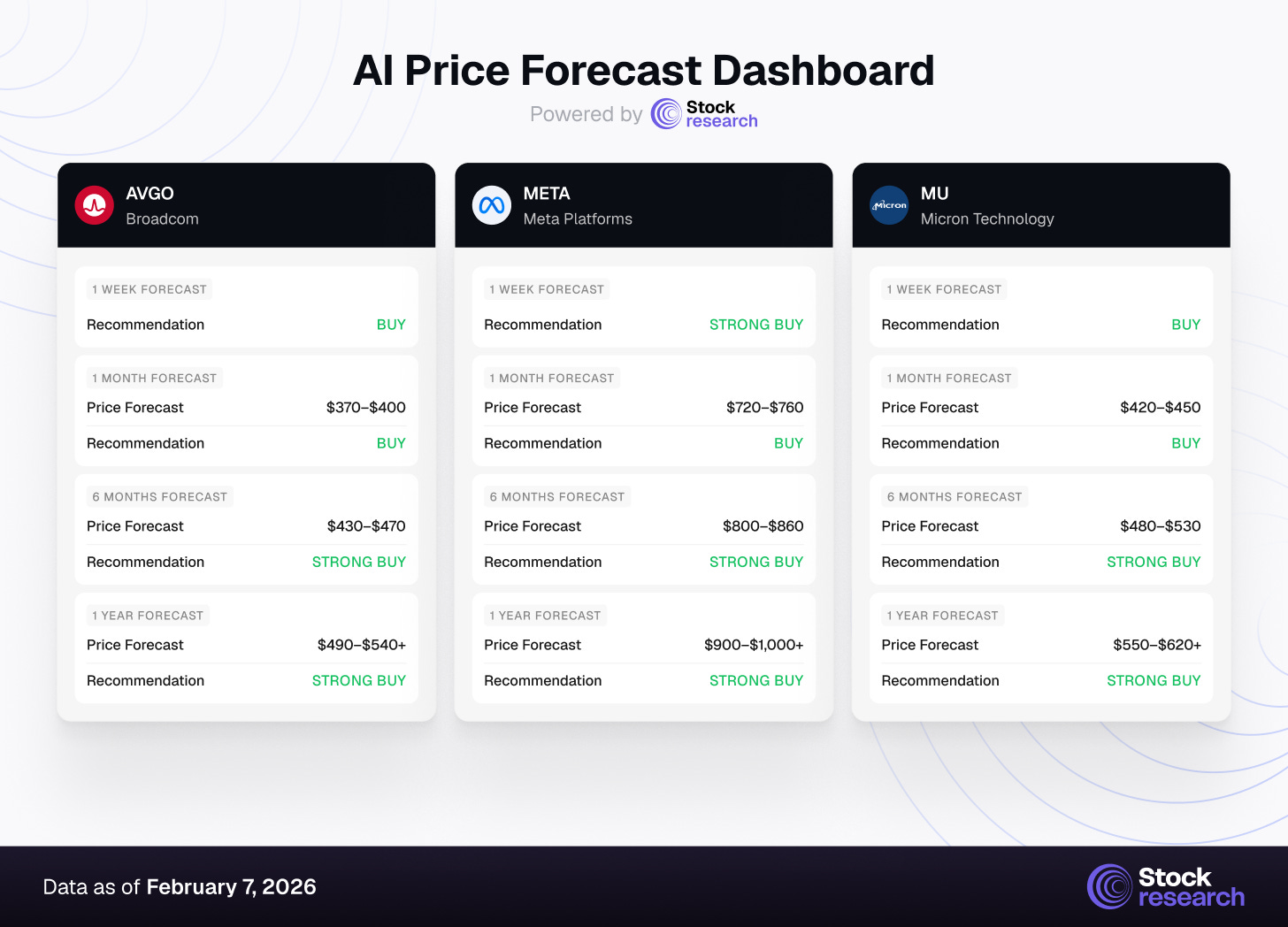

1. Broadcom (AVGO) | AI Custom Silicon & Networking Infrastructure Leader

Investment Horizon Recommendation:

-

1 Week: BUY (Friday’s +7.2% surge confirmed strong support at $308; Wolfe Research upgrade to Outperform)

-

1 Month: BUY ($370–$400; AI networking revenue momentum ahead of Q1 FY2026 earnings)

-

6 Months: STRONG BUY ($430–$470; custom ASIC backlog conversion accelerating; VMware synergies)

-

1 Year: STRONG BUY ($490–$540+; structural hyperscaler AI buildout beneficiary)

Thesis: Broadcom is the undisputed incumbent leader in custom AI accelerators and hyperscale networking silicon, with deep decade-long relationships across all major hyperscalers—most critically Google, which just announced $175–185 billion in 2026 AI capex. Broadcom secured $21 billion in orders from Google alone for custom TPU AI accelerators, and its AI revenue is guided at $8.2 billion for Q1 FY2026, representing 100% year-over-year growth. The company’s order backlog for AI solutions now stands at $73 billion over the next 18 months.

Friday’s 7.2% rally to ~$333 came after Wolfe Research upgraded the stock, citing Google’s massive capex commitment and Broadcom’s dominant role as custom silicon supplier. With analyst consensus target at $423 (27% upside) and 95% Buy ratings, the post-selloff entry point looks compelling.

Catalysts:

-

Custom ASIC backlog of $73B converting to production revenue through 2026–2027

-

AI networking silicon dominance: Tomahawk 5 commanding 70%+ market share in hyperscale Ethernet switching

-

VMware integration delivering cross-selling synergies and margin expansion

-

New undisclosed hyperscaler customer worth $10B+ in AI rack orders confirmed

Risks: Heavy dependence on a small group of hyperscaler customers (particularly Google), rising competition from Marvell in custom ASIC design, geopolitical risks around China AI chip export controls, and ongoing VMware integration execution risk.

2. Meta Platforms (META) | AI Monetization Powerhouse — Buy the Capex Fear Dip

Investment Horizon Recommendation:

-

1 Week: STRONG BUY (post-earnings pullback from $730 to $661 creates rare entry point)

-

1 Month: BUY ($720–$760; sentiment recovery as AI ad monetization narrative reasserts)

-

6 Months: STRONG BUY ($800–$860; Llama 4 launch + Advantage+ ad automation scaling)

-

1 Year: STRONG BUY ($900–$1,000+; AI monetization across 3.8B monthly active users)

Thesis: Meta’s 9–10% pullback from its post-earnings highs near $730 to $661 represents one of the best dip-buying opportunities in mega-cap tech this year. The company just delivered a blowout Q4 with 20.6% revenue growth and demonstrated that AI-driven advertising is not a future promise but a present reality—AI-powered ad tools increased user engagement by 5% on Facebook and 10% on Threads. Despite this, the stock sold off alongside the broader tech rout driven by AI capex fears, creating a mispriced entry.

At approximately 22x forward 2026 earnings, Meta trades at a significant discount to its Magnificent 7 peers relative to growth. The average analyst price target stands at $838 (27% upside), with 93% of analysts rating the stock a Buy. Baird’s Colin Sebastian maintains an Outperform rating with an $815 target, while the highest Street target is $1,144.

Catalysts:

-

Llama 4 launch in early 2026 expected to catalyze re-rating of Meta’s AI capabilities

-

Advantage+ ad automation expanding advertiser adoption and improving ROAS

-

Ray-Ban Meta smart glasses tripling in sales; 10M units projected in 2026

-

WhatsApp business monetization through AI-powered customer service tools

Risks: $103B+ 2026 capex plan compresses near-term free cash flow, Reality Labs continues to bleed losses ($70B+ cumulative), YouTube competitive pressures on Reels ad inventory, and regulatory scrutiny in the EU and US.

3. Micron Technology (MU) | The AI Memory Bottleneck Play

Investment Horizon Recommendation:

-

1 Week: BUY (strong +4.5% Friday recovery to $395; dip buyers defending $370 support)

-

1 Month: BUY ($420–$450; HBM supply constraints tightening; data center memory demand)

-

6 Months: STRONG BUY ($480–$530; HBM3E and HBM4 production ramp; memory upcycle)

-

1 Year: STRONG BUY ($550–$620+; structural AI memory beneficiary; new Singapore fab)

Thesis: Micron is the most mispriced AI infrastructure play in the market. While investors obsess over GPU providers, the reality is that the most expensive component in a top-tier AI GPU is not the processor die—it’s the high-bandwidth memory (HBM) and advanced packaging, which can account for approximately two-thirds of the bill of materials. Micron is one of only three companies globally (alongside SK Hynix and Samsung) capable of manufacturing the HBM chips that Nvidia, AMD, and every custom ASIC requires.

The stock’s volatile week—swinging from $442 to $366 before recovering to $395—reflects the market processing conflicting signals: Semianalysis cut Micron’s HBM4 share forecast for Nvidia, but Amazon’s $200B capex plan and broader hyperscaler spending more than offset any single-customer risk. Micron has already locked in price and volume agreements for its entire calendar 2026 HBM supply, confirming demand far exceeds available capacity. At 37.5x P/E with revenue growing 242% over the past year and a new $24B Singapore fab under construction, Micron offers the best “picks and shovels” memory exposure to the AI buildout.

Catalysts:

-

Amazon’s $200B capex plan directly benefits data center memory demand

-

Entire 2026 HBM supply already contracted at favorable pricing

-

$24B Singapore advanced wafer fab announced—scaling HBM and NAND capacity through 2028

-

HBM3E memory deployed in AMD’s latest AI accelerators, diversifying customer base

Risks: Potential loss of Nvidia HBM4 orders to SK Hynix (Semianalysis report), cyclical memory pricing risk, $24B fab execution risk with extended 2028 timeline, and competition from Samsung’s aggressive HBM capacity expansion.

Low-Cap Stock Opportunities: Undiscovered Value

The SaaS Disruption Rotation: Finding Value in the Wreckage

This week’s “SaaSpocalypse”—triggered by Anthropic’s Claude Cowork autonomous AI agent plugins—has created the most significant dislocation in software and technology valuations since 2022. The Goldman Sachs Software Index (IGV) is now down 30% from its October 2025 highs, and the S&P 500 Information Technology sector shed nearly 3% in a single session. While the panic is understandable—Claude’s ability to autonomously execute legal, financial, and CRM workflows directly threatens SaaS licensing models—the selloff has been indiscriminate, creating opportunities in stocks that are either insulated from AI substitution risk or actively positioned to benefit from the disruption.

Three structural factors favor selective small-cap and mid-cap positioning:

-

Valuation Dislocation Widening: The SaaS selloff has compressed multiples across the technology sector broadly, dragging down companies with limited AI substitution exposure purely through index-level selling pressure.

-

Defense and Physical Operations Immune to AI Software Disruption: Companies operating in defense hardware, semiconductor equipment, and physical-world IoT platforms face minimal risk from Claude-style AI agents that primarily target knowledge-worker workflows.

-

Quality Small-Caps Benefiting from Rotation: As capital exits high-multiple software, it flows into quality industrials, defense contractors, and niche technology providers with real asset bases and tangible revenue streams.

Three Low-Cap Stocks to Watch

1. BigBear.ai Holdings (BBAI) | ~$2.1B Market Cap

Defense-focused AI orchestration company building autonomous systems coordination platforms (ConductorOS, VANE) directly for the Pentagon and intelligence community. BBAI surged 15.7% on Friday alone, signaling growing investor recognition of its pure-play positioning within the expanding defense AI budget.

Why it matters: BBAI is one of the few publicly traded pure-play defense AI stocks, directly aligned with the Pentagon’s $13B+ autonomous systems budget. Its ConductorOS platform orchestrates drones, satellites, and sensors into a unified operational picture—a capability that becomes increasingly critical as Trump’s proposed $1.5T defense budget prioritizes next-generation warfare.

Key risks: The company is deeply unprofitable (net loss of $426M on just $144M revenue), making it a speculative play. Share price volatility is extreme (beta 3.21), and the stock is trading at a 553% premium to Morningstar’s fair value estimate of $3.87.

2. Axcelis Technologies (ACLS) | ~$2.6B Market Cap

Ion implantation equipment manufacturer serving the semiconductor fabrication industry, recently approved for merger with Veeco Instruments. ACLS is a direct “picks and shovels” beneficiary of the massive AI chip capex cycle, as every advanced GPU and ASIC requires ion implantation during fabrication.

Why it matters: With hyperscalers committing $500B+ to AI infrastructure in 2026, semiconductor equipment makers like Axcelis benefit from the downstream capex multiplier effect. The company just launched its Purion H6 next-generation high-current ion implanter and received stockholder approval for its Veeco merger, creating a more diversified equipment platform.

Key risks: Revenue declined 20.7% year-over-year as the semiconductor equipment cycle normalized after the 2023-2024 surge. The Veeco merger introduces integration risk, and cyclical exposure means earnings could remain under pressure if chip capex moderates.

3. Samsara (IOT) | ~$14.7B Market Cap

Pioneer of the Connected Operations platform, providing IoT-based fleet management, safety monitoring, and operational analytics for physical-world businesses. Samsara is uniquely insulated from the AI software substitution fear because its value proposition centers on physical sensors, hardware connectivity, and real-time operational data—not knowledge-worker software workflows.

Why it matters: With analyst consensus targeting $48.67 (91% upside from current $25.42), Samsara represents one of the most compelling growth-at-a-discount opportunities created by the indiscriminate SaaS selloff. The majority of North American commercial vehicles still lack telematics and safety products, providing a massive under-penetrated market runway.

Key risks: Still unprofitable with a negative P/E ratio, and the broader SaaS sentiment contagion could continue dragging shares lower despite the company’s differentiated physical-operations focus. Revenue growth of 29% YoY is strong but must be sustained to justify the premium.

Strategic Recap & Forward Outlook

-

The “AI as Pilot” Narrative Has Arrived: Anthropic’s Claude Cowork platform has shifted the market narrative from “AI enhances software” to “AI replaces software.” This paradigm shift will continue driving violent rotations within tech—away from SaaS incumbents and toward AI infrastructure hardware providers, cloud hyperscalers, and companies with physical-world moats.

-

Hyperscaler AI Capex Is Accelerating, Not Decelerating: Despite market hand-wringing over “wasteful spending,” the combined 2026 AI capex guidance from Alphabet ($175–185B), Amazon ($200B), and Meta ($135B) confirms that AI infrastructure buildout is entering a new phase of scale. Semiconductor and networking equipment providers (NVDA, AMD, AVGO, MRVL) are the primary beneficiaries.

-

Dow 50,000 Signals Institutional Rotation Has Legs: The historic breach of the 50,000 level was driven by old-economy industrials, financials, and energy—not tech. This rotation reflects a genuine reallocation of capital toward tangible earnings, reasonable valuations, and cyclical recovery beneficiaries, and is likely to persist as long as tech valuations remain under pressure.

Forward Outlook (Week Ending February 14, 2026)

The coming week features an exceptionally dense earnings calendar, with AppLovin (Feb 11), Cisco, Shopify, and several financial and industrial names reporting. Markets will remain highly sensitive to any further AI disruption announcements, with Anthropic’s Claude Opus 4.6 release still reverberating through software valuations. Key economic data includes the January CPI report, which will be critical for Fed rate expectations—any upside surprise in inflation could compound the selling pressure on rate-sensitive growth stocks.

Near-term direction hinges on three variables: whether the Friday semiconductor rally can sustain momentum into next week, whether additional SaaS earnings reports reveal real AI substitution impact versus sentiment-driven fear, and whether the January CPI report gives the Fed room to maintain its dovish trajectory. Volatility remains elevated (VIX rising during the week), but the medium-term backdrop stays constructive for quality names with earnings visibility and AI infrastructure exposure.

Positioning favors semiconductor and AI hardware infrastructure (NVDA, AMD, AVGO) over software; cloud hyperscalers with accelerating revenue (GOOGL) over those with capex-compressed margins (AMZN); quality cyclicals and financials benefiting from the Dow rotation; and selective small-cap defense and physical-operations names insulated from the SaaS disruption narrative. Maintain elevated cash buffers to deploy on further AI-related dislocations, which are likely to continue creating asymmetric entry points in fundamentally strong companies.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.