Caterpillar Ran 32% While Everyone Stared at Oil

Everyone was chasing oil. We were long CAT.

Early 2026 consensus was clean. Iran escalation. WTI ripping from $55 to $114. Pure-play energy was the trade. ExxonMobil and Chevron owned the tape, and the financial press had one story to tell.

We took the other side. On January 15, Stock Research went long Caterpillar at $636.53 with a $730 target.

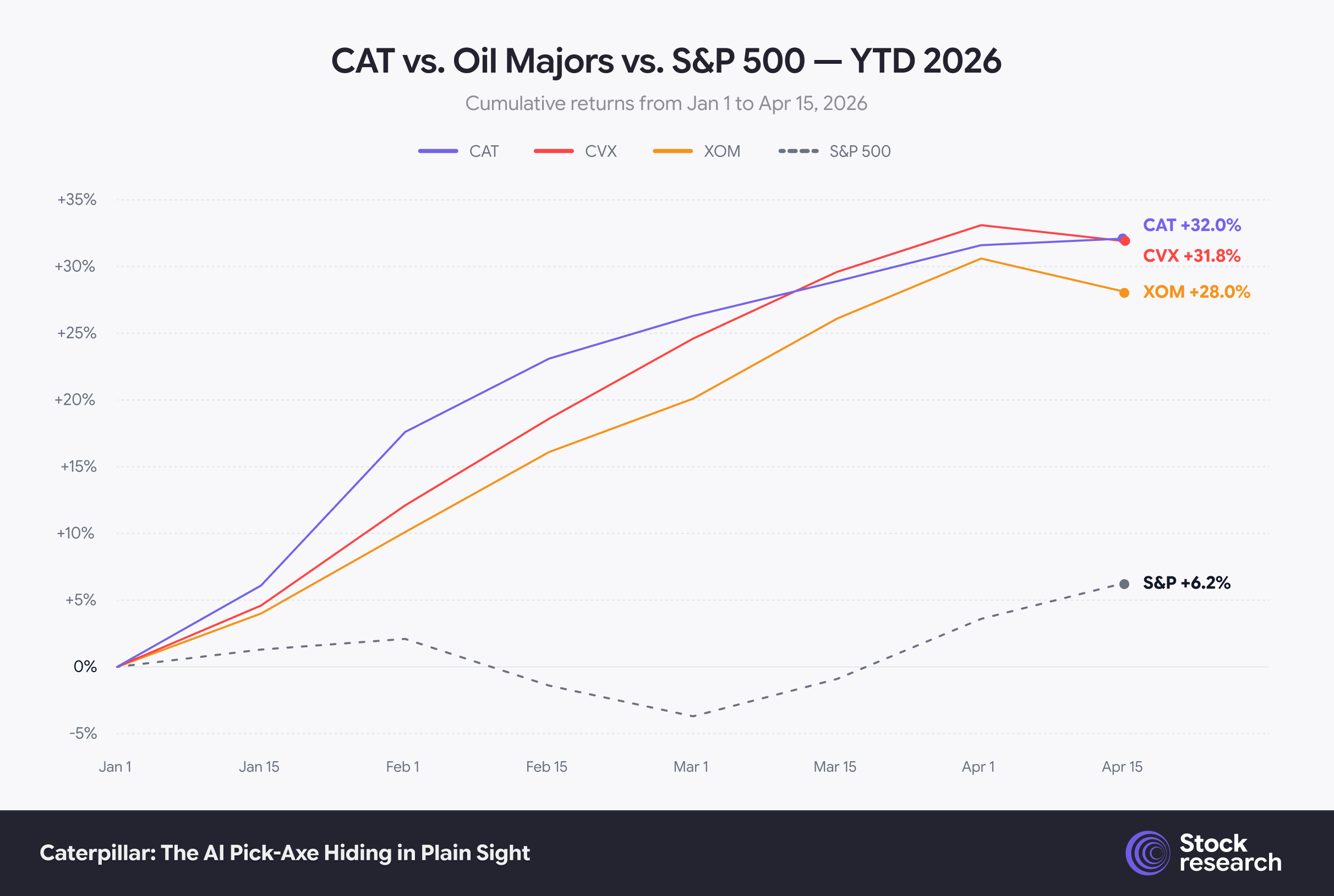

Ninety days later: target exceeded, all-time high of $797.85 printed on April 10, stock now trading around $770. Up 32% year-to-date. Roughly three times the S&P 500’s return over the same window.

But the scoreboard alone misses the story. Oil got there too. The real call wasn’t beating the energy trade on returns. It was picking the compounding story while the crowd piled into the cyclical one.

The Scorecard

Four numbers run the thesis:

-

Entry: $636.53 (Jan 15, 2026)

-

Target set: $730 (+15% called)

-

ATH: $797.85 (April 10) — target cleared by 9.3%

-

Today: ~$770 · +32% YTD

Forward P/E sits around 22x, up from the historical 12–15x industrial range. Roughly half the move is multiple expansion. The other half is earnings. Both are justified by what happened next.

Catalyst #1: The CES Reveal Nobody Saw Coming

Caterpillar took the CES 2026 keynote stage in early January. That alone was the tell. Heavy-equipment manufacturers don’t do consumer-electronics keynotes unless the story has shifted.

CEO Joseph Creed unveiled the Cat AI Nexus: a generative-AI layer embedded directly into the machine operating system. Alongside it, a $725 million capacity expansion at the Lafayette, Indiana engine facility, explicitly earmarked for AI data center power generation.

The signal was unmistakable. Caterpillar was no longer asking to be valued like John Deere or Cummins. It was asking to be valued like Rockwell Automation or Siemens. Industrial tech.

Within two weeks, analyst targets started migrating upward. Bernstein led. Others followed. That re-rate alone explains roughly half the YTD return.

Catalyst #2: The 2GW Order That Changed the Math

January 28. Caterpillar announced a strategic alliance with American Intelligence & Power Corp and Boyd CAT to deploy 2 gigawatts of fast-response natural-gas generator capacity at the Monarch Compute Campus in West Virginia. Deliveries begin September 2026. The campus is designed to scale toward 8 GW.

On the Q4 call, Creed called it “one of our largest single orders for complete power solutions.” The press covered the headline number. They missed the bigger point.

Monarch introduced a new category of customer relationship: prime power. Data centers bringing their own dedicated generation rather than waiting three years for a grid interconnect. These contracts carry multi-year parts, service, and monitoring attachment rates. Equipment sales become recurring revenue.

Cummins, Siemens Energy, and Rolls-Royce cannot scale turbine supply to meet current demand. That’s pricing power. That’s margin.

Catalyst #3: The $51 Billion Backlog

One day after Monarch, the Q4 2025 print landed. EPS beat consensus by 9.27% ($5.16 vs. $4.72 expected). Revenue beat by 6.12% ($19.13B vs. $18.03B). Backlog hit $51 billion.

The critical detail: Power & Energy, not Construction, not Resource Industries, became the fastest-growing segment. Management explicitly tied it to AI data center demand. The financial engineering had caught up with the narrative.

Renting vs. Owning the Rally

Here’s the part that matters most. Oil stocks rallied hard in Q1 too.

-

XOM: +28% YTD

-

CVX: +32% YTD

-

CAT: +32% YTD

On paper, everyone won. Read the underlying engine and the story inverts.

XOM and CVX are renting the rally. Their gains trace back to WTI doubling on Iran tensions — a cyclical, commodity-driven tailwind. When crude mean-reverts, multiples compress. The rally unwinds.

CAT is owning it. Its 32% is a structural re-rate anchored in multi-year AI power demand — a theme that compounds through 2030 rather than unwinding on a ceasefire headline. The order books are different. So is the margin profile. So is the duration.

Same return. Completely different quality.

The Next Leg

Four catalysts sit in front of the stock right now.

-

Q1 2026 earnings — April 30. First print after CES and Monarch. Any material P&E beat drives further multiple expansion.

-

Lynn Good added as board nominee — April 13. Former Duke Energy CEO. The board is building power-generation governance expertise for a reason.

-

CFO transition — May 1. Andrew Bonfield moves to advisor, Kyle Epley steps in. Planned succession, but execution continuity matters at an inflection like this.

-

Monarch deliveries — September 2026. Backlog begins converting to recognized revenue. First real proof point on prime-power margins.

Management’s published targets: $30 billion in services revenue by 2030 (from $24B in 2025) and turbine capacity roughly doubled over the same horizon. Both translate into high-margin, recurring revenue. Neither is fully baked into current consensus.

The Risks Are Real

At $770, the easy money is gone. Three things to respect.

-

Street target is $739 — below spot. The 34-analyst consensus says the stock has front-run the fundamentals. A 4% mean-reversion is the bearish read.

-

$2.6 billion tariff headwind. CAT’s global supply chain makes it exposed to any new round of US-China escalation.

-

Cyclical exposure. Construction still carries a meaningful slug of revenue. A hard landing in US housing or a deeper China slowdown hits the segment directly.

None of these invalidate the thesis. All of them can delay it.

The Bottom Line

We went long CAT as a non-consensus AI infrastructure play while the market chased oil. Ninety days later, the thesis paid — target cleared, ATH printed, 32% YTD. The interesting question isn’t whether the January call was right. It’s whether the structural re-rate still has room to run after the easy multiple expansion is done. We think the answer sits in the P&E segment. The market still isn’t pricing it at full value.

This article is a preview of our full Stock Research Intelligence Report on Caterpillar.

Read the complete deep-dive — including the benchmarked scorecard vs DE and CMI, the detailed Q4 earnings-beat visualization, the full catalyst calendar through year-end, the services + turbine capacity trajectory to 2030, the structural-vs-cyclical 2-panel, and our split Actionable Insights for new positions vs existing holders — on

Stock Research delivers institutional-grade US equity research for investors who want signal, not noise.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Stock Research analysts may hold positions in securities discussed. Equity investments carry market risk, including possible loss of principal. Always conduct your own due diligence before making any investment decisions.