NVIDIA: Is It Too Late to Buy the AI Supercycle?

NVIDIA just crossed a $4.5T market cap and became the most valuable company on earth. After a 10x run since early 2023, most investors are asking one thing: is there still upside, or is this the top?

This Substack edition is the lite version: the story, the key charts, and the core investment thesis.

For the full institutional-grade report, including our valuation model, scenario analysis, detailed risk assessment, and portfolio sizing framework, we provide complimentary access via a downloadable link.

TL;DR: Why We Still Rate NVIDIA a BUY

-

AI infra is still early: AI accelerator spend could grow from ~$118B in 2024 to $305–$650B by 2030. NVIDIA is currently taking the lion’s share.

-

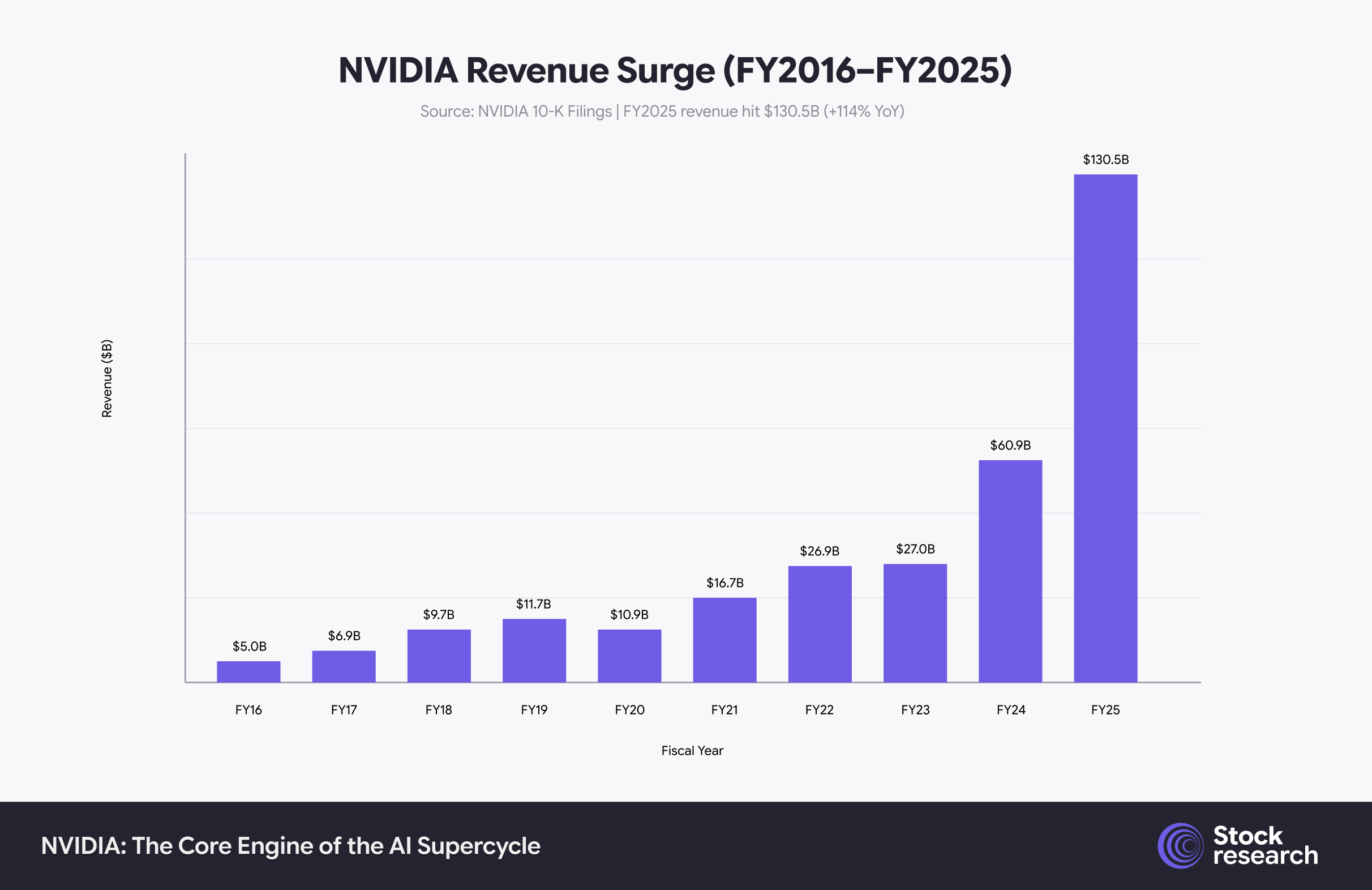

Insane revenue ramp: NVIDIA’s revenue went from $27B (FY2023) to $61B (FY2024) to $130.5B in FY2025, and is tracking to about $213B in FY2026.

-

Monopoly-like position in AI chips: NVIDIA controls 80%+ of the AI accelerator market and ~90% of data center GPU deployments.

-

Margins of a software company: FY2025 gross margin hit 75%, with net margin at ~56% and free cash flow of ~$61B.

-

Valuation looks expensive… until you look at 2027–2028: At ~51x forward earnings it looks pricey, but on FY2027–2028 estimates it trades closer to 24–30x with EPS still compounding >40%.

The AI Engine Behind NVIDIA’s 10x Run

NVIDIA is no longer “just a GPU company.” It’s the default operating system for AI compute.

1. From gaming to AI supercomputer vendor

In less than three fiscal years, NVIDIA turned itself from a cyclical gaming/crypto name into an AI infrastructure vendor with Data Center at 88% of revenue.

Data Center revenue alone reached about $115B in FY2025, up ~142% year‑on‑year, while gaming, pro‑viz, and auto now look like satellites around the AI core.

2. The most profitable “hardware” company in history?

Revenue isn’t the only thing going vertical.

-

Revenue went from $5B in FY2016 to $130.5B in FY2025.

-

Gross margin recovered from a FY2023 dip (crypto/gaming bust) back up to ~75%, with operating margin over 60% and net margin ~56%.

Effectively, NVIDIA now looks like a high‑growth software platform on semiconductor scale.

Why NVIDIA’s Moat Is Hard to Break

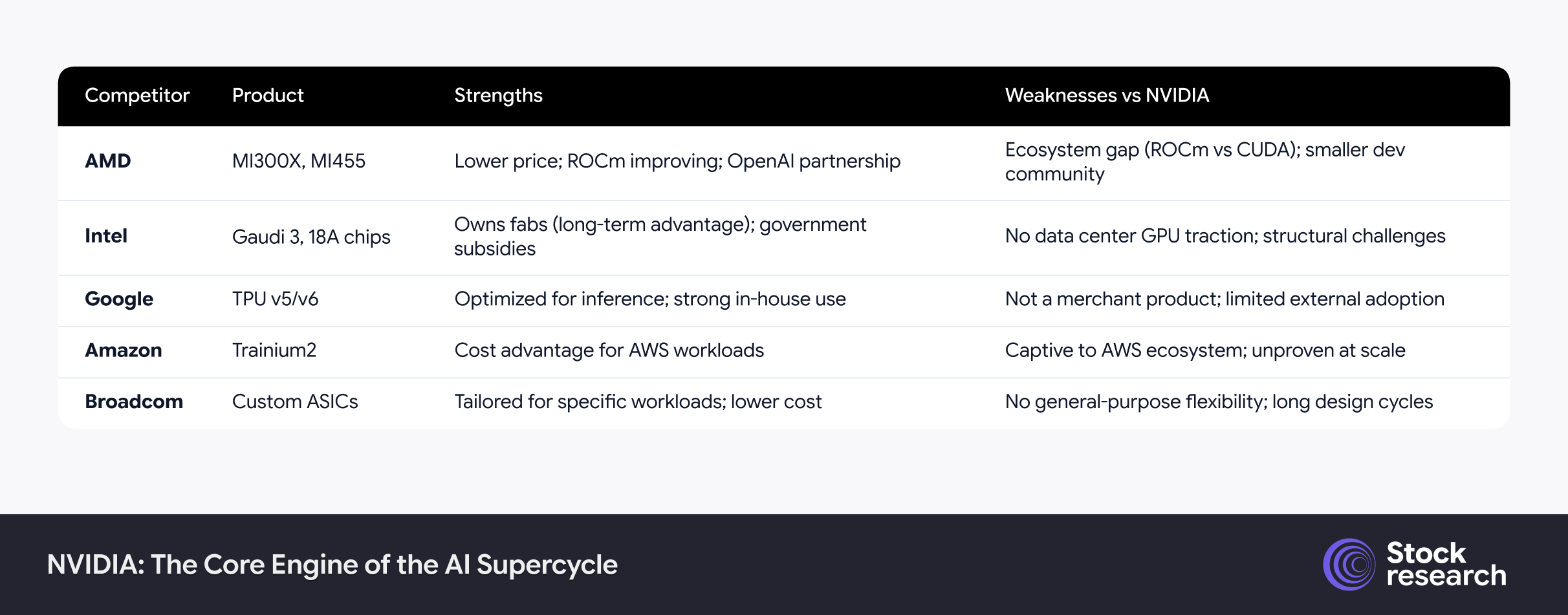

Competitors aren’t asleep. AMD is pushing MI300/MI455, Intel is betting on Gaudi and its 18A process, and hyperscalers are building TPUs, Trainium, and Maia. So why hasn’t that destroyed NVIDIA’s economics?

At a high level, the moat is full‑stack lock‑in:

-

Hardware: Leading edge AI GPUs (Hopper → Blackwell → Rubin → Vera) with superior tensor performance and memory bandwidth.

-

Software (CUDA): 2M+ developers, optimized libraries (cuDNN, TensorRT, NCCL), and tight integration with PyTorch, TensorFlow and major AI frameworks.

-

Platform: DGX systems, DGX Cloud, NVIDIA AI Enterprise, Omniverse, DRIVE — turning chips into a full AI operating system.

-

Network effects: Every quarter more models, tools and research target NVIDIA first; the ecosystem lead compounds.

For a hyperscaler, switching away from NVIDIA isn’t just swapping a chip. It’s re‑tooling the entire software and tooling stack. That’s why, even with credible alternatives, NVIDIA still holds >80% AI accelerator share.

The Numbers: What the Market Is Paying For

Despite the rally, NVDA’s move from “insane bubble” to “expensive but rational” is happening faster than most realize.

Revenue & Earnings Ramp

-

Quarterly revenue stepped from $26B (Q1 FY2025) to $39B (Q4 FY2025) to $57B (Q3 FY2026), with Q4 FY2026 guided to $65B.

-

FY2026 revenue is on track for ~$213B, up from $130.5B last year.

-

Consensus EPS: $4.4 (FY2026E) → $6.4 (FY2027E) → $7.8 (FY2028E).

Valuation Snapshot

At around $190/share, NVIDIA trades at:

-

~51x FY2026E earnings

-

~30x FY2027E

-

~24x FY2028E

-

~25x sales on trailing revenue

Versus peers:

You’re paying a premium, but you’re also buying the company that structurally owns the fastest‑growing part of the data center stack.

The AI TAM: How Much Room Is Left?

The core question for long‑term investors: how big can AI accelerators and NVIDIA’s slice of it actually get?

Different sources peg AI accelerator TAM in 2030 anywhere between ~$305B (conservative) and ~$650B (bullish), with some work suggesting a path to $1T+ if agentic/“reasoning” AI and physical AI really hit escape velocity. Jensen Huang himself talks about a $5T AI TAM when you include the full stack (chips, systems, software, services).

If NVIDIA holds 60–70% share (down from ~80%+ today) on a $300–600B market, you’re still looking at a company doing $200B+ of high‑margin AI revenue annually.

What Could Break the Story?

This isn’t risk‑free. The full stockresearch.ai report goes into a dedicated Risks & Bear Case section, but here are the big ones to watch:

-

China risk: Export controls have been a moving target. The Trump administration recently shifted to case‑by‑case approvals and introduced a 25% tariff, while China has reportedly asked local firms to halt orders of H200 chips.

-

Hyperscaler behavior: If Microsoft, Meta, Google or Amazon materially slow AI CapEx or migrate large chunks of workload to AMD/custom silicon, NVIDIA’s growth could decelerate quickly.

-

Margin compression: From 75% gross margin today, more competition and more aggressive pricing could drag that down into the high‑60s over time.

-

Key‑person risk: Jensen Huang is both CEO and the strategic brain of NVIDIA. Any negative surprise here would hit sentiment fast.

In our base case, these risks bend the curve, but don’t break it. The bear case in the full report lays out what numbers would justify a downgrade to HOLD/SELL.

So… Is It Too Late to Buy?

In the full stockresearch.ai report, we rate NVIDIA BUY, with:

-

Base‑case 12‑month target of $260 (~35–40% upside)

-

Bull case north of $300 if AI spending and margins remain at current trajectories

-

Bear case in the $140–150 zone if AI CapEx rolls over and margins compress

The core idea: this is no longer about “multiple expansion”. Future returns will be driven by actual earnings power catching up with the hype — and so far, NVIDIA is delivering numbers that justify a big chunk of the valuation.

For a long‑term, fundamentally‑driven investor, that’s exactly the setup you want: a structurally advantaged compounder where the multiple compresses as earnings explode.

Want the Full, Institutional‑Grade NVIDIA Report?

This Substack is the lite version. Inside the full research report, you’ll get:

-

Full 14‑section NVIDIA report

-

Detailed DCF and relative valuation model

-

Scenario analysis (bull / base / bear) with explicit revenue & EPS paths

-

Moat deep‑dive on CUDA, ecosystem, and hyperscaler behavior

-

Risk matrix with “what would change our rating” triggers

-

Portfolio sizing guidance for long‑term investors

If you want the same style of research you see on the sell side — but built for long‑term, independent investors — you can access the full NVIDIA report and future coverage directly here:

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.