StockResearch Intelligence Weekly #1

Welcome to the first-ever edition of StockResearch Intelligence Weekly, where we cover the most important developments in the U.S. stock market, high-conviction investment ideas, and data-driven insights for long-term investors.

Market Insight

The second full week of January 2026 marks a psychological inflection point for U.S. equities, with record highs colliding with growing sustainability concerns. The S&P 500 reached a new all-time high at 6,966, the Dow Jones surpassed 49,500 for the first time, and the Russell 2000 delivered its strongest start since 2021. Beneath the surface, however, market leadership is fragmenting and institutional conviction remains selective.

This is a measured, not euphoric, rally driven by optimism around Fed rate cuts, strong Q4 earnings, and resilient consumer demand, while key risks persist. The VIX fell to 14.6, signaling complacency even as inflation, valuation fragility in AI and mega-cap tech, and Fed leadership uncertainty linger. With markets priced for dovish outcomes, the January 27–28 Fed meeting presents a binary risk: any hawkish surprise could quickly unwind recent gains.

Strengths

-

Broad Market Breakout & Momentum: All major U.S. indices hit new all-time highs, with small caps leading. The Russell 2000’s strong start signals genuine market broadening beyond mega-cap dominance.

-

Earnings Strength Confirms Resilience: Major U.S. banks beat Q4 expectations, validating consumer and credit strength. Earnings growth outlook for 2025–2026 remains supportive of current valuations.

-

Small-Cap Rotation Underway: Institutional flows are rotating into undervalued small caps, which trade at meaningful discounts and offer asymmetric upside as Fed easing expectations build.

Weaknesses

-

Mega-Cap Valuation Risk: AI and large-cap tech valuations are stretched, creating asymmetric downside if earnings or AI ROI disappoint. Low volatility suggests complacency.

-

Fed Policy Disconnect: Markets are pricing aggressive rate cuts, while Fed guidance implies a higher-for-longer path. The January FOMC meeting presents binary repricing risk.

-

Labor Market Softening: Job openings and hiring are slowing beneath the surface, threatening consumer spending and earnings if deterioration accelerates.

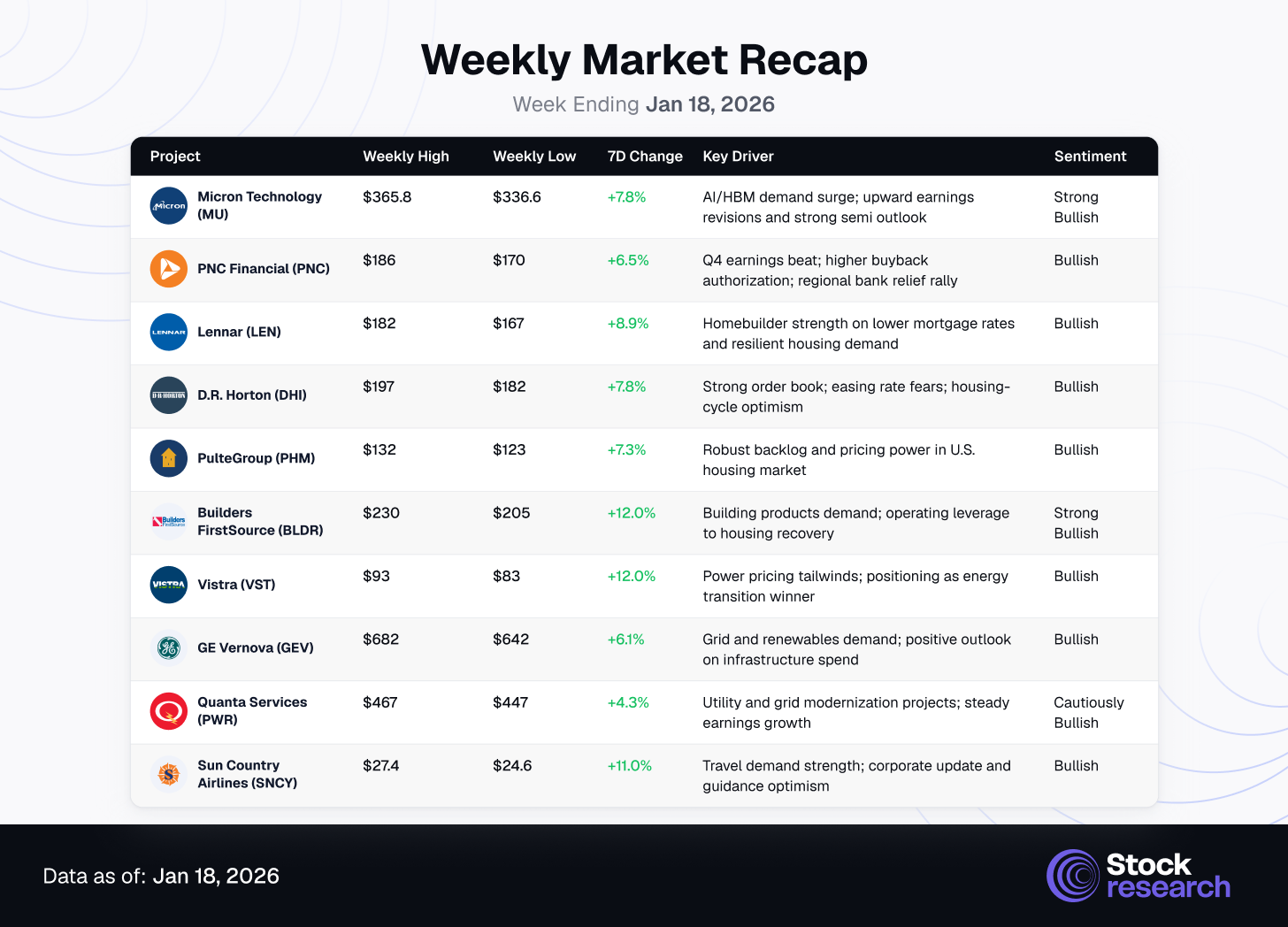

Market Recap

Market Context: The week ending January 18, 2026, represents a transition from mega-cap dominance to genuine market broadening. Small-cap leadership, bank earnings strength, and improved market breadth signal institutional conviction. However, this rally remains conditional on Fed accommodation and sustained earnings growth—two variables that face material uncertainty ahead of the January 27–28 FOMC meeting.

Top 3 Stock Picks for Long-Term Investment

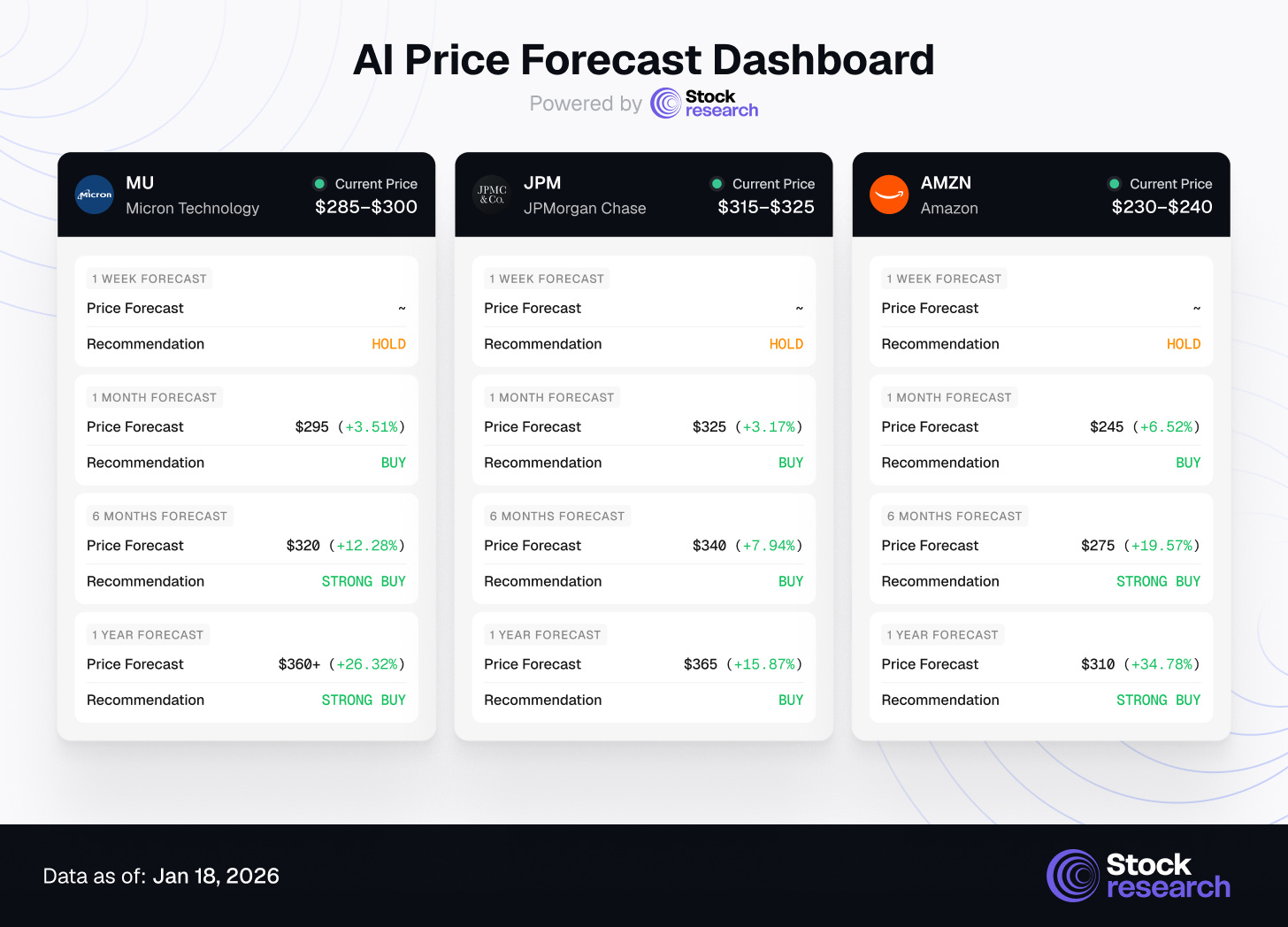

1. Micron Technology (MU)

Investment Horizon Recommendation:

-

1 Week: HOLD (near-term consolidation likely)

-

1 Month: BUY (earnings catalyst imminent)

-

6 Months: STRONG BUY (AI/HBM demand accelerating)

-

1 Year: STRONG BUY (structural semiconductor upcycle)

Thesis: Micron has emerged as the definitive winner in the AI infrastructure buildout, driven by surging demand for High-Bandwidth Memory (HBM) solutions critical for training and deploying large language models and AI workloads. The company posted record data center sales in Q1 FY2026 and is forecasting revenue growth of 89.3% and earnings growth exceeding 100% for the fiscal year ending August 2026. This is not speculative growth; it is structural demand driven by capital expenditure commitments from hyperscalers (Microsoft, Amazon, Google, Meta) deploying next-generation AI infrastructure.

Catalysts:

-

AI Memory Bottleneck: HBM is the critical constraint in AI chip performance, and Micron’s leadership in HBM3E positions it as the sole supplier capable of meeting hyperscaler demand at scale.

-

Earnings Momentum: Zacks Consensus Estimate for FY2026 earnings has risen 64.2% over the past month, reflecting upward estimate revisions—a leading indicator of outperformance.

-

Margin Expansion: Micron’s transition from commodity DRAM to high-margin HBM products is driving operating leverage and profitability inflection.

Risks: Cyclical semiconductor inventory corrections; geopolitical tensions (Taiwan/China); potential AI capex slowdown if return on investment disappoints.

Price Targets:

-

1-Month: $295

-

6-Month: $320

-

1-Year: $360+

Micron represents a pure-play on the AI infrastructure thesis with genuine revenue and earnings visibility, trading at a reasonable valuation relative to its growth trajectory. This is a structural winner, not a speculative trade.

2. JPMorgan Chase (JPM)

Investment Horizon Recommendation:

-

1 Week: HOLD

-

1 Month: BUY

-

6 Months: BUY

-

1 Year: BUY

Thesis: JPMorgan represents the highest-quality exposure to the U.S. financial system, combining deposit franchise dominance, investment banking leadership, and trading desk resilience. The bank’s Q4 2025 earnings decisively beat expectations, with record revenues driven by net interest margin expansion and strong capital markets activity. CEO Jamie Dimon’s commentary emphasized the bank’s fortress balance sheet, diversified revenue streams, and ability to navigate higher-for-longer rates—a macro environment that benefits large-cap banks over regional competitors.

Catalysts:

-

Net Interest Margin Expansion: Higher-for-longer rates benefit JPM’s deposit-rich balance sheet, driving structural margin expansion.

-

Investment Banking Revival: M&A activity and capital markets issuance are accelerating after two years of weakness, directly benefiting JPM’s fee-based businesses.

-

Shareholder Returns: JPM has signaled continued buybacks and dividend growth, supported by robust capital generation.

Risks: Recession-driven loan loss provisions; regulatory capital requirements; potential commercial real estate stress.

Price Targets:

-

1-Month: $325

-

6-Month: $340

-

1-Year: $365

JPM is a defensive quality play with offensive growth characteristics. It offers exposure to economic resilience, financial sector rotation, and a management team with a proven track record of capital allocation. This is a core holding for any long-term portfolio.

3. Amazon (AMZN)

Investment Horizon Recommendation:

-

1 Week: HOLD

-

1 Month: BUY

-

6 Months: STRONG BUY

-

1 Year: STRONG BUY

Thesis: Amazon is trading at a temporary valuation disconnect, offering a compelling entry point into the dominant e-commerce and cloud infrastructure franchises. RBC Capital analyst Brad Erickson labeled Amazon as a top 2026 pick, citing “best-in-class visibility on infrastructure ROI with a compelling product cycle/capacity acceleration cycle approaching.” Amazon Web Services (AWS), which generates the majority of Amazon’s operating profit, is positioned to benefit disproportionately from the AI infrastructure buildout as enterprises migrate workloads to generative AI-optimized cloud environments.

Catalysts:

-

AWS AI Revenue Acceleration: AWS is capturing enterprise AI spending through services like Bedrock (generative AI platform) and SageMaker (machine learning infrastructure).

-

E-Commerce Margin Expansion: Amazon’s retail segment is achieving structural margin improvement through automation, logistics optimization, and advertising revenue growth.

-

Advertising Business Maturation: Amazon’s advertising segment is now a $50+ billion annual run-rate business with higher margins than retail, driving incremental profitability.

Risks: Regulatory scrutiny (antitrust, FTC); AWS competitive pressure from Microsoft Azure and Google Cloud; consumer spending slowdown.

Price Targets:

-

1-Month: $245

-

6-Month: $275

-

1-Year: $310 (RBC target: $300)

Amazon offers dual exposure to secular growth themes—cloud computing and AI infrastructure—while trading at a valuation that reflects near-term pessimism rather than long-term structural dominance. This is a buy-the-dip opportunity in a generational compounder.

Low-Cap Stock Opportunities: Undiscovered Value

As mega-cap stocks reach valuation extremes, institutional capital is rotating into small-cap equities, creating asymmetric opportunities in companies with market caps below $2B. These stocks benefit from discounted valuations, accelerating earnings growth, and limited analyst coverage, resulting in exploitable inefficiencies for disciplined investors.

The Small-Cap Setup

Small-caps are off to their strongest start since 2021, with the Russell 2000 up 7.8% YTD versus 1.5% for the S&P 500. This move reflects valuation-driven rotation rather than speculation, as small-value stocks trade at a ~23% discount to fair value. With the Fed transitioning toward easing, mean reversion remains a powerful tailwind. Quality small-caps with strong balance sheets and exposure to secular themes such as energy infrastructure, financial services, and renewables are leading the rotation.

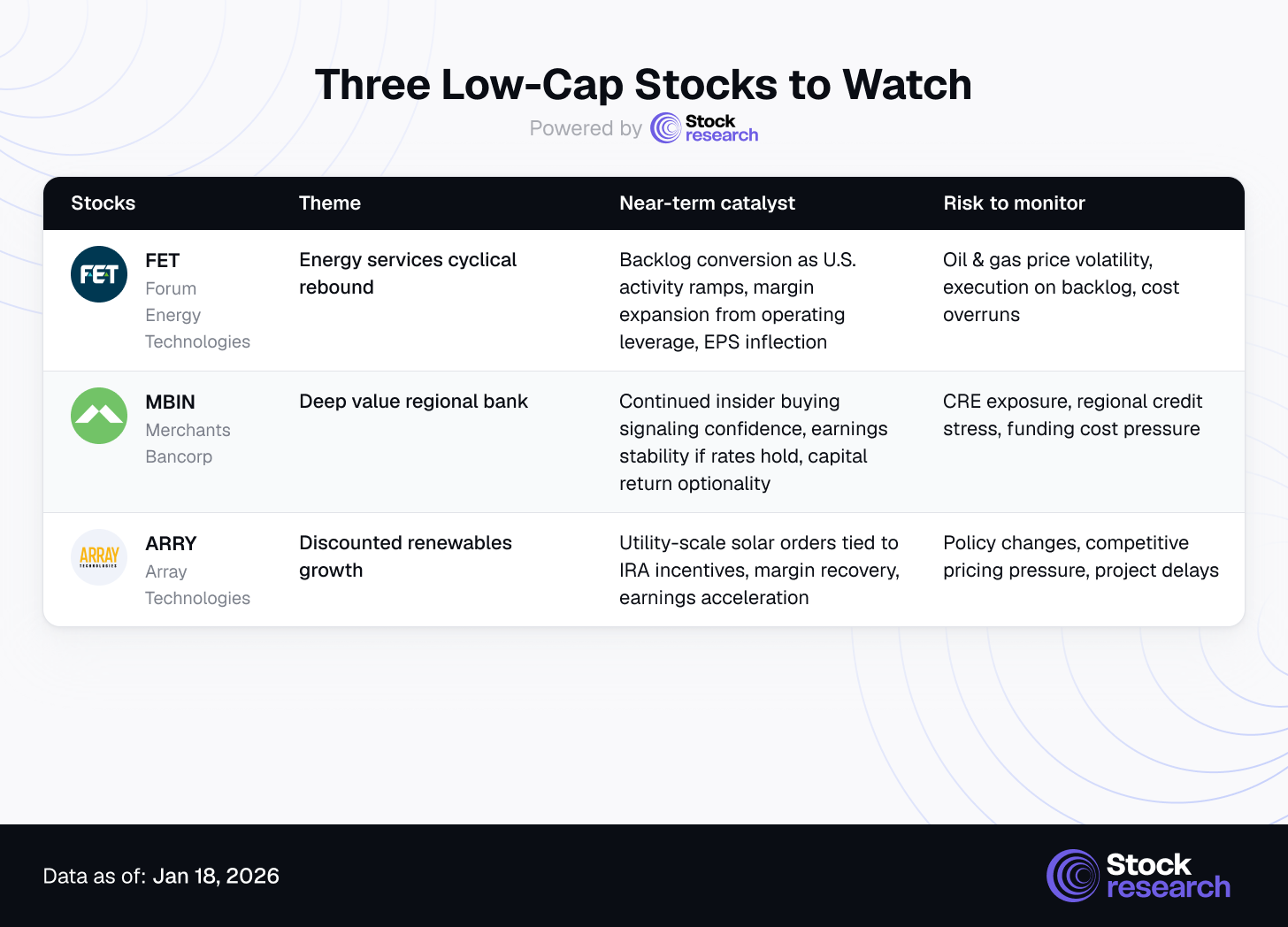

Three Low-Cap Stocks to Watch

1. Forum Energy Technologies (FET) | ~$500M

Energy services provider with a $1.9B backlog dominated by domestic projects. EPS is projected to grow nearly 200% this year, reflecting operating leverage to energy recovery.

Why it matters: Cyclical upside with improving cash flow visibility.

Key risks: Energy price volatility and execution risk.

2. Merchants Bancorp (MBIN) | ~$1.2B

Regional bank trading at 8.2x forward earnings with heavy insider buying and conservative underwriting. Positioned to benefit from stable rates and resilient regional lending.

Why it matters: Deep value with insider conviction.

Key risks: CRE exposure and regional credit stress.

3. Array Technologies (ARRY) | ~$1.8B

Solar tracking systems leader benefiting from IRA incentives and utility-scale solar expansion. Projects ~45% earnings growth while trading below 10x forward earnings.

Why it matters: Structural renewables growth at discounted valuation.

Key risks: Policy shifts and competitive pressure.

Why Low-Caps Matter in 2026

The small-cap rotation is structural, not tactical. With small-cap earnings expected to outpace large-caps in 2026, capital is reallocating from crowded mega-cap trades into under-owned growth at reasonable prices. For investors willing to accept higher volatility, low-cap stocks offer a compelling source of next-cycle alpha.

Strategic Recap & Forward Outlook

The week ending January 18, 2026 highlights a market at a crossroads. U.S. equities reached record highs supported by genuine market broadening, yet face rising binary risks from Fed policy, valuation stretch in mega-cap tech, and early signs of economic deceleration. Rotation into small caps, financials, and cyclicals is constructive, but sustainability hinges on dovish Fed guidance at the January 27–28 meeting and continued earnings delivery.

Key Takeaways

-

Small-Cap Rotation Is Structural: The Russell 2000’s outperformance reflects institutional recognition of valuation dislocations, not speculative excess. Quality small caps offer asymmetric upside if easing expectations hold.

-

Bank Earnings Confirm Resilience: Strong Q4 results from major U.S. banks validate consumer and credit strength, supporting financial sector leadership and reducing near-term recession risk.

-

Mega-Cap Execution Risk Rising: AI and mega-cap tech valuations leave little margin for error. Any earnings or AI ROI disappointment could trigger sharp pullbacks.

-

Fed Is the Primary Catalyst: Markets remain positioned for dovish outcomes. A higher-for-longer signal would force rapid repricing across risk assets.

-

Conviction Plays for 2026: Micron, JPMorgan, and Amazon offer exposure to durable growth themes at valuations that balance caution with long-term opportunity.

Forward Outlook (Week Ending January 25, 2026)

Expect near-term consolidation as markets position ahead of the January FOMC meeting. Softer inflation data would extend the rally, with small caps continuing to lead. A hawkish surprise would likely pressure mega-cap tech and accelerate rotation into defensive value.

Risk Context: Headline trends remain constructive, but underlying fragility persists. Elevated valuations, mega-cap concentration, and subdued volatility create asymmetric downside risk. Positioning should remain selective, with disciplined sizing, quality bias, and cash reserves for volatility-driven opportunities.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Equity markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.