StockResearch Intelligence Weekly #11

The week ending March 29, 2026 delivered the fifth consecutive weekly loss for U.S. equities, a grinding, risk-off tape that now carries the S&P 500 to a -7.0% year-to-date print, the Nasdaq into correction territory (-9.9% YTD), and the Dow Jones down more than 10% from its February highs. Unlike the sharp, news-driven breaks earlier in March, this week’s decline had a different texture: it started with hope, briefly rallied on ceasefire headlines, and then reversed as reality returned.

Monday’s session saw a broad relief rally after the U.S. reportedly sent a 15-point ceasefire proposal to Iran. The S&P 500 gained as much as +1.3% on the optimism, with oil pulling back nearly -10% intraday. By Wednesday, the three major indices were briefly green as traders positioned for a peace trade, with the Dow gaining 305 points. But Iran’s military spokesperson dismissed the notion of direct talks, oil snapped back, and by Friday the major indices had logged their worst week in months.

The single most dominant variable in the market right now is oil. Brent closed the week near $100/barrel, a level that has become both ceiling and floor, after briefly surging above $108 earlier in the week. The ongoing closure of the Strait of Hormuz, which channels roughly 17.8 million barrels per day of global oil flow, is creating a structural energy shock that markets must now price as a persistent baseline, not a transient spike. President Trump again extended the deadline for Iran to reopen the route, moving it to April 6.

The CBOE Volatility Index (VIX) held above 31 for much of March, its highest sustained level since early 2022, while the CNN Fear & Greed Index plummeted to a reading of 15, firmly in “Extreme Fear” territory. These are not panic readings, but they represent structural anxiety: an inflation-fed, geopolitically-driven risk premium that the Federal Reserve cannot simply cut away.

Strengths

-

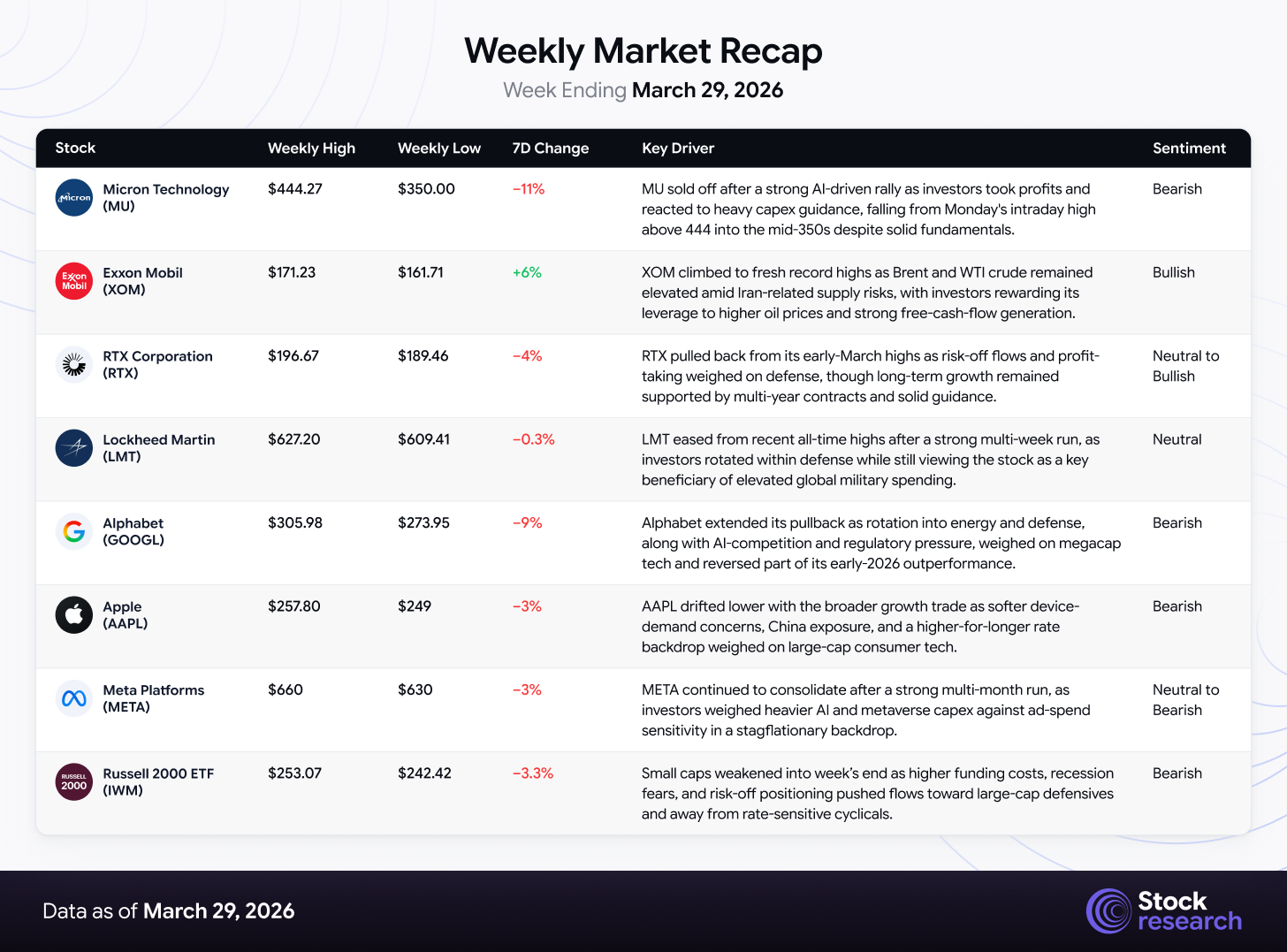

Energy and defense still providing a floor: ExxonMobil hit a new all-time high of $170.99 and Chevron reached a record $211.15 on March 27, cementing the energy sector’s status as the standout performer of 2026. Defense contractors (LMT, RTX, NOC) maintained relative resilience as geopolitical budgets globally expand. Year-to-date, the energy sector is up more than 22% even as the broader S&P 500 languishes in negative territory.

-

Quality and cash-flow leadership: The Russell 2000 eked out a +0.05% gain for the week, outperforming all three major large-cap indices, driven by institutional rotation into small-cap value names, which Morningstar rates as the most undervalued segment of the U.S. market, trading 23% below fair value estimates. High-quality large caps in staples, healthcare, and select industrials continued to outperform high-beta growth as investors prioritized balance-sheet durability over optionality.

-

Q1 earnings season beating expectations: With roughly 60% of S&P 500 companies having reported, FactSet forecasts an aggregate Q1 2026 EPS growth rate of approximately 12.5%, which would mark the sixth consecutive quarter of double-digit earnings growth for the index. The Industrials sector posted the largest positive EPS surprise aggregate for the period.

-

AI infrastructure winners breaking away from generic tech: Within technology, names tied directly to AI infrastructure, memory, semis, and data-center power, continued to show relative strength versus broad software. Wednesday’s brief ceasefire rally (+1.3% single-day S&P 500 gain) also confirmed substantial pent-up buying power, suggesting investors are refining AI exposure rather than abandoning the theme outright.

Weaknesses

-

Nasdaq and Dow in official correction territory: The Nasdaq closed the week 9.9% below its year-to-date opening value and more than 13% below its recent all-time high. The Dow crossed the -10% correction threshold, and the S&P 500 at -8.7% from its January peak is pressing the correction line heading into the final trading day of Q1.

-

Magnificent Seven hemorrhaging alpha: Nvidia’s shares fell on heavy retail selling even as they briefly recovered, with retail investors actively trimming exposure to the top AI winner. Micron Technology (MU) dropped 10% over the week following its blowout earnings print, markets are penalizing large capex commitments even when the fundamentals are strong.

-

Stagflation overhang becoming entrenched: Import prices surged 1.3% in February, the largest monthly increase in nearly four years, while export prices rose 1.5%. The Federal Reserve, which held rates at 3.50%–3.75% at its March 19 meeting, now projects core PCE to finish 2026 at 2.7%, above its December forecast. With energy costs elevated and wage-price dynamics sticky, the Fed has essentially no room to cut until geopolitical resolution is in sight.

-

Retail investor conviction collapsed: According to Vanda analysts, retail investors sold $5.5 million in U.S.-listed stocks in the first two hours of Wednesday’s trading, a session where the broader market was up, signaling that everyday investors are now in full capital-preservation mode.

Market Recap

Top 3 Stock Picks for Long-Term Investment

Powered by StockResearch AI

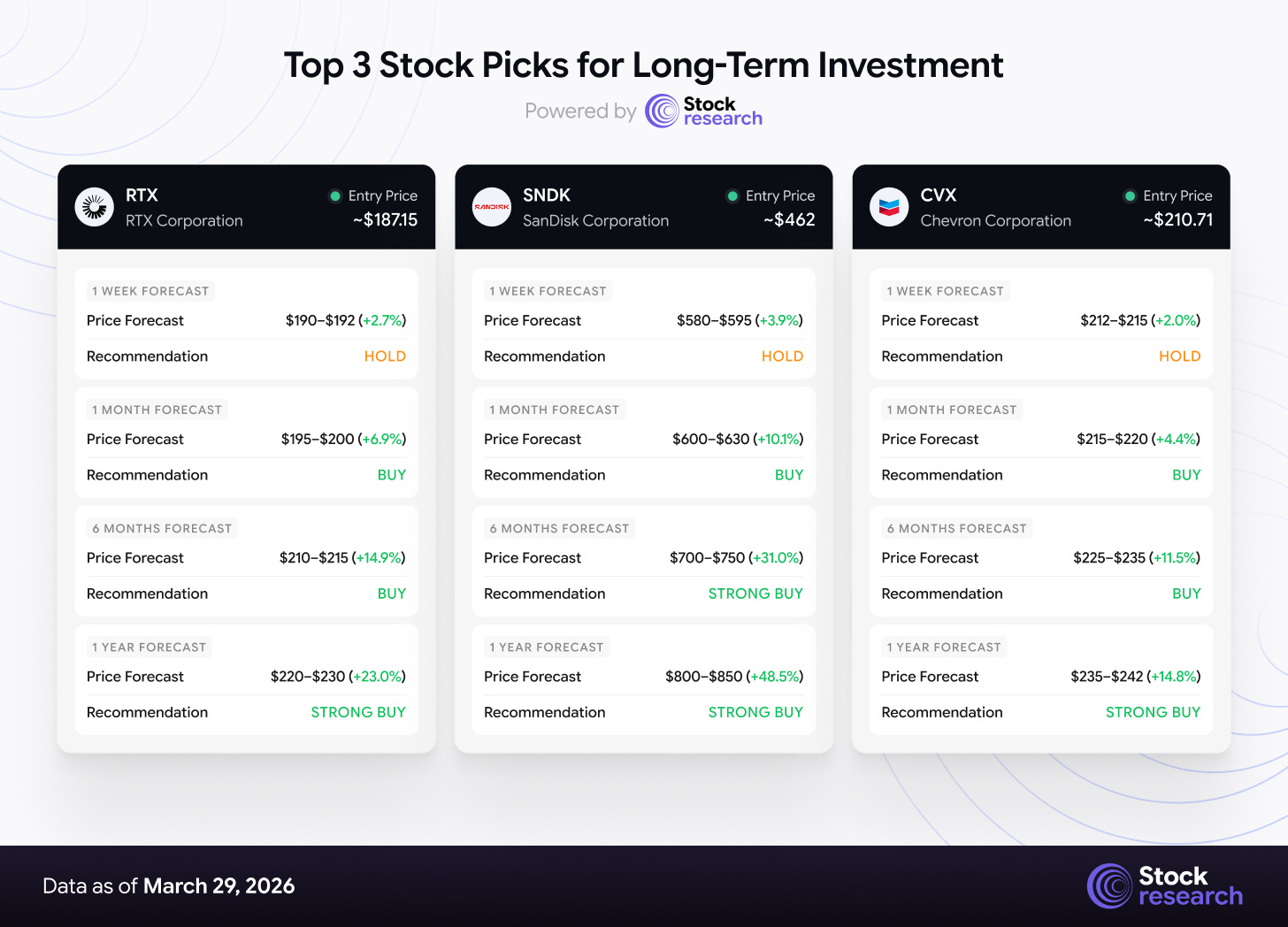

#1 RTX Corporation (NYSE: RTX)

Current Price: ~$187.15 | Sector: Aerospace & Defense | Rating: BUY

Thesis: RTX Corporation (formerly Raytheon Technologies) is the clearest structural beneficiary of the geopolitical environment now defining 2026. The company operates three divisions, Collins Aerospace, Pratt & Whitney, and Raytheon, giving it exposure to both military systems (missile defense, precision munitions) and commercial aerospace aftermarket services. The Iran conflict has driven a global reassessment of defense investment, and RTX sits squarely in the path of elevated government procurement. Citigroup has a Strong Buy rating with a $238 price target, while JP Morgan rates it Buy with a $215 target.

Fundamentals: Revenue is forecast at $94.29B for fiscal 2026, growing +6.41% YoY, expanding to $100.56B in 2027 (+6.65%). EPS growth is projected at 39.1% this year and 10.1% next year. The company carries a consensus Buy rating from 12 active analysts, with zero Sell ratings.

#2 SanDisk Corporation (NASDAQ: SNDK)

Current Price: ~$572.50 | Sector: Semiconductor / Storage | Rating: BUY ON PULLBACK

Thesis: SanDisk is the top-performing S&P 500 constituent of 2026, up more than 159% year-to-date, driven by a global NAND flash shortage and explosive AI-related demand for high-bandwidth storage. The company completed its spin-off from Western Digital in early 2025 and has since emerged as a pure-play on the data storage supercycle that AI is creating. The recent 10% pullback during the week (shares fell from ~$615 to ~$572) as investors digested capital expenditure guidance creates an attractive re-entry for long-term investors. B of A Securities carries a Strong Buy with a $900 target; Citigroup echoes that at $875.

Fundamentals: Revenue is forecast to surge 111.67% this fiscal year to $15.57B, then another 71.04% to $26.63B next year. EPS is expected to reach $40.83 this year (from -$11.32 last year), then nearly triple to $90.46 the following year. This is a semiconductor name with explosive earnings velocity, rare in any market environment.

#3 Chevron Corporation (NYSE: CVX)

Current Price: ~$210.71 | Sector: Integrated Energy | Rating: BUY

Thesis: Chevron hit a new all-time high on March 27 at $211.15, cementing its status as the top performer in the Dow Jones Industrial Average for the week. As an integrated oil major with global upstream production, downstream refining, and a growing chemical division, Chevron is uniquely positioned to capture the full value chain of an elevated oil price environment. With Brent above $100/barrel and the Iran conflict showing no near-term resolution, CVX is generating exceptional free cash flow that supports its dividend and ongoing buyback program. Morgan Stanley recently raised its CVX price target to $212, while Piper Sandler holds the street-high at $242.

Fundamentals: Revenue is forecast at $193.05B for fiscal 2026 (+4.55% YoY), scaling to $200.13B in 2027 (+3.67%). EPS growth of +1.40% this year accelerates to +36.68% in fiscal 2027 as the full benefit of sustained high oil prices flows through. The Buy consensus from 19 analysts, anchored by Piper Sandler’s Overweight and Mizuho’s Outperform, reflects deep conviction in the energy supercycle.

Low-Cap Stock Opportunities: Undiscovered Value

They represent higher-risk, higher-reward opportunities suited for patient, research-driven investors.

Opportunity #1, BWX Technologies (NYSE: BWXT)

Current Price: ~$191.59 | Market Cap: ~$17.5B | Sector: Nuclear Defense & Industrial

Overview: BWX Technologies is the sole manufacturer of naval nuclear reactors and fuel for the U.S. Naval Nuclear Propulsion Program, making it one of the most mission-critical and irreplaceable contractors in the defense industrial base. The company holds a $7.3 billion backlog supported by sole-source contracts and decades of specialized expertise that create near-impenetrable competitive moats. In its latest quarter, BWXT delivered EPS of $1.08 versus $0.91 expected (+18.7% YoY revenue growth), and set FY2026 guidance of $4.55–$4.70 EPS.

Why Now: The convergence of two mega-themes, the defense spending surge driven by the Iran conflict and the nuclear renaissance driven by AI data center power demand, gives BWXT twin catalysts that most investors are not yet pricing. BTIG recently raised its target to $235 (from $225), citing strong execution and expanding nuclear commercial opportunities. The consensus Buy rating from 16 analysts with an average target of $204 represents modest near-term upside, but BTIG’s $235 and proprietary model targets of $256 reflect the full bull case.

Risk: Insider selling activity is notable (CEO sold 10,000 shares); the forward PEG of 9.68x is elevated, meaning execution risk is high.

Opportunity #2, International Seaways (NYSE: INSW)

Current Price: ~$71–72 | Market Cap: ~$2.2B | Sector: Oil Tanker / Shipping

Overview: International Seaways is a medium-sized tanker company operating a fleet of crude and product tankers, and it is the most direct financial beneficiary of the oil supply disruption caused by the Strait of Hormuz crisis. When oil shipping routes are disrupted, tanker rates surge, and INSW captures that premium directly. The company just reported record Q4 net income and its largest-ever quarterly dividend (combined $2.15/share), generating a one-year total shareholder return of 143.19%.

Why Now: INSW has surged +51.44% in just 12 weeks and posted record financial results. Seven analysts rate it Buy, with Deutsche Bank at a $80 price target. The forward P/E of 9.22x is deeply discounted versus sector peers (sector median 39.7x), giving the stock a genuine value argument alongside its cyclical momentum. If the Iran conflict persists, which is the base case, global tanker utilization remains at elevated levels, supporting dividend sustainability.

Risk: A ceasefire deal would be a significant headwind; tanker rates and stock prices could correct sharply on geopolitical resolution. This is a high-beta event-driven trade with a clear negative catalyst.

Opportunity #3, Kinetik Holdings (NYSE: KNTK)

Current Price: ~$48.60 | Market Cap: ~$7.9B | Sector: Midstream Energy

Overview: Kinetik Holdings is a gathering and processing midstream energy company focused in the Permian Basin, one of the most prolific U.S. oil and gas production areas. Unlike upstream producers, which are exposed to commodity price volatility, Kinetik’s fee-based business model means it captures volume-driven revenue regardless of the exact price of oil. Its projected adjusted EBITDA CAGR of approximately 8% through 2030, the highest among gathering and processing peers per Jefferies, reflects the structural growth of Permian production.

Why Now: Two fresh upgrades came in just the past week: Wells Fargo upgraded KNTK from Hold to Buy (target raised to $52), and Truist Securities initiated coverage at Strong Buy with a $53 target. Kinetik also beat Q4 2025 earnings expectations, with revenue of $464M versus $449M estimated, triggering a 10.9% single-session gain. The dividend yield is compelling for an energy infrastructure name with this growth profile, and the company is positioned as an M&A target within midstream consolidation.

Risk: An EPS miss of $0.03 vs. $0.32 expected in Q3 2025 showed operational execution risk at this growth stage; the current ratio of 0.69x suggests some liquidity tightness.

The Week Ahead: April 1–5, 2026

Key Events to Watch:

-

April 6, Iran Strait of Hormuz Deadline: President Trump’s extended deadline for Iran to reopen the oil route expires. This is the single most market-moving event of the week, a confirmed deal sends oil sharply lower and triggers a broad relief rally; escalation could push Brent above $110+ again.

-

Q1 Earnings Season Acceleration: Nike (NKE), Beyond Meat (BYND), and McCormick (MKC) report this week. Consumer-facing names will be the first barometer of how the energy shock is affecting discretionary spending.

-

Fed Speakers: Vice Chair Michelle Bowman and other FOMC members are scheduled to speak publicly. Any dovish signals, or, conversely, any hawkish language affirming the “no rush to cut” stance, will move rate-sensitive equities.

-

Manufacturing & Services PMI Data (ISM): March ISM Manufacturing and Services reports will test whether the U.S. economy is still growing amid the oil shock or beginning to slow materially.

-

PCE Inflation Data: The Fed’s preferred inflation measure arrives Friday. Given the import price surge of 1.3% in February, the reading will be closely watched as a catalyst for either repricing rate-cut expectations or confirming the stagflationary base case.

Bottom Line for the Week Ahead: The market remains in a binary state. Risk assets are suppressed by geopolitical uncertainty, and any confirmed progress on Iran will release substantial pent-up buying energy. Maintain a barbell: keep exposure to energy (CVX, XOM) and defense (RTX, LMT) as the structural core, while holding selective positions in AI infrastructure names (SNDK, MU on dips) for the eventual macro normalization trade. Cash reserves remain valuable ahead of the April 6 binary event.

StockResearch Intelligence Weekly is published each Sunday for the week just concluded. All data as of market close Friday, March 27–28, 2026. Next edition: #12, week ending April 5, 2026.