StockResearch Intelligence Weekly #12

1. One Week of Relief. Five Weeks of Reality.

The week ending April 5, 2026 delivered the first winning week for US equities since the beginning of the Iran conflict, as all three major indexes snapped five-week losing streaks on optimism that the war could be approaching an endgame. The S&P 500 gained 3.4% to close at 6,582.69, the Nasdaq surged 4.4% to 21,879.18, and the Dow climbed 3.0% to 46,504.67, with the Russell 2000 contributing an additional 3.3% advance. The week was holiday-shortened due to Good Friday, with the March jobs report — a robust 178,000 payrolls addition and an unemployment rate dipping to 4.3% — released as markets were closed. Despite the weekly relief rally, context matters: the S&P 500 recorded its worst first quarter since 2022, declining 4.6% over Q1 2026, and the geopolitical backdrop remains exceptionally fluid, with WTI crude ending the week near $111/barrel and the Strait of Hormuz still operating at a fraction of its normal capacity.

2. Strengths

-

Relief Rally Grounded in Genuine Catalyst: Tuesday’s surge — the S&P 500’s largest single-day gain since May 2025 — was anchored by President Trump’s public comments suggesting the Iran conflict could conclude within two to three weeks. This is a fundamentally different rally driver than speculative optimism; it reflects repricing of geopolitical risk premium rather than rotation noise.

-

Equal-Weight and Small-Cap Resilience: Beneath the mega-cap headlines, the equal-weight S&P 500 actually closed Q1 in positive territory, and the Russell 2000 ended Q1 with modest gains — evidence that broadening participation outside of tech concentration supports the underlying market structure. Small- and mid-cap stocks outperformed their large-cap counterparts for the quarter.

-

Q1 Earnings Season Entering with Upgraded Expectations: Heading into April, analysts have revised Q1 2026 S&P 500 earnings estimates upward to 13.2% year-over-year growth (from 12.8% at the start of the quarter), with the index on track for its sixth consecutive quarter of double-digit earnings growth. The full-year 2026 EPS growth forecast stands at 17.4%, providing structural earnings support for patient investors.

3. Weaknesses

-

Stagflation Risk Intensifying: With WTI crude near $111 and Brent above $109 — a 52%+ surge in U.S. crude during March alone — the Iran war “tax” is beginning to filter through the real economy. Diesel at $5.38/gallon, air freight rates up 70%, and war-risk insurance premiums surging over 1,000% are compressing corporate margins and consumer purchasing power. The Federal Reserve is caught in a stagflation trap: it cannot cut rates while inflation reaccelerates from energy shocks, yet economic growth faces an oil-driven headwind.

-

Hormuz Blockade Threat Remains Acute: The Strait of Hormuz — through which approximately 20% of global oil, product, and gas supply passes — is operating at roughly six transits per day versus a normal 130. As long as this chokepoint remains effectively closed, every geopolitical headline acts as a market volatility amplifier. The IEA has characterized the disruption as exceeding the oil shocks of 1973, 1979, and the Russian gas cut combined.

-

Fed Paralysis Delays Rate Cut Relief: The March FOMC held rates steady as the Iran conflict complicated the disinflation trajectory, raising the 2026 core PCE forecast to 2.7%. Twelve of nineteen Fed officials still pencil in at least one cut in 2026, but the wide range of outcomes makes guidance unreliable. Markets cannot price in rate cut relief with confidence, removing a key support mechanism that drove the 2024-2025 bull market.

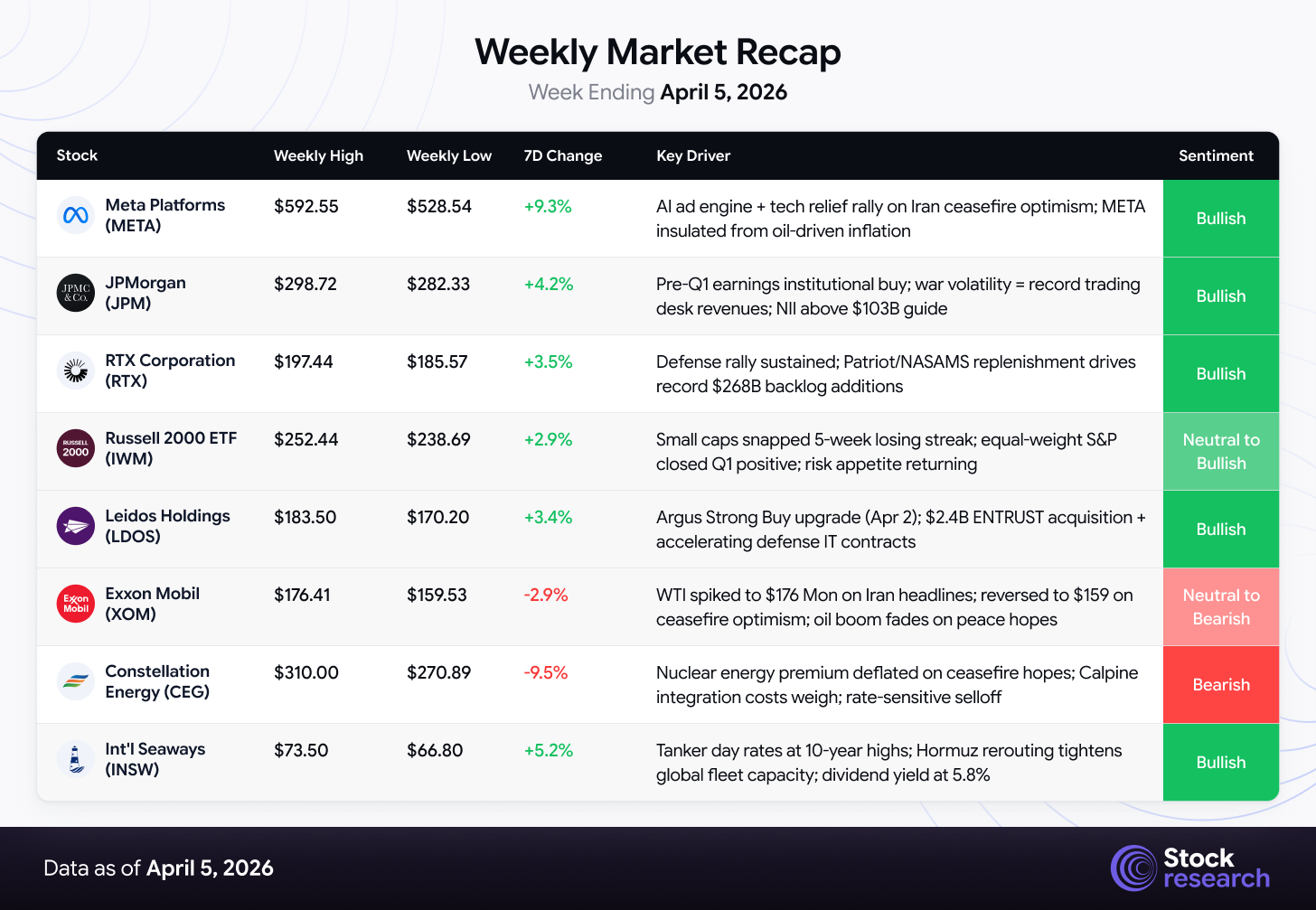

4. Weekly Market Recap – Week Ending April 5, 2026

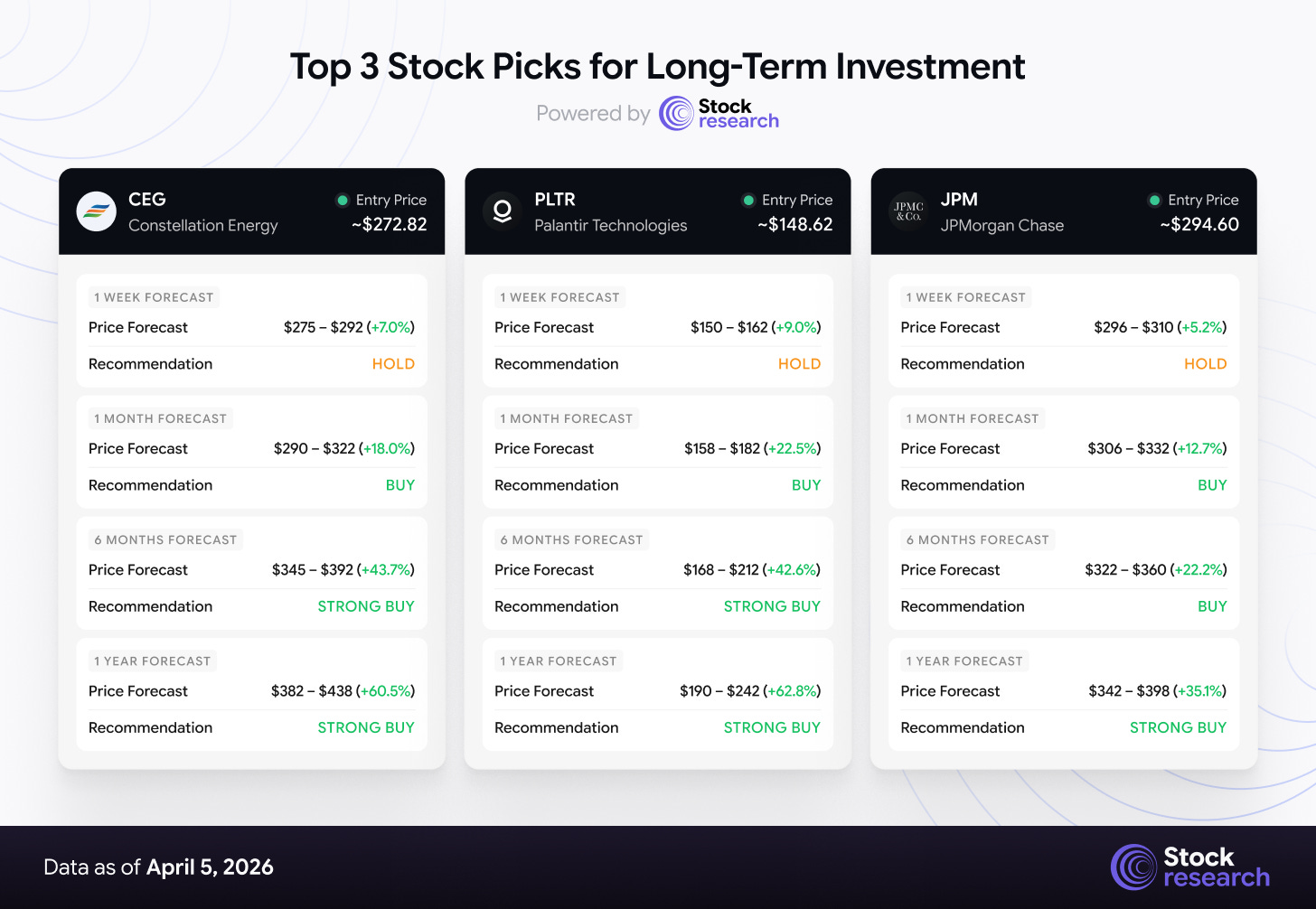

5. Top 3 Stock Picks for Long-Term Investment

AI Price Forecast Dashboard

Powered by StockResearch AI — Updated Week Ending April 5, 2026

A. Constellation Energy (CEG) | ~$272.82

Investment Horizon Recommendation:

-

1 Week: BUY (oversold at −38% from ATH; Morgan Stanley Overweight re-initiated at $385; technical support forming near $270)

-

1 Month: BUY (Q1 2026 earnings — first full quarter consolidating Calpine; analyst re-rating cycle beginning)

-

6 Months: STRONG BUY (new hyperscaler nuclear supply deals likely; $2B annual FCF uplift reaching full run-rate; nuclear PTC clarity expected)

-

1 Year: STRONG BUY (Calpine fully integrated; domestic energy security premium structurally repriced; infrastructure-grade multiple realization)

B. Palantir Technologies (PLTR) | ~$148.62

Investment Horizon Recommendation:

-

1 Week: HOLD/BUY (suited for staged entry; technically recovering from $140 lows)

-

1 Month: BUY (Q1 earnings approaching; $7.19B guide implies strong tracking; AIP contracts accelerating)

-

6 Months: BUY (defense AI entrenchment post-Iran war; $4.26B Q4 bookings converting to revenue)

-

1 Year: STRONG BUY (70% compounding drives normalization; Citi $235 target implies 58% upside)

C. JPMorgan Chase (JPM) | ~$294.60

Investment Horizon Recommendation:

-

1 Week: STRONG BUY (April 14 Q1 earnings is the single most actionable near-term catalyst; pre-positioning window is now)

-

1 Month: STRONG BUY (Q1 beat expected; NII tracking above $103B annual guide; analyst upgrades to follow)

-

6 Months: BUY (IB fee recovery compounding; Basel III rollback buybacks; higher-for-longer NII)

-

1 Year: BUY (EPS compounding to $24+; deregulation dividend realized; 15–16x re-rating)

6. Low-Cap Stock Opportunities: Undiscovered Value

The New Small-Cap Setup: Defense Tech, Tankers, and Sleep Medicine Disruptors

This week’s low-cap selection pivots meaningfully from prior editions’ focus on AI semiconductors and automotive aftermarket plays. The Iran war has created three distinct low-cap opportunity pools that remain underappreciated by the broader market: defense IT contractors benefiting from digitization of warfare, crude tanker operators directly profiting from Hormuz routing disruptions, and specialty pharma companies positioned in the now-validated sleep disorder market. The equal-weight S&P 500 and small-cap indices closing Q1 in positive territory — while mega-cap tech struggled — confirms that institutional rotation into quality, cash-generative smaller companies is a real and ongoing phenomenon.

Three structural factors support continued low-cap outperformance in this specific environment:

-

Geopolitical Defense Spending Lock-In: The Iran conflict has not just created a one-time procurement spike — it has exposed U.S. and allied inventory gaps that will require multi-year replenishment programs. Defense IT and services contractors with long-term government contracts are uniquely insulated from energy inflation (government contracts typically include cost-escalation provisions) while benefiting from accelerated digital warfare spending.

-

Tanker Market Structural Dislocation: The rerouting of global crude flows away from the Persian Gulf is extending voyage times, tightening effective fleet capacity, and driving tanker day rates to multi-year highs. Unlike crude prices (which can reverse overnight on ceasefire news), tanker rate improvements take months to unwind as fleets reposition and new bookings are contracted at elevated rates.

-

Sleep Medicine Validation by Lilly: Eli Lilly’s $7.8 billion Centessa acquisition has effectively put a major-pharma valuation floor under the entire orexin-pathway sleep medicine space. Smaller companies operating in this niche — particularly those with differentiated mechanisms or commercial revenue — are now operating in a sector where a single large-cap acquirer just demonstrated willingness to pay 40%+ premiums for early-stage pipeline assets.

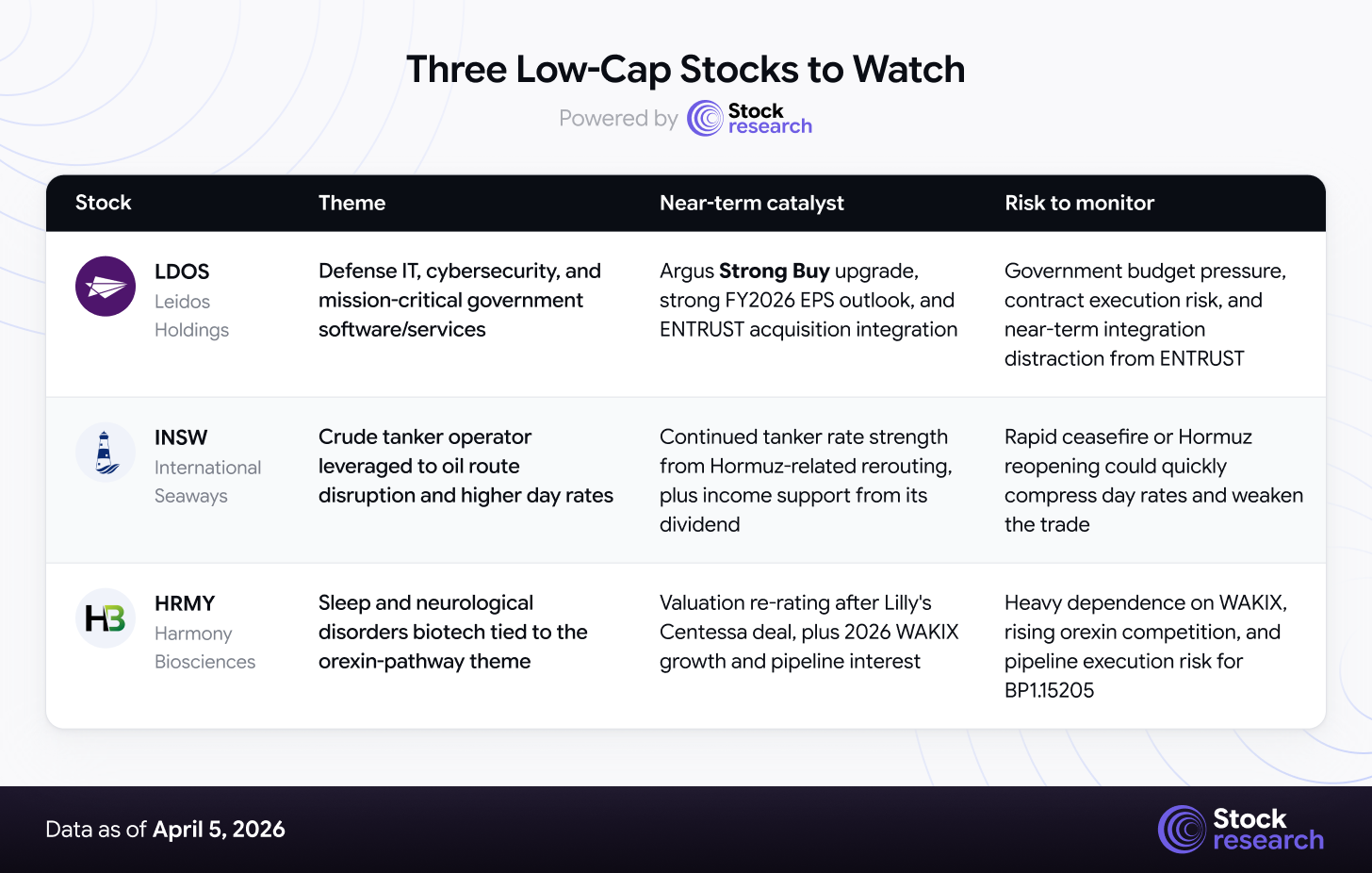

Three Low-Cap Stocks to Watch

A. Leidos Holdings (LDOS) | ~$20B Market Cap — Defense IT & Cybersecurity

Leidos is the “hidden champion” of the defense technology sector: a $20 billion market cap company managing national security IT, AI-driven command-and-control systems, cybersecurity, and mission-critical logistics for the U.S. Department of Defense and intelligence agencies. Unlike traditional defense primes (Lockheed, Northrop) that build hardware, Leidos monetizes the software and services layer — the fastest-growing component of modern defense budgets.

The Q4 2025 earnings report delivered $2.76 EPS against a $2.57 consensus estimate (+7.4% beat) and $4.88 billion in revenue versus $4.31 billion expected (+13.2% revenue beat). Management set FY2026 EPS guidance at $12.05–$12.45, well above prior year levels. The company also completed its $2.4 billion acquisition of ENTRUST Solutions Group in late March, creating a scaled utility cybersecurity and grid modernization services platform that positions Leidos in the AI-driven energy transition space.

Argus upgraded Leidos to Strong Buy this week, joining a consensus of one Strong Buy, seven Buys, and five Holds with an average analyst price target of $207–$211 — approximately 31% above the current trading price near $156. At 14x earnings with accelerating EPS growth, Leidos trades at a significant discount to both the broader market and its own historical multiples.

Why it matters: Pure-play U.S. government technology exposure with mission-critical contract structures, cybersecurity leadership at a moment when digital warfare is accelerating, and a valuation that fails to reflect the company’s quality of earnings. Key risks: Government budget sequestration risk, contract execution challenges, and the ENTRUST integration absorbing management attention in the near term.

B. International Seaways (INSW) | ~$3.73B Market Cap — Crude Tanker Operations

International Seaways is a crude and product tanker operator that owns and manages a fleet of 70 vessels — VLCCs, Suezmaxes, Aframaxes, and product carriers — that are directly and immediately benefiting from the Strait of Hormuz closure. When Gulf crude can no longer flow through the Strait, every barrel of oil destined for Asia must be rerouted around the Cape of Good Hope, adding weeks to voyage times and consuming far more tanker capacity per cargo unit. This is structurally bullish for day rates and earnings in a way that cannot be quickly reversed even if a ceasefire is announced tomorrow.

INSW’s Q4 2025 revenue surged 37.6% year-over-year, and the company completed the acquisition of the remaining 50% stake in Tankers International Limited in January 2026, consolidating its commercial pooling position. The stock has rallied nearly 60% in the past three months and now carries a 5.81% dividend yield at current prices, providing income support even as the stock price appreciation accrues.

Analyst consensus is Strong Buy with three analysts covering the name. At a forward P/E of approximately 10.55x and P/B well below the shipping sector average, INSW remains attractively valued even after the recent rally. The tanker market historically takes 6–18 months to fully normalize after a major route disruption, suggesting the earnings tailwind has room to run even beyond a potential Iran ceasefire.

Why it matters: Direct, liquid exposure to the oil supply disruption with income support from a 5.8%+ dividend yield. Key risks: Rapid war resolution and Hormuz reopening would compress day rates sharply; the stock’s beta to oil prices is negative (beta -0.22), meaning it can decouple from broader market moves in ways that surprise investors.

C. Harmony Biosciences (HRMY) | ~$2B Market Cap — Sleep & Neurological Disorders

Harmony Biosciences became dramatically more interesting this week as Eli Lilly’s $7.8 billion Centessa acquisition reset the valuation benchmark for the entire orexin-pathway sleep medicine space. Harmony is a profitable, growing specialty pharma company with WAKIX (pitolisant), the only FDA-approved non-scheduled drug for excessive daytime sleepiness in narcolepsy — a fundamentally different mechanism from traditional stimulants and one that Lilly just confirmed is worth multi-billion-dollar acquisition premiums.

The company guided to over $1 billion in WAKIX revenue for 2026, which would mark blockbuster status and a major commercial milestone. At approximately $2 billion market cap, Harmony is trading at roughly 2x its projected 2026 revenue from WAKIX alone — before accounting for its pipeline, including BP1.15205, a potentially best-in-class OX2R agonist with first-in-human trial data expected in 2026. This is the exact same drug target (OX2R agonist for narcolepsy) that Lilly just paid $7.8 billion for in Centessa’s earlier-stage program.

Wall Street analyst consensus is Buy with a median price target of $46.00 — representing approximately 27.7% upside from current levels. The InvestingPro Health Score of 3.66/5 places Harmony among the top-rated stocks in its sector for financial health and growth quality. The Lilly/Centessa deal has effectively placed Harmony on the M&A radar of every major pharma company seeking to build a sleep medicine franchise.

Why it matters: Profitable, revenue-generating specialty pharma company in a suddenly validated M&A-active sector, trading at a discount to its blockbuster growth potential. Key risks: Single-drug revenue concentration in WAKIX; increasing competition from orexin agonists entering the market (including potentially Centessa’s pipeline post-Lilly acquisition); pipeline execution uncertainty for BP1.15205.

7. Strategic Recap & Forward Outlook

-

Iran War as the Market’s Master Variable: Every sector rotation, every Fed decision, and every earnings revision model in April 2026 is subordinate to a single question: when and how does the Iran conflict resolve? The week’s 3–4% gains reflected hope of resolution; Thursday’s reversal on escalation headlines demonstrated that the market is pricing an uncertain probability distribution over outcomes. Investors should maintain exposure to beneficiary sectors (energy, defense, tankers) while sizing positions to tolerate headline volatility.

-

Earnings Season Will Surprise — But Guide Lower: Q1 2026 earnings growth is tracking at 13.2% year-over-year — impressive on its face. However, the key market-moving variable will be Q2 and full-year guidance. Companies with significant energy input cost exposure will almost certainly revise down 2026 guidance given $110+ crude, and airlines, consumer discretionary, and manufacturing names face acute margin compression. Seek companies that can pass costs through (defense, energy) or are insulated from them (software, healthcare).

-

Fed Paralysis Creates Duration Risk: With core inflation forecast at 2.7% and energy adding further upward pressure, the “Fed put” that backstopped markets in 2024 is currently suspended. The April 10 CPI report (March data) is the single most important economic data point of the month — a hot reading could push rate cut expectations from June to September and trigger a de-rating of rate-sensitive sectors.

Forward Outlook (Week Ending April 12, 2026)

The coming week is front-loaded with critical data and the beginning of Q1 earnings season. April 10’s March CPI report will anchor rate cut expectations and determine whether markets can sustain the relief rally or face renewed pressure from sticky inflation. Bank earnings from JPMorgan, Bank of America, and Citigroup will provide the first hard data on how the Iran war oil shock is affecting loan demand, net interest margins, and trading revenues — sectors that have underperformed significantly in Q1.

Technology names will also be under scrutiny as the Nasdaq’s 4.4% weekly gain invites skepticism: can the AI infrastructure spend thesis hold amid stagflation pressures that compress corporate IT budgets? TSMC’s quarterly report and guidance will be closely watched for signs that hyperscaler AI capex remains committed despite energy cost inflation.

Geopolitical developments continue to dominate. Oil at $111+ is unsustainable for the global economy without demand destruction, and markets will be tracking any ceasefire developments with extreme sensitivity in both directions. A confirmed ceasefire would trigger a violent rotation out of energy and defense into tech and consumer names; a further escalation (Iranian civilian infrastructure strikes, expanded conflict) could push crude toward $130–$150 and reignite stagflation fears with full force.

Positioning favors selective allocation to energy and defense beneficiaries (XOM, RTX, INSW) while maintaining exposure to quality healthcare names with durable growth (LLY, HRMY) that are insulated from both energy cost inflation and geopolitical disruption. Reduce exposure to high-multiple consumer discretionary, pure-play tech software, and rate-sensitive financial names until the CPI trajectory and Iran war resolution timeline become clearer. Maintain modest cash buffers given elevated VIX (23.9) and the potential for sudden headline-driven volatility in either direction.

Disclaimer

This analysis is for informational purposes only and should not be construed as investment advice. Equity markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Price targets are based on analytical frameworks and current market data but involve significant uncertainty. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.