StockResearch Intelligence Weekly #2

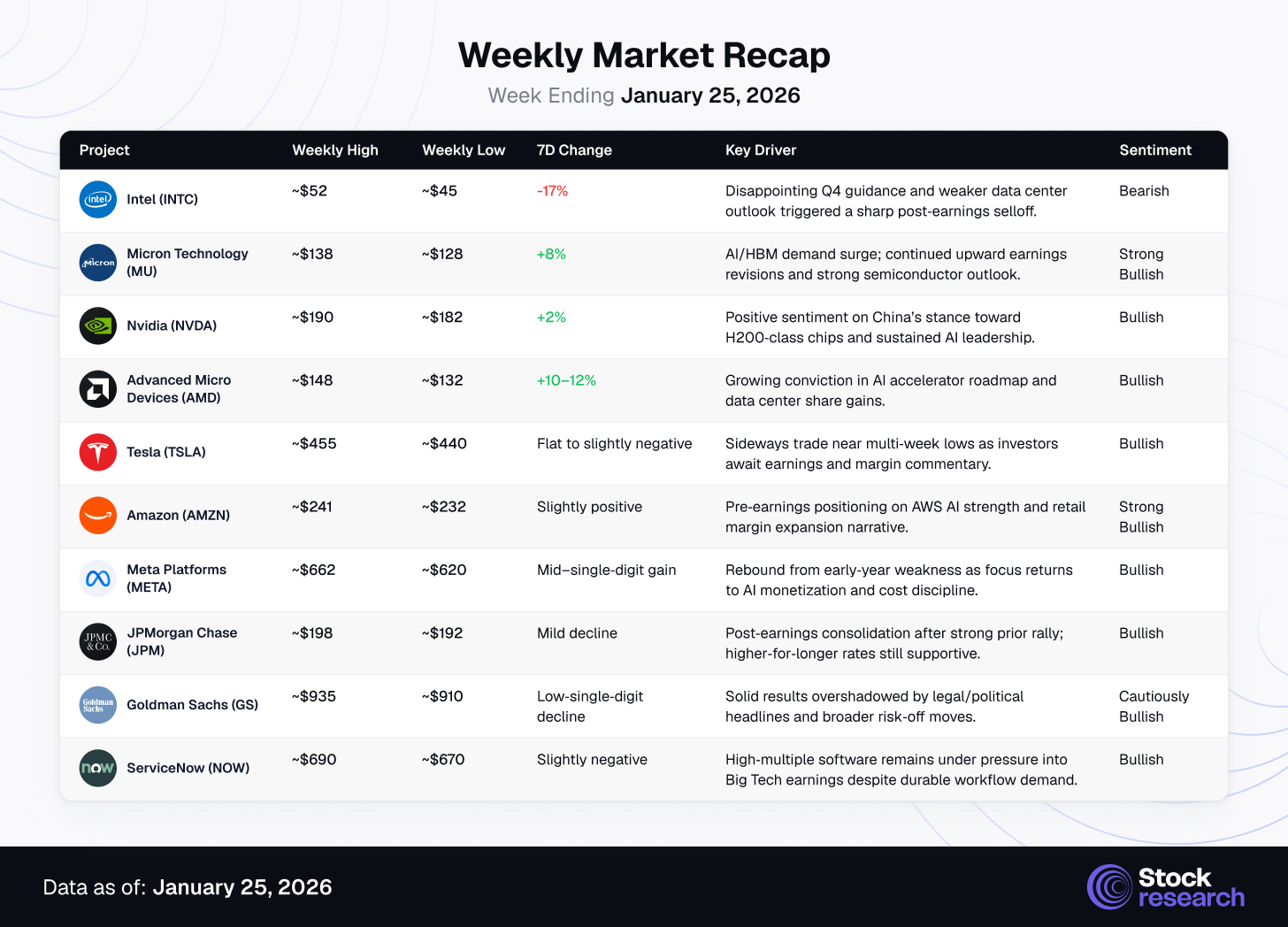

During the week of 19–23 January 2026, the US equity market traded near record highs with the S&P 500 consolidating around the upper‑6,000s as volatility quickly compressed after a brief tariff‑related spike. Leadership favored Technology, Communication Services, and Consumer Discretionary on continued AI enthusiasm, while Energy and Consumer Staples lagged and investors rotated selectively toward financials and small caps. A still‑robust macro backdrop, with real GDP growth running above trend and the Fed funds rate in the mid‑3% range, underpinned risk sentiment even as inflation near 2.8% kept expectations for only gradual policy easing. Earnings season supported the broader market, but narrative focus shifted from narrow mega‑cap tech leadership to a more diversified, infrastructure‑ and cyclicals‑friendly phase of the bull market.

Strengths

-

Small-Cap Outperformance Structural, Not Speculative: The Russell 2000 has outperformed the S&P 500 by 8.5% YTD, reflecting genuine institutional capital rotation driven by valuation dislocations (small caps trade at 30% discount to large caps on forward P/E) and superior small-cap earnings growth expectations for 2026.

-

Financial Sector Validates Resilience: Major banks’ strong Q4 results, coupled with deposit franchise durability and net interest margin expansion, confirm the consumer remains resilient and economic recession risk remains manageable near-term.

-

Manufacturing PMI Expansion Signals Broad-Based Growth: Both Flash Manufacturing PMI (51.9) and Services PMI (52.5) came in above 50, confirming economic expansion beyond mega-cap tech, validating small-cap and industrial sector momentum.

Weaknesses

-

Mega-Cap Tech Execution Risk Rising Sharply: Intel’s 17% single-day decline following guidance disappointment and AI chip demand constraints signals real cash flow vulnerability in the semiconductor supply chain. If other mega-cap tech players (Microsoft, Meta, Apple, Nvidia) disappoint on earnings, rapid repricing becomes likely.

-

Valuation Extension at Dangerous Levels: The “Magnificent Seven” mega-cap tech stocks trade at average forward P/E ratios exceeding 28x, while the broader S&P 500 trades at 18.5x. AI ROI visibility remains murky; if capex returns disappoint, multiple compression will be swift and severe.

-

Geopolitical Uncertainty Unresolved: Greenland deal framework notwithstanding, U.S.-China trade tensions, Taiwan vulnerability, and Middle East escalation risks remain material headwinds. VIX briefly exceeded 20, suggesting latent market fragility beneath surface complacency.

Market Recap

AI infrastructure beneficiaries such as Micron, Nvidia, and AMD continued to attract flows, while Intel’s earnings stumble highlighted how little tolerance markets have for execution missteps at elevated valuations. Mega-cap platforms like Amazon and Meta traded as “event assets” into an earnings-heavy week and the upcoming Fed decision, while money center banks and high-quality software names saw tactical de-risking rather than thesis breaks.

Top 3 Stock Picks for Long-Term Investment

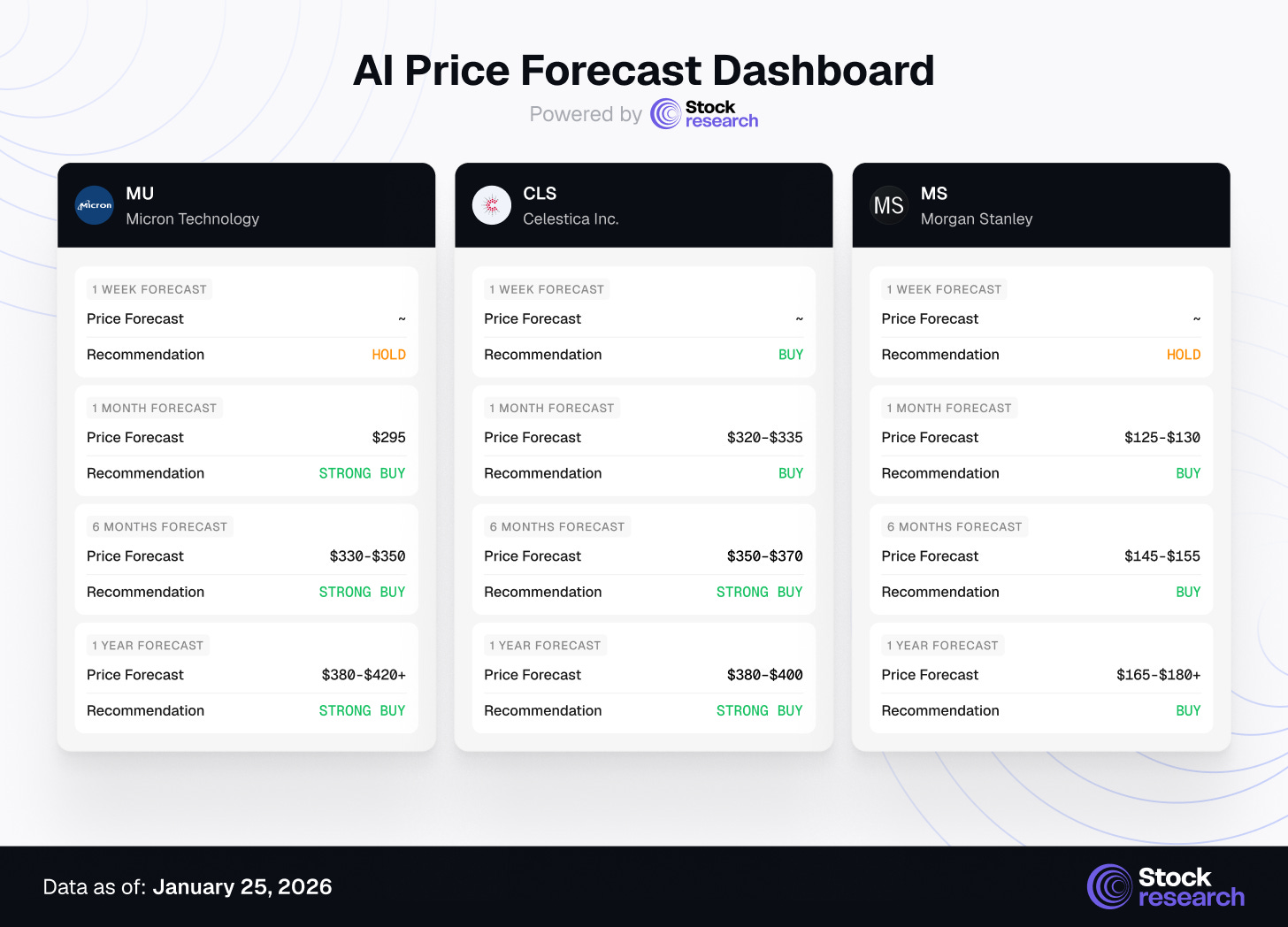

1. Micron Technology (MU) | Semiconductor & AI Infrastructure

Investment Horizon Recommendation:

-

1 Week: HOLD (consolidation expected; earnings catalyst imminent)

-

1 Month: STRONG BUY (earnings report + AI demand acceleration)

-

6 Months: STRONG BUY (HBM/DRAM cycle expansion; hyperscaler capex)

-

1 Year: STRONG BUY (structural AI infrastructure upcycle)

Thesis: Micron has cemented its position as the definitive AI infrastructure beneficiary, commanding unmatched exposure to the High-Bandwidth Memory (HBM) shortage that is the critical bottleneck constraining AI model training. The company’s recent commentary confirms record data center orders, with customer commitments extending through 2026 and into 2027. Micron’s FY2026 revenue is projected to grow 89.3%, while earnings are on track to exceed 100% growth—numbers that are not speculative but rather underpinned by multi-year customer agreements with hyperscalers (Microsoft, Amazon, Google, Meta).

The semiconductor cycle is bifurcated: commodity DRAM facing near-term headwinds, but HBM pricing and demand accelerating at an unprecedented pace. Micron’s strategic pivot toward high-margin HBM products is driving operating leverage and margin expansion that will support multiples re-rating if execution remains flawless.

Catalysts:

-

HBM Supply Constraint Resolution: Micron is the only chipmaker capable of scaling HBM3E production to meet hyperscaler demand, creating a structural pricing power environment lasting through 2026-2027.

-

Earnings Momentum Inflection: Zacks consensus estimates for FY2026 earnings have risen 64.2% over the past 30 days—a leading indicator of sustained positive estimate revisions and potential upside surprise on the earnings call.

-

Margin Expansion Trajectory: Gross margins are expanding as HBM, which commands 50%+ gross margins versus 35% for commodity DRAM, becomes a larger revenue mix contributor.

-

Cash Generation & Balance Sheet: Micron is generating record operating cash flow, providing capital allocation flexibility (buybacks, debt reduction, M&A optionality).

Key Risks:

-

Cyclical semiconductor inventory corrections if hyperscaler capex slows unexpectedly.

-

Geopolitical escalation involving Taiwan or China could disrupt advanced chip manufacturing.

-

Competitive entrants (SK Hynix, Samsung) accelerating HBM development timelines.

-

AI ROI disappointment could trigger capex pullback from hyperscalers.

Price Targets (analyst consensus + fundamental analysis):

-

1 Month: $295 (modest upside from current levels; consolidation likely)

-

6 Months: $330-$350 (accelerating HBM demand visibility)

-

1 Year: $380-$420+ (structural margin expansion; earnings growth acceleration)

Micron is the purest play on AI infrastructure buildout with genuine revenue and earnings visibility underpinned by multi-year customer commitments. The stock trades at reasonable valuations relative to growth—a rare feature in the current market environment.

2. Celestica Inc. (CLS) | AI Infrastructure Services & Electronics Manufacturing

Investment Horizon Recommendation:

-

1 Week: BUY (data center networking solutions gaining adoption)

-

1 Month: BUY (AI capex cycle acceleration)

-

6 Months: STRONG BUY (margin expansion from mix shift)

-

1 Year: STRONG BUY (structural capex cycle tailwinds)

Thesis: Celestica has emerged as a critical-but-overlooked beneficiary of the AI infrastructure buildout, providing electronics manufacturing services, design engineering, and supply chain solutions for hyperscale data centers. The company’s Connectivity and Cloud Solutions (CCS) division is experiencing explosive growth, driven by demand for custom data center networking switches—the critical infrastructure enabling rapid connectivity within AI data centers.

While investors focus on chip designers (Nvidia, Broadcom, AMD), they overlook the manufacturers and service providers who are capturing significant economic rents from hyperscaler infrastructure buildout. Celestica is designing and fabricating custom networking switches for leading-edge hyperscalers and AI chip suppliers, partnering with Broadcom, Marvell Technology, AMD, and Intel.

The company’s solid growth trajectory—31% top-line acceleration expected in 2026, coupled with 39% earnings-per-share growth to $8.20—reflects operating leverage from the AI infrastructure cycle that will compound for multiple years as capex intensity remains elevated.

Catalysts:

-

CCS Division Mix Expansion: As the CCS division (higher-margin services) grows faster than legacy electronics manufacturing, overall company margins expand and earnings multiples re-rate.

-

Hyperscaler Capex Persistence: Bank of America estimates the AI capex cycle is only halfway through an 8-10 year evolution, with data center infrastructure spending projected to hit $1.2 trillion by 2030.

-

Supply Chain Optionality: As manufacturing becomes supply-constrained and geopolitically complex, hyperscalers are diversifying manufacturing partnerships, benefiting diversified providers like Celestica.

-

Valuation Opportunity: Celestica trades at attractive multiples relative to expected earnings growth, offering asymmetric upside as market re-rates the company’s structural growth visibility.

Key Risks:

-

Margin pressure if hyperscaler capex slows or demand for custom switches decelerates.

-

Competitive pressure from larger contract manufacturers (Flex Ltd., Jaco Electronics).

-

Supply chain volatility in key component sourcing.

-

Customer concentration risk (significant revenue from leading hyperscalers).

Price Targets (analyst consensus + fundamental analysis):

-

1 Month: $65-70 (steady execution; modest upside)

-

6 Months: $80-90 (margin expansion; capex cycle confidence building)

-

1 Year: $100-110+ (sustained earnings growth; multiple expansion)

Celestica offers exposure to the AI infrastructure buildout through an often-overlooked manufacturing and services lens. With 30%+ expected earnings growth and reasonable valuations, the stock offers asymmetric risk-reward.

3. Morgan Stanley (MS) | Financial Services & Wealth Management Leadership

Investment Horizon Recommendation:

-

1 Week: HOLD (consolidation amid broader market uncertainty)

-

1 Month: BUY (earnings catalyst; wealth management momentum)

-

6 Months: BUY (capital markets activity expansion)

-

1 Year: BUY (secular wealth management tailwinds)

Thesis: Morgan Stanley represents the highest-conviction financial services play for 2026, combining defensive balance sheet quality with offensive growth optionality. The company’s strategic focus on wealth and asset management (now 55%+ of net revenue), coupled with its leading investment banking franchise and trading desk capabilities, positions MS to benefit from both an improved capital markets environment and secular wealth creation flows.

The EquityZen acquisition, announced in late 2025, represents a transformational move into the rapidly expanding private markets landscape—a secular growth area where MS can leverage its distribution and technology capabilities to capture outsized returns. Unlike traditional big banks with heavy legacy CRE exposure, Morgan Stanley has proactively de-risked its balance sheet and is positioned to grow earnings from higher-quality revenue streams.

Q4 2025 earnings demonstrated the power of this diversified revenue mix: wealth management net flows remained robust, investment banking activity accelerated from 2025 lows, and trading desk profitability remained healthy despite softer market conditions.

Catalysts:

-

Wealth Management Operating Leverage: Rising AUM (assets under management) from market appreciation and continued client flows, combined with disciplined cost management, are driving operating margin expansion.

-

Capital Markets Activity Acceleration: IPO and M&A activity are inflecting positively as economic certainty improves and capital availability expands; MS’s fee-based businesses will capture significant economics.

-

Private Markets Expansion (EquityZen): The EquityZen acquisition positions MS as a leading distributor of private equity and private credit to its wealth management client base—a secular growth opportunity.

-

Capital Return Optionality: With fortress balance sheet strength and improving capital generation, MS can increase shareholder returns (dividends, buybacks) while maintaining strategic flexibility.

Key Risks:

-

Recession-driven Asset Under Management (AUM) declines if equity markets correct sharply.

-

Credit cycle deterioration could impair investment banking and trading desk profitability.

-

Regulatory capital requirements remain a headwind to balance sheet optimization.

-

Competitive pressure from technology-native wealth platforms (Stripe, SoftBank Vision Fund).

Price Targets (analyst consensus + fundamental analysis):

-

1 Month: $125-130 (consolidation near current valuations)

-

6 Months: $145-155 (AUM growth + margin expansion)

-

1 Year: $165-180+ (capital markets recovery; EquityZen contribution)

Morgan Stanley offers a balanced exposure to financial sector resilience, capital markets cycle recovery, and secular wealth management growth. The stock trades at reasonable valuations relative to peer average while offering superior franchise quality and structural growth drivers.

Low-Cap Stock Opportunities: Undiscovered Value

As mega-cap stocks reach valuation extremes, institutional capital continues rotating into small-cap and micro-cap equities, creating asymmetric opportunities in companies with market capitalizations below $2B. These stocks benefit from discounted valuations, accelerating earnings growth, and limited analyst coverage—inefficiencies that disciplined investors can exploit.

The Russell 2000 has outperformed the S&P 500 by 8.5% YTD, with micro-caps leading the advance (Russell Microcap up 23% in 2025, the strongest performance in 25+ years). This move reflects valuation-driven rotation rather than speculation. Small-cap forward P/E ratios trade at a 30% discount to large caps on consensus estimates, while earnings growth expectations for small-caps are higher than large-caps for 2026—a rare and compelling setup that historically has driven multi-year outperformance.

The Small-Cap Setup: Why 2026 Is a Critical Inflection Point

Three structural factors support continued small-cap leadership:

-

Valuation Mean Reversion: Small-cap forward P/E ratios are near 25-year lows relative to large caps, offering deep discounts to historical averages.

-

Earnings Growth Inflection: For the first time in 13 quarters, small-cap earnings growth is outpacing large-cap earnings growth—a reversal of the mega-cap concentration trend.

-

Fed Pivot Benefits Small-Caps Disproportionately: If the Fed begins rate cuts in the second half of 2026, small-caps (higher leverage, greater interest rate sensitivity) will benefit more than large-caps from declining discount rates.

Three Low-Cap Stocks to Watch

-

Array Technologies (ARRY) | ~$1.8B

Solar tracking systems leader benefiting from IRA incentives and utility-scale solar expansion. Projects ~45% earnings growth while trading below 11x forward earnings.

Why it matters: Structural renewables growth at discounted valuation.

Key risks: Policy shifts and competitive pressure.

-

ScanSource (SCSC) | ~$650M

Specialty technology distributor focused on hybrid cloud, cybersecurity, and unified communications. Recurring revenue has grown to roughly one‑third of total sales, yet shares trade at ~8–9x forward earnings with a net cash position.

Why it matters: Under‑the‑radar cash‑rich compounder with growing services mix.

Key risks: SMB customer exposure and potential channel disintermediation.

-

Fluence Energy (FLNC) | ~$4.2B

Utility-scale energy storage provider enabling grid stability and renewable integration, backed by Siemens and AES. Revenue is expected to grow around 40% in 2026, with profitability inflecting after recent scale‑up.

Why it matters: Direct play on grid modernization and battery storage adoption.

Key risks: Project execution, battery supply constraints, and regulatory delays.

Strategic Recap & Forward Outlook

The week ending January 25, 2026 underscores a market navigating rotation rather than broad-based enthusiasm. U.S. equities saw modest headline weakness, even as small caps, semiconductor infrastructure, and select financials showed relative strength. Fed policy uncertainty, geopolitical tension, and elevated mega-cap valuations kept volatility elevated and limited risk appetite. Rotation into small caps, AI infrastructure, and high-quality banks is constructive, but sustainability hinges on dovish guidance at the January 28–29 FOMC meeting and resilient earnings from Big Tech and AI leaders.

Key Takeaways

-

Small-Cap Leadership Is Structural: The Russell 2000’s outperformance reflects institutional recognition of valuation dislocations and earnings growth acceleration—not speculative excess. Quality small-caps with strong balance sheets and secular tailwinds continue to offer asymmetric upside.

-

Mega-Cap Tech Execution Risk Is Rising: Intel’s 17% single-day decline following guidance disappointment signals real cash flow vulnerability in the semiconductor supply chain. If other mega-cap tech players disappoint on earnings this week, rapid repricing becomes likely.

-

AI Infrastructure Buildout Persists: Despite semiconductor sector weakness, the structural demand for AI infrastructure remains intact. Companies positioned along the entire AI value chain (chip designers, manufacturers, infrastructure providers) offer compelling risk-reward at current valuations.

-

Financial Sector Validates Economic Resilience: Strong Q4 bank earnings confirm consumer resilience and credit quality stability. JPMorgan, Morgan Stanley, and regional financials offer both defensive quality and cyclical upside.

-

Energy Infrastructure Recovery Is Underway: Geopolitical tensions, combined with renewed capital discipline and hyperscaler power infrastructure investment, are creating a multi-year tailwind for energy services providers.

Forward Outlook (Week Ending February 1, 2026)

Expect near-term choppiness as markets digest the January 28–29 FOMC decision alongside a dense slate of Big Tech earnings. Softer inflation tone and dovish messaging would likely extend the rally in small caps, semiconductors, and financials, while any hawkish surprise or weak guidance from mega-caps could trigger another leg of de‑risking in high‑multiple tech and software.

Risk Context: Headline trends still point to economic expansion, but underlying fragility persists. Elevated valuations in select growth franchises, concentration risk in mega-cap indices, policy uncertainty, and geopolitical noise create asymmetric downside if expectations are not met. Positioning should stay selective, with disciplined sizing, a quality bias, and sufficient cash to take advantage of volatility-driven dislocations rather than chase late‑cycle momentum.

Disclaimer

This analysis is for informational purposes only and should not be construed as investment advice. Equity markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.

The stocks mentioned in this report represent analysis based on publicly available data, analyst consensus estimates, and fundamental research. Price targets are directional estimates derived from consensus analyst expectations and fundamental analysis, not precise forecasts. Market conditions can change rapidly; investors should continuously reassess positions based on evolving fundamentals and market dynamics.