StockResearch Intelligence Weekly #3

During the week of January 27–31, 2026, the US equity market navigated significant volatility triggered by Big Tech earnings divergence and Federal Reserve policy decisions. The S&P 500 posted modest gains to close at fresh record highs near 6,100, while the tech-heavy Nasdaq experienced heightened turbulence following mixed reactions to Microsoft, Meta, Tesla, and Apple earnings reports. Small-cap outperformance continued with the Russell 2000 extending its remarkable winning streak, though momentum showed signs of fatigue toward week’s end. Meta emerged as the week’s clear winner with shares surging 10% on strong AI monetization results, while Microsoft plunged 12% to nine-month lows on cloud growth deceleration concerns. The Federal Reserve held rates steady at 3.5%-3.75% as expected, with Chair Powell maintaining a cautious stance on future cuts amid elevated inflation and political pressure. Market leadership remained bifurcated: defensive rotation into small-caps, financials, and selective AI infrastructure plays persisted, while high-multiple software and mega-cap tech faced profit-taking pressure.

Strengths

-

Small-Cap Outperformance Still Structural: The Russell 2000’s January outperformance and ~30% valuation discount to large caps signal ongoing institutional rotation driven by earnings growth, not speculation.

-

Fed Policy Credibility Intact: The FOMC’s unanimous decision to hold rates at 3.5–3.75% despite political pressure reinforces a data-dependent stance and supports risk assets.

-

Defense & Energy Tailwinds Building: Trump’s proposed $1.5T 2027 defense budget and persistent geopolitical tensions are driving renewed interest in defense and energy infrastructure names such as Kratos.

Weaknesses

-

Microsoft Cloud Slowdown Raises Capex Concerns: Azure growth deceleration and a 12% stock drop revived fears that AI infrastructure spending may normalize faster than expected.

-

High-Multiple Software Under Pressure: Enterprise software and workflow names remain in derating mode as investors question rich AI-driven valuations ahead of slower growth.

-

Fiscal & Political Risks Resurface: Ongoing budget standoffs and Department of Homeland Security funding disputes raise shutdown risks that could disrupt data, sentiment, and Fed signaling.

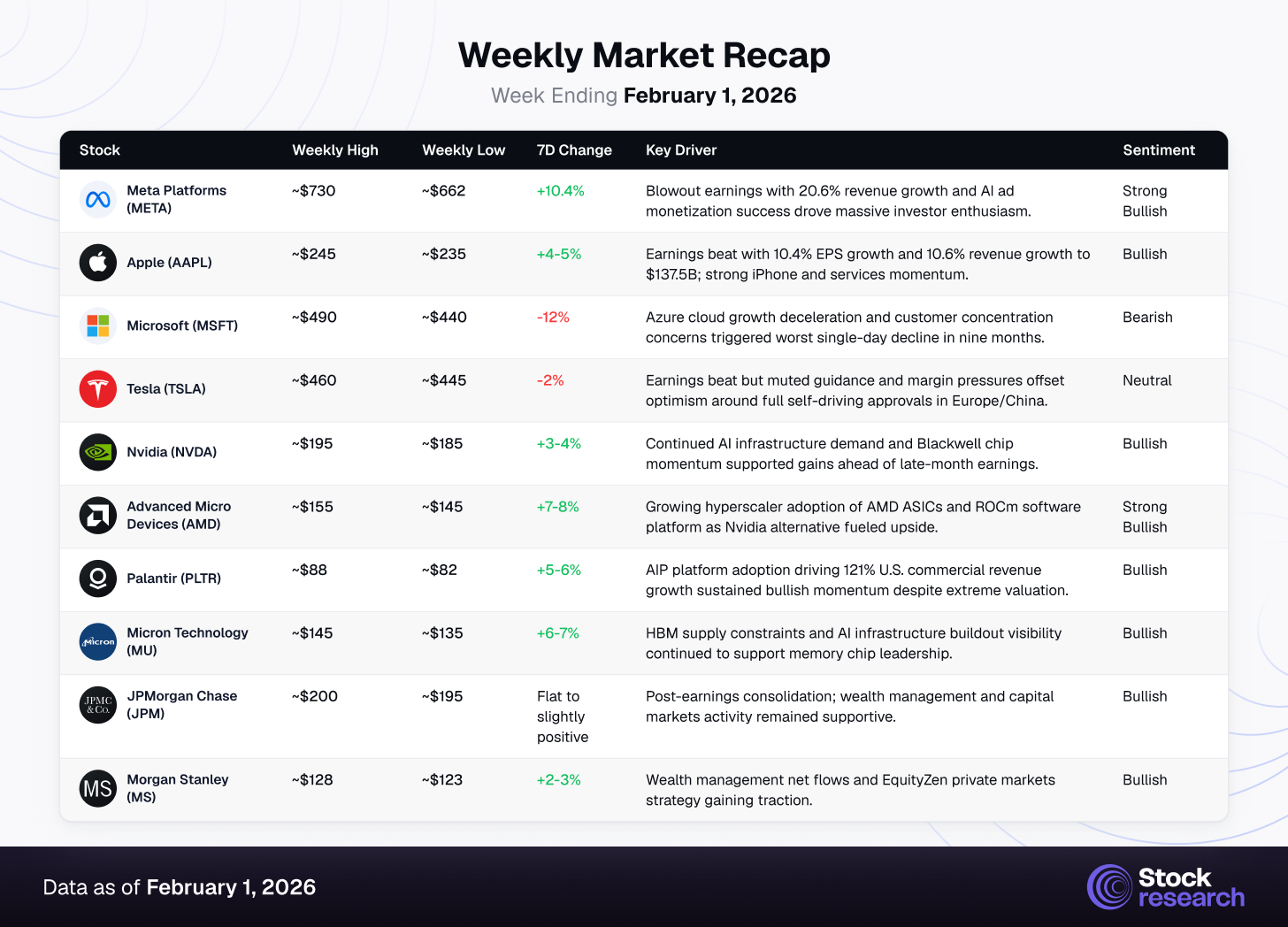

Weekly Market Recap

Week Ending February 1, 2026

The week highlighted the growing divergence within mega-cap tech: Meta’s AI revenue realization success contrasted sharply with Microsoft’s infrastructure spending caution. Small-caps extended their remarkable outperformance, though momentum cooled slightly as profit-taking emerged. Semiconductor infrastructure plays (AMD, Micron, Nvidia) continued to benefit from hyperscaler diversification and AI buildout demand, while traditional software stocks faced sustained pressure. Financial sector resilience persisted with Morgan Stanley and JPMorgan consolidating near highs on wealth management and capital markets strength.

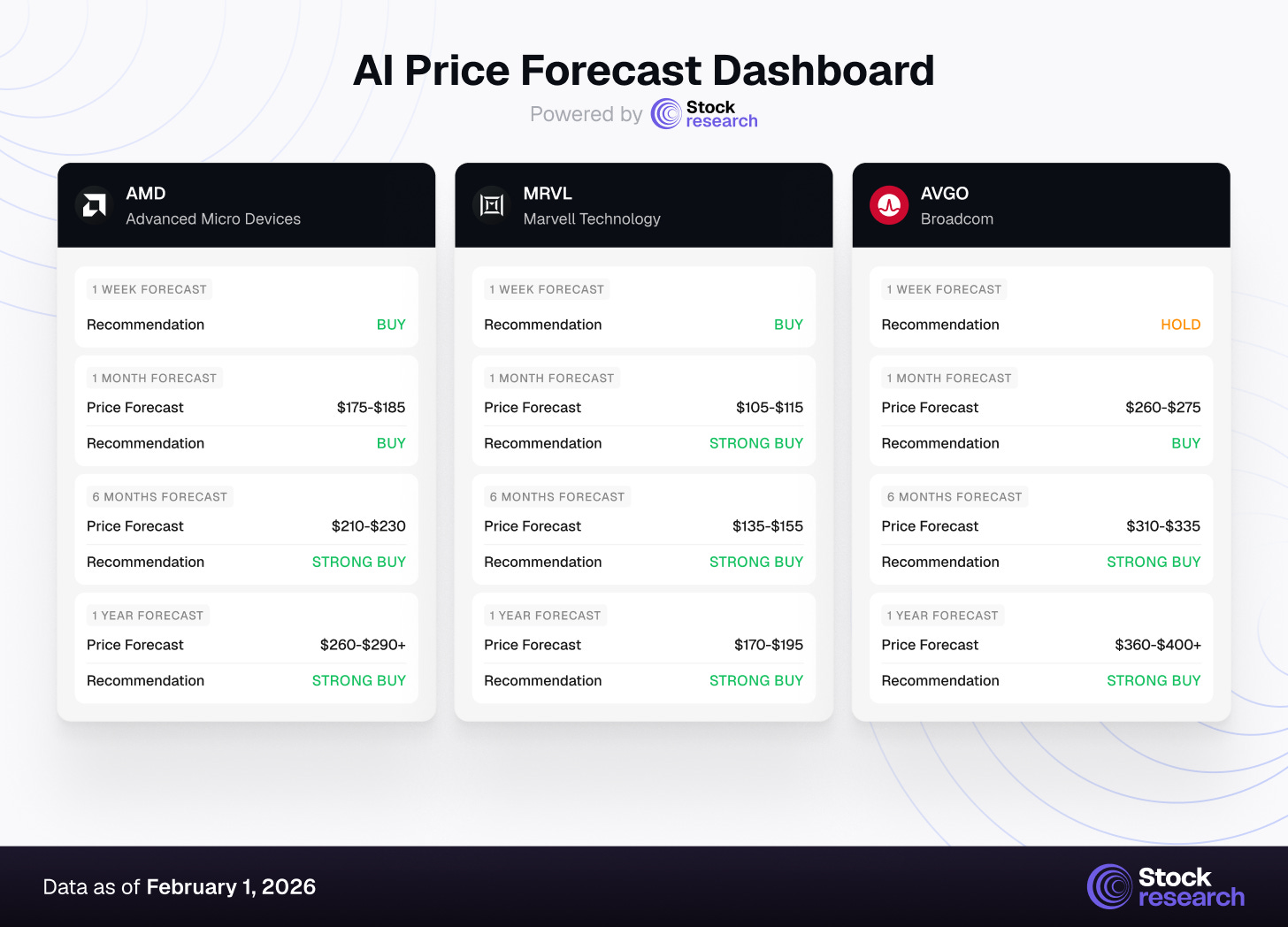

Top 3 Stock Picks for Long-Term Investment

AI Price Forecast Dashboard

Powered by StockResearch AI

1. Advanced Micro Devices (AMD) | Semiconductor & AI Infrastructure Diversification Play

Investment Horizon Recommendation:

-

1 Week: BUY (momentum from hyperscaler wins; technical breakout)

-

1 Month: BUY (data center share gains accelerating)

-

6 Months: STRONG BUY (ASIC market penetration and ROCm ecosystem expansion)

-

1 Year: STRONG BUY (structural AI diversification beneficiary)

Thesis: Advanced Micro Devices has emerged as the leading “second-source” AI accelerator, gaining share as hyperscalers diversify away from Nvidia to reduce concentration risk and improve economics. Its recent 7–8% weekly rally reflects growing recognition that AMD is not just a cheaper alternative, but a strategic vendor helping big tech balance cost, performance, and bargaining power.

AMD’s edge rests on three pillars: MI300 accelerators now deployed at scale for training and inference, the open-source ROCm platform that reduces CUDA lock-in, and a full-stack portfolio spanning CPUs, GPUs, and networking. With hyperscalers expected to spend over $500B on AI infrastructure in 2026, even incremental share gains position AMD for meaningful revenue growth and margin expansion, reinforced by multi-year contracts across all major cloud providers.

Catalysts:

-

Hyperscaler Diversification Imperative: Big tech’s strategic need to reduce Nvidia dependency creates sustained demand for AMD’s MI300 accelerators, with recent deployments across Microsoft Azure, Google Cloud, and Meta’s AI infrastructure confirming technical parity for production workloads.

-

ROCm Ecosystem Maturation: AMD’s open-source software platform is rapidly closing the gap with Nvidia’s CUDA, attracting enterprise developers seeking vendor flexibility and lower total cost of ownership. Recent partnerships with major AI framework providers (PyTorch, TensorFlow) accelerate adoption.

-

Revenue Inflection from Data Center Mix Shift: Data center segment revenue is projected to grow 40%+ in 2026, driven by accelerated AI accelerator adoption and CPU share gains in cloud servers. AMD’s data center margins are expanding as higher-value AI products become a larger revenue mix.

Risks: Nvidia’s deeply entrenched CUDA ecosystem, which still limits ROCm adoption, execution risk as AMD must keep pace with Nvidia’s aggressive chip roadmap, potential volatility in hyperscaler AI capex if spending slows, and geopolitical semiconductor risks tied to U.S.–China tensions and Taiwan-centric supply chains.

Price Targets:

-

1 Month: $175-$185 (consolidation above recent breakout levels; steady hyperscaler wins)

-

6 Months: $210-$230 (data center revenue inflection; margin expansion visibility)

-

1 Year: $260-$290+ (ASIC market share gains; structural AI diversification beneficiary)

AMD represents the highest-conviction AI infrastructure play for investors seeking exposure to hyperscaler diversification trends at reasonable valuations. Trading at 25x forward earnings—significantly below Palantir’s 243x and in line with Nvidia’s 38x—AMD offers asymmetric risk-reward as the company transitions from “challenger” to “co-leader” in AI accelerator markets. The stock’s recent momentum reflects institutional recognition of this strategic positioning shift.

2. Marvell Technology (MRVL) | Custom ASIC & AI Data Center Infrastructure

Investment Horizon Recommendation:

-

1 Week: BUY (positive momentum from AI infrastructure spending trends)

-

1 Month: STRONG BUY (custom ASIC demand acceleration)

-

6 Months: STRONG BUY (market share expansion in AI accelerator market)

-

1 Year: STRONG BUY (structural AI infrastructure beneficiary with 20-25% ASIC market share target)

Thesis: Marvell Technology has positioned itself as a key enabler of AI data centers through custom ASIC design and high-speed connectivity, capturing value beyond headline GPU players. By building bespoke accelerators for hyperscalers, Marvell helps optimize cost and performance for proprietary AI workloads while reducing reliance on standard GPUs.

With the custom ASIC market forecast to grow at 27% CAGR to $118B by 2033, Marvell is well placed to capture meaningful share, implying a large long-term revenue upside. Its optical, switching, and storage connectivity businesses further benefit from the surge in data movement as AI clusters scale, creating durable tailwinds alongside ASIC growth.

Catalysts:

-

Custom ASIC Design Win Acceleration: Marvell is actively engaged with all major hyperscalers on multi-year custom chip development programs, with increasing visibility into production deployments beginning in late 2026 and ramping through 2027-2028.

-

Data Center Connectivity Growth: As AI clusters scale from hundreds to thousands of GPUs per node, demand for Marvell’s 800G and 1.6T optical interconnects, switch silicon, and storage solutions is accelerating at unprecedented rates.

-

Market Share Gains from Broadcom: Marvell’s competitive positioning in custom ASIC design is strengthening relative to incumbent leader Broadcom, with hyperscalers seeking vendor diversification and Marvell offering differentiated IP and faster development cycles.

Risks: Heavy reliance on a small group of hyperscaler customers, rising competition from in-house silicon efforts, execution risk inherent in complex multi-year ASIC design programs, and valuation sensitivity if AI-related revenue growth or guidance falls short of expectations.

Price Targets:

-

1 Month: $105-$115 (near-term momentum from AI infrastructure trends; positive sentiment)

-

6 Months: $135-$155 (custom ASIC design wins becoming visible; revenue inflection)

-

1 Year: $170-$195 (market share gains validated; margin expansion trajectory confirmed)

Marvell represents a “picks and shovels” AI infrastructure play that has received insufficient investor attention relative to its strategic positioning. The company’s dual exposure to custom ASIC acceleration and data center connectivity provides diversified AI infrastructure upside at current valuations. With analyst average price target approximately 38% above current levels and sustained hyperscaler AI spending projected through 2027+, Marvell offers compelling risk-adjusted returns for long-term investors.

3. Broadcom (AVGO) | AI Accelerator & Networking Infrastructure Leader

Investment Horizon Recommendation:

-

1 Week: HOLD (near-term consolidation after strong year-to-date performance)

-

1 Month: BUY (earnings catalyst; AI custom silicon backlog visibility)

-

6 Months: STRONG BUY (sustained AI infrastructure spending; networking dominance)

-

1 Year: STRONG BUY (structural beneficiary of hyperscaler AI buildout)

Thesis: Broadcom is the incumbent leader in custom AI accelerators and hyperscale networking, supported by deep, decade-long relationships with hyperscalers and multi-year AI order visibility extending beyond 2027. Its portfolio spans custom ASICs, Ethernet switching silicon, and enterprise software, positioning the company at the core of large-scale AI infrastructure buildouts.

As AI data centers scale from hundreds to thousands of interconnected GPUs, Broadcom’s Tomahawk and Jericho switching silicon have become essential for low-latency, high-bandwidth connectivity, a key bottleneck in AI training. This combination of custom silicon expertise and critical networking IP forms a durable competitive moat.

Financially, AI-related revenue is expected to grow more than 40% in fiscal 2026, while Broadcom’s diversified business mix, including VMware, provides earnings stability and reduces cyclicality relative to pure-play semiconductor peers.

Catalysts:

-

Custom ASIC Backlog Conversion: Broadcom’s multi-year design agreements with hyperscalers (particularly Google TPU and other undisclosed customers) are transitioning from development to production deployment, driving accelerating revenue recognition through 2026-2027.

-

AI Networking Silicon Dominance: Tomahawk 5 and next-generation switching platforms are experiencing unprecedented demand as AI cluster sizes scale exponentially, with Broadcom commanding 70%+ market share in hyperscale Ethernet switching.

-

VMware Integration Synergies: The $69 billion VMware acquisition is beginning to deliver cross-selling opportunities and operational efficiencies, with enterprise customers seeking integrated infrastructure and software solutions for hybrid cloud AI workloads.

Heavy dependence on a small group of hyperscaler customers, rising competition in custom silicon from players like Marvell, execution risk around VMware integration, and ongoing exposure to cyclical end markets that could weaken in a macro downturn.

Price Targets:

-

1 Month: $260-$275 (near-term consolidation; pre-earnings positioning)

-

6 Months: $310-$335 (AI backlog conversion accelerating; networking silicon strength)

-

1 Year: $360-$400+ (sustained hyperscaler AI buildout; VMware synergies materializing)

Broadcom represents the “safest” AI infrastructure play among our top picks, combining market leadership, diversified revenue streams, and strong balance sheet with compelling AI-driven growth visibility. The stock’s valuation—while not cheap—remains reasonable relative to sustained double-digit earnings growth expectations. Wall Street’s average price target of approximately 38% upside from current levels reflects confidence in Broadcom’s ability to capitalize on the multi-year AI infrastructure spending cycle while maintaining financial discipline and shareholder returns (dividends + buybacks).

Low-Cap Stock Opportunities: Undiscovered Value

The Small-Cap Setup: Rotation Continues Despite Near-Term Volatility

The Russell 2000’s extraordinary 14-day outperformance streak through mid-January—the longest since 1996—validated our previous edition’s thesis that small-cap rotation reflects structural revaluation rather than speculative excess. While the streak ended and small-caps pulled back slightly toward month-end, January’s approximately 5.3% gain significantly outpaced the S&P 500’s 1.5% advance, confirming institutional capital reallocation is underway.

Three critical factors support continued small-cap leadership:

-

Persistent Valuation Dislocation: Small-cap forward P/E ratios remain at approximately 30% discount to large-caps—near 25-year lows on a relative basis. This valuation gap exists despite improving small-cap earnings growth expectations, creating a classic mean-reversion setup.

-

Earnings Growth Inflection Sustained: For the fourth consecutive quarter, small-cap earnings growth is outpacing large-cap growth—a reversal of the 2021-2024 mega-cap concentration trend. Analysts forecast 13.5% small-cap earnings growth for 2026 versus 11% for large-caps, supported by strong macroeconomic backdrop (2-2.5% GDP growth expected).

-

Fed Rate Cut Optionality: While the January 28-29 FOMC meeting resulted in a hold at 3.5-3.75%, market expectations for two 25-basis-point cuts in 2026 (June and December) remain intact. Small-caps, with higher leverage and greater interest rate sensitivity, will benefit disproportionately from declining discount rates and improved credit availability.

The temporary momentum pause should be viewed as a healthy consolidation rather than trend reversal, creating selective entry opportunities in quality small-caps with genuine earnings catalysts and limited analyst coverage.

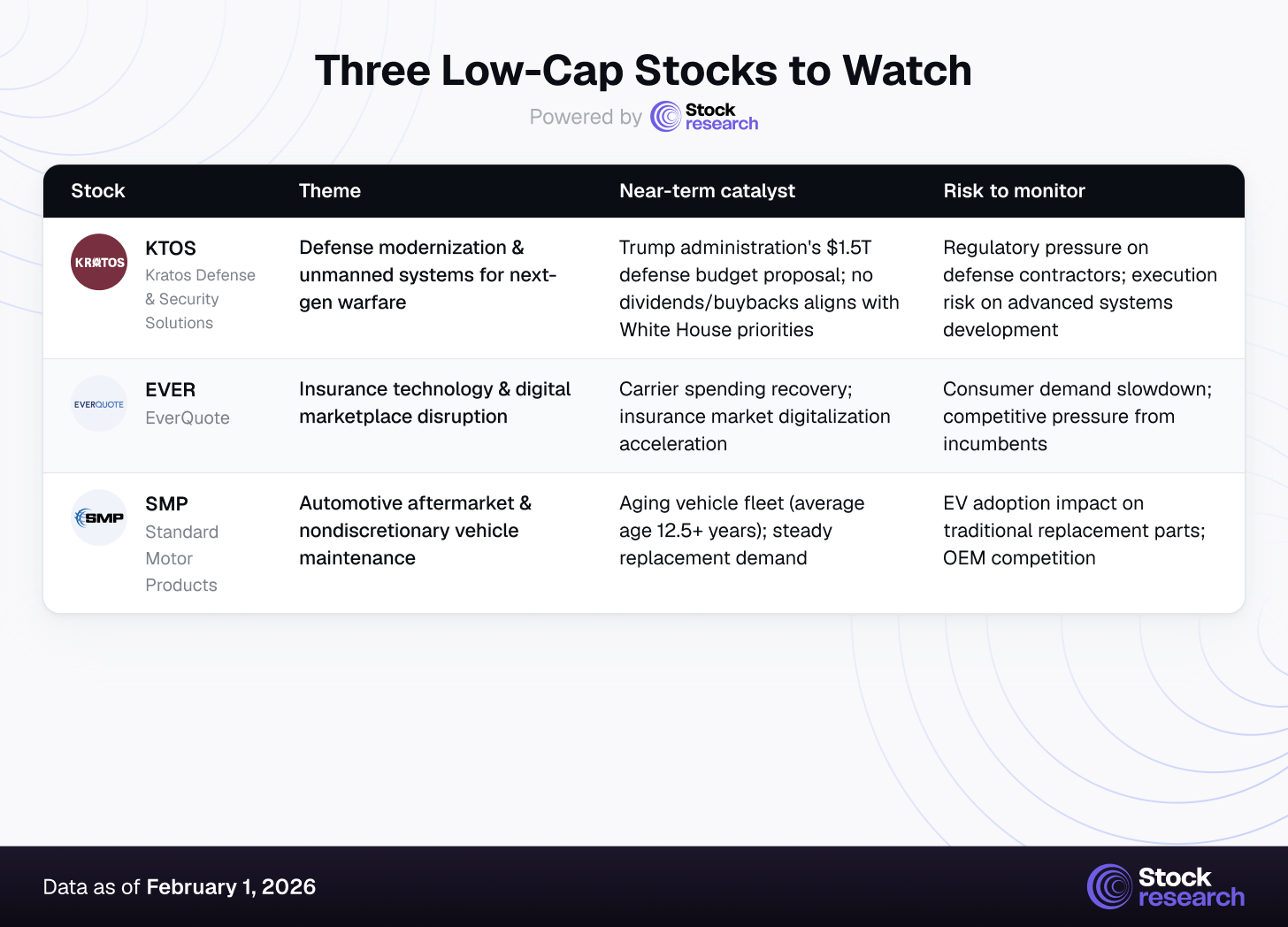

Three Low-Cap Stocks to Watch

-

Kratos Defense & Security Solutions (KTOS) | ~$3.7B

Defense contractor focused on unmanned systems, hypersonics, and space-based capabilities, uniquely aligned with Trump’s proposed $1.5T 2027 defense budget and modernization priorities.

Why it matters: Pure‑play exposure to next‑gen defense spending at a still-small scale versus legacy primes.

Key risks: Valuation after a 293% 1Y run, program execution and dependence on U.S. defense budgets. -

EverQuote (EVER) | ~$855M

Online insurance marketplace connecting consumers and carriers across auto, home, life, and health, positioned to benefit as carrier marketing budgets recover and distribution shifts to digital.

Why it matters: Capital‑light platform levered to long‑term insurance digitalization and higher-margin marketplace economics.

Key risks: Sensitivity to carrier ad budgets, intense competition from larger comparison sites and aggregators. -

Standard Motor Products (SMP) | ~$855M

Automotive aftermarket supplier of nondiscretionary replacement parts, supported by a record‑old U.S. vehicle fleet (12.5+ years) that drives steady repair demand.

Why it matters: Defensive small‑cap with recurring demand and reasonable valuation as small‑cap rotation continues.

Key risks: Faster‑than‑expected EV adoption, OEM competition, and raw‑material cost inflation pressuring margins.

Strategic Recap & Forward Outlook

-

Small-Cap Rotation Structurally Sound: Despite near-term momentum fatigue, the Russell 2000’s January outperformance reflects genuine institutional capital reallocation driven by valuation dislocations and earnings growth inflection. Quality small-caps with visible catalysts continue offering asymmetric upside.

-

AI Infrastructure Spending Remains Intact: Microsoft’s Azure slowdown notwithstanding, hyperscaler AI infrastructure commitments remain robust. Diversification strategies are creating opportunities for AMD, Marvell, and Broadcom as big tech reduces Nvidia concentration risk while expanding total AI spending.

-

Defense and Energy Sectors Offer Cyclical Hedge: Geopolitical tensions (Venezuela, Middle East) and Trump administration defense budget priorities ($1.5T proposal for 2027) are creating multi-year tailwinds for defense contractors and energy infrastructure providers—offering portfolio diversification away from tech concentration.

Forward Outlook (Week Ending February 8, 2026)

The coming week centers on earnings from Alphabet and Amazon alongside key data releases, including January employment and ISM services. Markets remain highly sensitive to tech guidance after Microsoft flagged slower Azure momentum, with any further signs of hyperscaler capex caution likely pressuring high-multiple software and cloud stocks. Strong results from Google Cloud and AWS would instead support the view that AI spending continues but shifts toward infrastructure, benefiting semiconductors over software.

Near-term direction hinges on whether Alphabet and Amazon confirm sustained AI infrastructure growth, whether labor data reinforces Fed rate cut expectations, and whether Congress avoids a government shutdown ahead of the March FOMC. Volatility remains elevated, but the medium-term backdrop stays constructive given resilient growth, earnings support, and policy flexibility.

Positioning favors balance, combining defensive quality with AI infrastructure exposure in names like AMD, Marvell, and Broadcom, while limiting exposure to stretched software valuations. Maintain selective allocations to quality financials such as Morgan Stanley, use volatility to add fundamentally strong small caps, and keep modest cash buffers to deploy on pullbacks.

Disclaimer

This analysis is for informational purposes only and should not be construed as investment advice. Equity markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.