StockResearch Intelligence Weekly #5

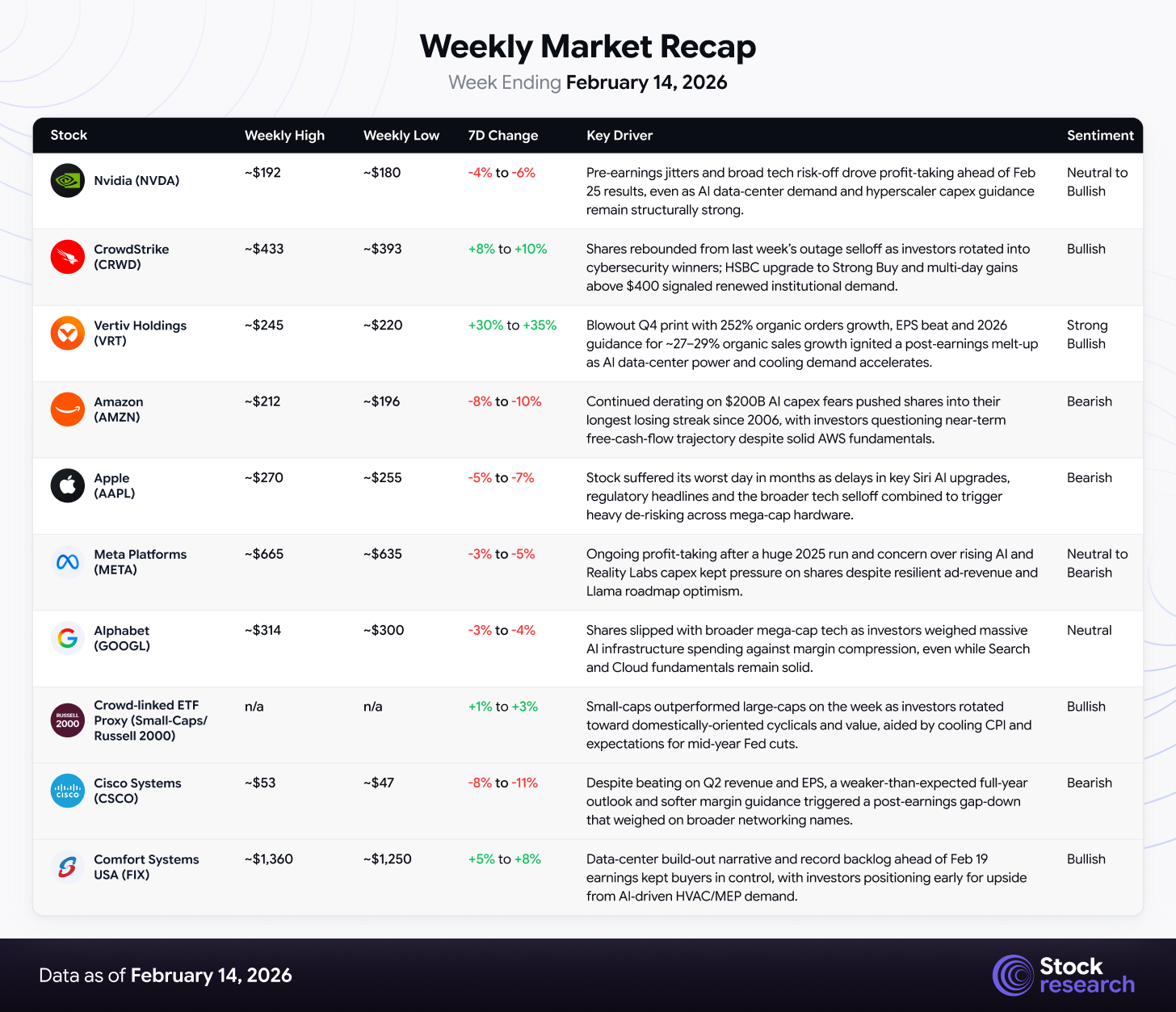

During February 10–14, 2026, U.S. equities posted their worst week since November as renewed AI disruption fears, now hitting wealth management and insurance, combined with weak corporate guidance to spark a sharp three-day selloff. The VIX jumped 18%. The S&P 500 fell 1.39% to 6,836.17, the Nasdaq dropped 2.10% to 22,546.67 on mega-cap tech weakness, and the Dow declined 1.23% to 49,500.93, cushioned by rotation into defensives.

Three catalysts drove the downturn: the “Altruist Event,” where Hazel AI triggered 7–9% plunges in Schwab, LPL, and Raymond James; a brutal Thursday selloff after Cisco’s guidance miss and Apple’s 5% slide; and softer January CPI that lifted June rate-cut odds to 83% but failed to restore risk appetite.

Amazon recorded its longest losing streak in nearly 20 years, wiping out about $463 billion in value amid backlash to its $200 billion 2026 AI capex plan. Meanwhile, small and mid caps outperformed, with the Russell 2000 up 1.2% Friday and the S&P MidCap 400 gaining 0.8%, continuing their year-to-date leadership.

Strengths

-

CPI Inflation Cools Below Expectations: The January CPI report showed headline inflation at 2.4% year-over-year (down from 2.7% in December) and core at 2.5%, both below consensus. Shelter costs — which account for over a third of CPI — rose just 0.2% monthly, their slowest pace in years. Futures markets now price an 83% probability of a Fed rate cut by June, providing crucial support for rate-sensitive sectors.

-

Small-Cap and Mid-Cap Outperformance Accelerating: The Russell 2000 and S&P Mid Cap 400 are now leading all major U.S. indices year-to-date at +6.6% and +7.8% respectively, compared to the S&P 500 at flat and the Nasdaq at -3.0%. The equal-weighted S&P 500 surged 1.0% on Friday while the cap-weighted version barely held positive, confirming that breadth is broadening away from mega-cap concentration.

-

Vertiv’s Record AI Data Center Earnings: Vertiv Holdings reported blockbuster Q4 results with organic orders growth of 252%, adjusted operating margin of 23.2% (up 170 bps YoY), and adjusted diluted EPS of $1.36 (up 37%). The company guided for 2026 net sales of $13.25–$13.75 billion (27–29% organic growth) and adjusted diluted EPS of $5.97–$6.07, confirming that physical AI infrastructure demand is accelerating far beyond software.

Weaknesses

-

“Altruist Event” Extends AI Disruption Beyond Software: Altruist’s Hazel AI platform demonstrated autonomous tax planning and financial document generation capabilities, triggering the largest single-day selloff in wealth management stocks since 2020. Charles Schwab fell 8.8%, LPL Financial dropped 8.3%, Raymond James lost 7%, and the contagion spread to European insurers within 24 hours. The Goldman Sachs Software Index (IGV) extended its decline, now down significantly from October 2025 highs.

-

Amazon’s Historic Nine-Day Losing Streak: Amazon shares closed at $198.79 on Friday, their lowest since May 2025, after falling for nine consecutive sessions — the longest such streak since July 2006. The selloff erased approximately $463 billion in market capitalization, driven by persistent investor anxiety over the company’s $200 billion 2026 AI capex commitment and its potential to push free cash flow negative.

-

Apple Suffers Worst Day Since April Tariff Shock: Apple shares tumbled 5% on Thursday alone, wiping out approximately $200 billion in market value, hit by a triple blow of delayed Siri AI features, an FTC warning letter, and the broader tech rout. The stock closed the week at $255.78, down 2.27% on Friday.

Market Recap

The week cemented a critical evolution in the AI disruption narrative: from “AI replaces software” to “AI replaces services.” While the prior week’s SaaS selloff was triggered by Anthropic’s Claude Cowork targeting enterprise software workflows, this week’s Altruist Event demonstrated that autonomous AI agents are now credibly threatening high-value human advisory services in finance, tax, and insurance — sectors that collectively represent trillions in market capitalization. This broadening of AI disruption targets, combined with persistent concerns over hyperscaler capex sustainability, created a “nowhere to hide” environment for growth investors that pushed the VIX above 20 and the CNN Fear & Greed Index firmly into Fear territory at 37.

Meanwhile, the physical infrastructure layer of the AI buildout continues to deliver exceptional results. Vertiv’s blowout quarter, AppLovin’s revenue beat (+66% YoY), and strong AI hyperscaler orders at Cisco all confirm that demand for hardware, cooling, power, and networking equipment remains structurally robust — even as the software and services layers face existential disruption questions.

Top 3 Stock Picks for Long-Term Investment

Powered by StockResearch AI

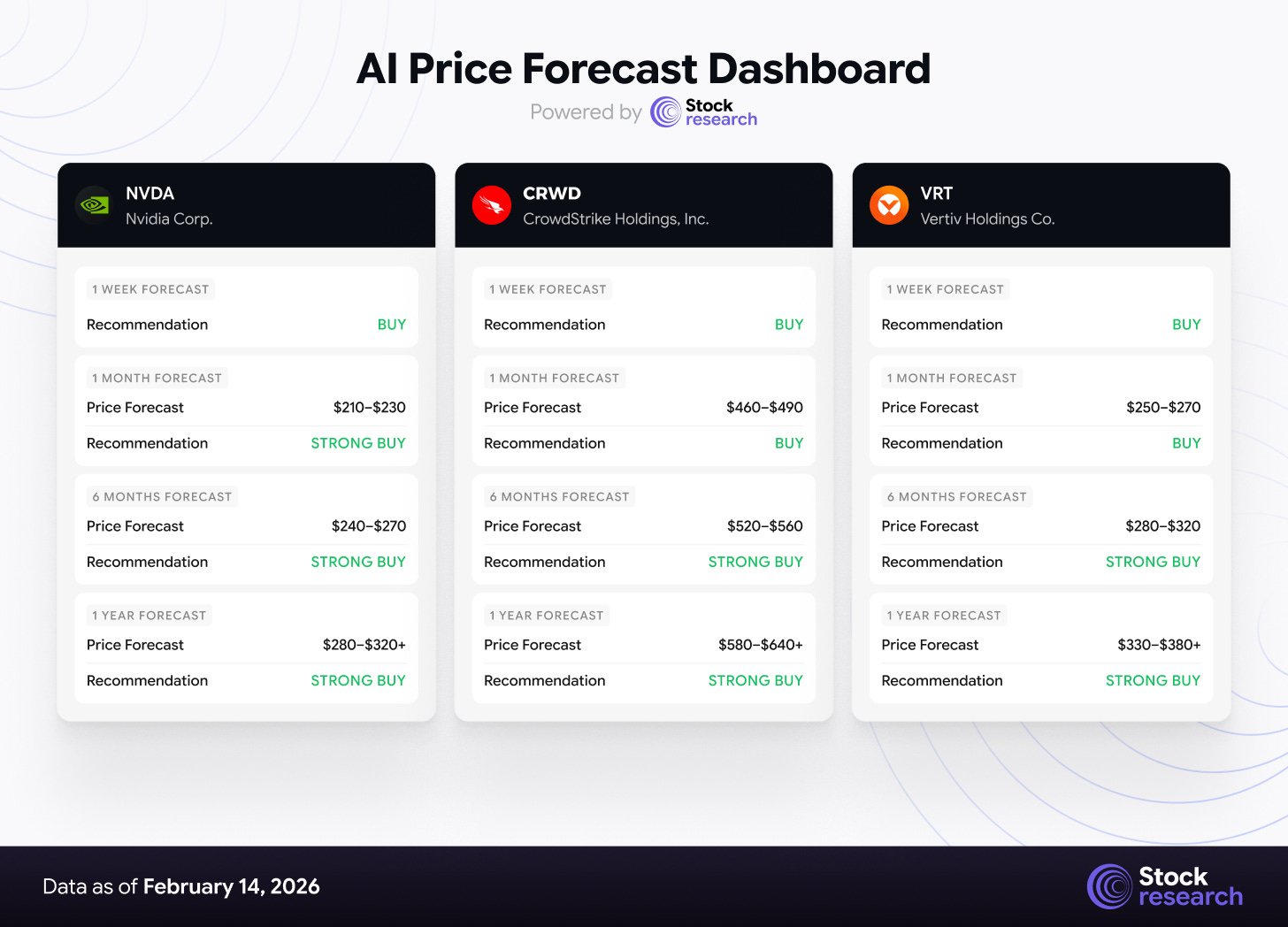

1. Nvidia (NVDA) | The Pre-Earnings AI Infrastructure Bellwether

Investment Horizon Recommendation:

-

1 Week: BUY (pre-earnings positioning ahead of Feb 25 Q4 FY2026 report; technical support holding at $180)

-

1 Month: STRONG BUY ($210–$230; earnings catalyst plus hyperscaler capex tailwinds)

-

6 Months: STRONG BUY ($240–$270; Blackwell/Rubin product cycle revenue conversion accelerating)

-

1 Year: STRONG BUY ($280–$320+; structural beneficiary of $600B+ annual hyperscaler AI spend)

Thesis: Nvidia enters its most consequential earnings week trading at $182.81 — down approximately 14% from its 52-week high of $212.19 and sitting near its 50-day moving average — creating one of the most compelling risk-reward setups of 2026. With over 90% of covering analysts maintaining positive ratings and an average price target of $250 (implying 36%+ upside), the stock is priced for pessimism while the fundamentals continue to accelerate.

UBS recently raised its price target to $245, estimating Q4 revenue approximately $2.5 billion above the company’s own guidance. Goldman Sachs maintains a $250 target, citing favorable supply-demand dynamics and the strong performance of new large language models trained on Nvidia’s Blackwell architecture. The most bullish estimate, from Evercore, reaches $352.

The February 25 earnings report will serve as a litmus test for the entire AI infrastructure thesis, with investors focused on Blackwell production ramp metrics, data center revenue trajectory, and forward guidance incorporating the $600 billion annual hyperscaler capex environment.

Catalysts:

-

Q4 FY2026 earnings report on February 25 — consensus expects significant beat-and-raise cycle

-

$500 billion revenue target for Blackwell and Rubin products through end of CY2026 reaffirmed

-

Hyperscaler AI capex commitments exceeding $500B in 2026 from Google, Amazon, Meta, and Microsoft

-

Next-generation Rubin architecture announcement expected at GTC 2026

Risks: Post-earnings “sell the news” reaction given elevated expectations; China export control escalation; potential margin compression from rising input costs (wafer, memory, packaging); competitive threats from custom ASICs at Google/Amazon reducing Nvidia GPU dependence; CEO Jensen Huang’s surprise cancellation of India AI summit appearance raises questions.

2. CrowdStrike Holdings (CRWD) | Cybersecurity’s AI-Proof Fortress

Investment Horizon Recommendation:

-

1 Week: BUY ($429.64 entry; HSBC upgrade to Strong Buy on Feb 13 provides near-term catalyst)

-

1 Month: BUY ($460–$490; defensive positioning as AI disruption fears drive security spending)

-

6 Months: STRONG BUY ($520–$560; Falcon platform consolidation gains; AI security market expansion)

-

1 Year: STRONG BUY ($580–$640+; Annual Recurring Revenue scaling toward $6B+)

Thesis: In a market environment where AI disruption is systematically destroying value across software, financial services, and insurance, CrowdStrike stands out as one of the rare companies that directly benefits from AI disruption rather than being threatened by it. Every new AI agent deployed — whether Anthropic’s Claude, Altruist’s Hazel, or any other autonomous system — dramatically expands the attack surface that needs to be protected, creating incremental demand for CrowdStrike’s Falcon platform.

The stock closed at $429.64 after receiving a significant upgrade from HSBC on February 13 (from Hold to Strong Buy with a $446 target), adding to the 41 analysts covering the stock with a consensus “Buy” rating and an average price target of $548.80 — implying 27.7% upside. Citizens maintains a $550 target citing CrowdStrike’s strategic acquisitions in identity governance and secure browsers, while BTIG has the highest Street target at $640.

CrowdStrike’s Q3 FY2026 results demonstrated 22% revenue growth to $1.23 billion with ARR reaching $4.92 billion. The company’s transition to a “hyperscaler of cybersecurity” through its unified Falcon platform creates powerful switching costs and cross-sell momentum — exactly the kind of deep platform moat that AI agents cannot easily disrupt.

Catalysts:

-

HSBC upgrade to Strong Buy signals broadening institutional conviction

-

AI security market expanding as every new AI agent deployment creates incremental endpoint security demand

-

Charlotte AI capabilities driving platform adoption and upsell

-

Q4 FY2026 earnings approaching — consensus expects continued 20%+ revenue growth

Risks: Premium valuation (trading above sector averages) leaves limited room for execution missteps; intense competition from Palo Alto Networks and SentinelOne; the July 2024 CrowdStrike outage still lingers as a reputational headwind; potential macro slowdown could pressure enterprise IT budgets.

3. Vertiv Holdings (VRT) | The Physical AI Infrastructure Powerhouse

Investment Horizon Recommendation:

-

1 Week: BUY ($234.53 post-earnings consolidation; strong support after 42% YTD rally)

-

1 Month: BUY ($250–$270; record backlog converting to revenue; Barclays Overweight rating)

-

6 Months: STRONG BUY ($280–$320; 2026 guidance of 27–29% organic growth executing)

-

1 Year: STRONG BUY ($330–$380+; structural beneficiary of multi-year data center buildout cycle)

Thesis: Vertiv is arguably the single best “physical layer” play on the AI infrastructure buildout, and its Q4 2025 earnings report validated the thesis emphatically. The company delivered organic orders growth of 252%, Q4 adjusted operating margin of 23.2% (up 170 bps YoY), and adjusted diluted EPS of $1.36 — beating guidance by $0.10. Full-year 2025 net sales reached $10.2 billion with 26% organic growth, while adjusted free cash flow surged 66% to $1.9 billion with a 115% conversion rate.

The 2026 guidance is where the story truly accelerates: Vertiv projects net sales of $13.25–$13.75 billion (27–29% organic growth), adjusted diluted EPS of $5.97–$6.07 (43% growth at midpoint), and adjusted free cash flow of $2.2 billion. With AI-specific data center clusters now requiring 120–150kW per rack (versus 10–15kW just three years ago), the demand for Vertiv’s power, cooling, and thermal management solutions is structurally accelerating.

The stock has rallied 42% year-to-date but still trades approximately 8.5% below the consensus analyst target of $256.41. The Barclays upgrade to Overweight specifically cited Vertiv’s “beat-and-raise” potential and its 80% revenue exposure to data centers. With net leverage at just 0.5x, the balance sheet provides significant optionality for capacity expansion and strategic acquisitions.

Catalysts:

-

Record backlog converting to production revenue throughout 2026–2027

-

Americas segment growing 46% organically — the highest-margin geography

-

Liquid cooling and AI-specific thermal solutions commanding premium pricing

-

Capacity expansion through new facilities to meet surging demand

Risks: Premium valuation (P/E ~67x trailing) leaves the stock vulnerable to any demand deceleration; execution risk on capacity expansion and potential supply chain bottlenecks; concentration risk around hyperscaler customers; EMEA weakness (down 14% in Q4) could persist if European data center buildout lags expectations.

Low-Cap Stock Opportunities: Undiscovered Value

The AI Infrastructure & Defense Rotation: Finding Alpha Beyond Mega-Cap Tech

This week’s extension of the AI disruption narrative — from enterprise software to financial services — has further accelerated the institutional rotation into companies with physical-world moats, defense exposure, and infrastructure-critical positioning. The Russell 2000’s 1.2% Friday outperformance and the S&P Mid Cap 400’s year-to-date leadership (+7.8%) confirm that capital is systematically flowing into domestically-focused companies trading at significant valuation discounts to mega-cap tech.

Three structural factors support selective positioning in smaller-cap names:

-

AI Disruption Is a Tailwind for Physical Infrastructure: While software and services companies face existential questions, companies that build, cool, power, and defend AI infrastructure are experiencing record demand. The physical layer cannot be disrupted by AI agents — it enables them.

-

Defense Budget Expansion Accelerating: The Pentagon’s 2026 budget request for drones and counter-drones is 53% higher than fiscal 2024 actual spending and 78% above fiscal 2025 funding, creating a structural multi-year demand cycle for defense technology companies.

-

Valuation Gap at Historical Extremes: Small-cap stocks trade at a 31% valuation discount to large caps, with Russell 2000 earnings projected to grow 35% annually through 2027 — more than double the S&P 500’s projected 14% growth. JPMorgan’s Eduardo Lecubarri calls this “the best stockpicking era we have seen in our lifetime”.

Three Low-Cap Stocks to Watch

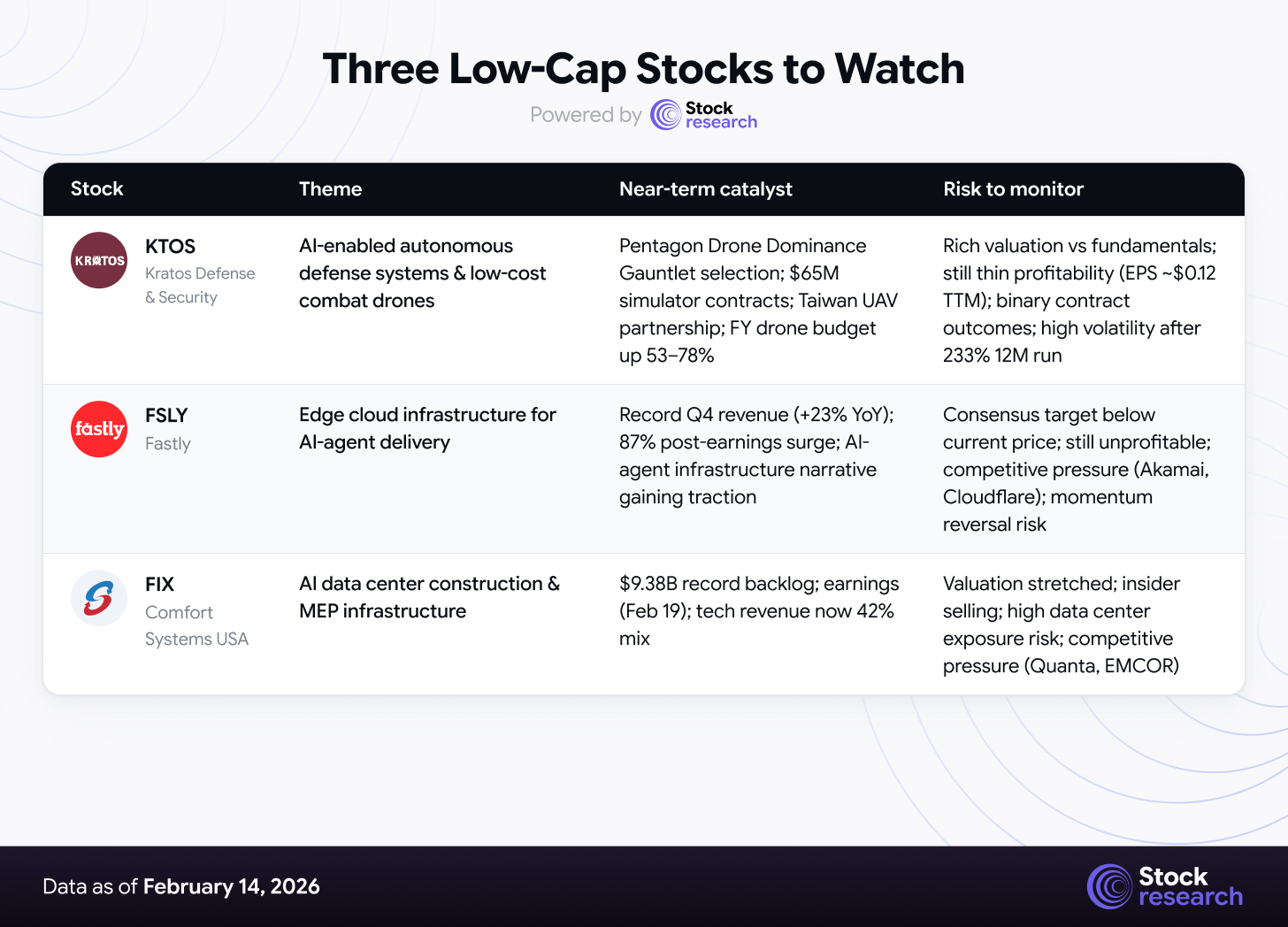

1. Kratos Defense & Security Solutions (KTOS) | ~$15B Market Cap

Defense technology company specializing in high-performance unmanned aerial systems, AI-powered military drones, and satellite communications. Kratos was selected for Phase 1 of the Pentagon’s Drone Dominance Gauntlet in February 2026 and secured approximately $65 million in new training simulator contracts alongside a breakthrough Taiwan UAV partnership with NCSIST.

Why it matters: Kratos is uniquely positioned at the intersection of two of the most powerful defense investment themes: low-cost attritable drones and AI-enabled autonomous warfare. Its flagship XQ-58 Valkyrie platform is central to Pentagon demonstrations of affordable jet-powered unmanned combat aircraft, and selection for the Drone Dominance Gauntlet puts Kratos in direct competition for prototype delivery contracts worth potentially billions. With the Pentagon’s drone budget surging 53–78% above prior fiscal year spending, Kratos’ pipeline visibility is expanding rapidly.

The stock closed at $89.06 on February 13, down 5.67% for the week amid broader market selling, but up 233% over the past 12 months. The average analyst target of $101.43 implies approximately 14% upside, with B. Riley Securities upgrading to Buy in December 2025.

Key risks: Still essentially unprofitable at scale (EPS of $0.12 TTM); Morningstar fair value estimate of $19.68 suggests extreme premium pricing relative to current fundamentals; Drone Dominance Gauntlet is a competition with binary outcomes; market cap of $15B is large relative to current revenues, creating significant downside risk if drone program wins fail to materialize.

2. Fastly (FSLY) | ~$2.7B Market Cap

Edge cloud computing and content delivery platform that surged 87% in a single session on February 12 after reporting record Q4 revenue of $172.6 million, representing 23% year-over-year growth. The company’s edge computing infrastructure serves as the delivery backbone for AI-powered applications, positioning it as an unexpected beneficiary of the AI-agent proliferation wave.

Why it matters: While the market has been laser-focused on AI disruption destroying value in traditional software, Fastly represents the infrastructure layer that actually delivers AI-generated content to end users. Every autonomous AI agent — whether handling tax planning, customer service, or enterprise workflows — requires low-latency edge computing to function effectively at scale. As AI agents proliferate, the demand for Fastly’s edge delivery, security, and compute services scales proportionally.

The stock’s explosive 87% single-day move to $18.26 reflects a dramatic sentiment shift, as the record revenue quarter validated that Fastly’s turnaround strategy is gaining traction. With a market cap of approximately $2.7 billion and accelerating revenue growth, Fastly represents a speculative but potentially high-reward play on the physical delivery infrastructure required by AI-agent ecosystems.

Key risks: The analyst consensus remains “Hold” with an average price target of $11.17 — suggesting significant overvaluation at current levels following the explosive move. The company has a history of volatile price action and missed expectations. Profitability remains elusive, and competition from Akamai and Cloudflare is intense. The post-earnings surge could reverse sharply if follow-through buying does not materialize.

3. Comfort Systems USA (FIX) | ~$47B Market Cap

Leading specialty contractor for HVAC and MEP (mechanical, electrical, plumbing) systems, with a rapidly growing focus on AI data center construction. The company’s record backlog of $9.38 billion is being driven primarily by technology sector projects, which now constitute approximately 42% of total revenue — up from 32% just one year ago.

Why it matters: Comfort Systems represents the ultimate “picks and shovels” play on the physical AI data center buildout. While Nvidia provides the GPUs and Vertiv provides the power and cooling equipment, Comfort Systems provides the specialized craft labor and installation services required to actually build these facilities. The company’s Kodiak division (a traveling craft labor agency) has roughly doubled headcount in the past year, and its modular construction capabilities (15–20% of revenue) offer speed and flexibility that hyperscaler customers demand.

The stock closed at $1,337.95 on February 13, with Q4 and full-year 2025 earnings scheduled for February 19, 2026 — a near-term catalyst that could validate continued backlog conversion. The consensus rating is “Strong Buy” with a target of $1,178.67, though Stifel has a significantly higher target of $1,155 (note: the stock has already exceeded most analyst targets, reflecting the pace of the AI data center demand surge).

Key risks: Market cap of $47 billion is large for this section and pricing already reflects significant AI data center optimism. Aggressive insider selling by senior executives raises questions about valuation sustainability. Heavy revenue concentration in technology/data center projects (42%) creates vulnerability if the buildout cycle moderates. Competition from Quanta Services and EMCOR is intensifying in the data center construction space.

Strategic Recap & Forward Outlook

-

AI Disruption Has Gone Multi-Sector — and the Market Isn’t Done Repricing: The progression from Anthropic disrupting SaaS (Week 4) to Altruist disrupting wealth management and insurance (Week 5) demonstrates that autonomous AI agents are systematically working through every high-fee, human-advisory service category. Expect additional disruption catalysts targeting legal, consulting, real estate brokerage, and healthcare administration in coming weeks. Each event will trigger sector-specific selloffs and reinforce the rotation toward companies with physical-world moats.

-

CPI Relief Is Necessary but Not Sufficient: The softer-than-expected January inflation data provides important macro support — bringing rate-cut expectations forward and reducing the probability of a Fed policy surprise. However, the market’s muted reaction to the CPI print on Friday confirms that macro tailwinds alone cannot overcome the structural anxieties around AI disruption and hyperscaler capex sustainability. The February 20 PCE report will be the next critical inflation datapoint.

-

Nvidia’s February 25 Earnings Will Set the Tone for Q1: The most important single event for the U.S. equity market in the near term is Nvidia’s Q4 FY2026 earnings report. A strong beat-and-raise could reignite risk appetite across the entire AI infrastructure complex, while any sign of demand deceleration or margin compression would amplify the current defensive rotation. UBS projects revenue approximately $2.5 billion above Nvidia’s own guidance, setting the bar extremely high.

Forward Outlook (Week Ending February 21, 2026)

Markets are closed Monday, February 17 for Washington’s Birthday, providing a shortened four-day trading week. The earnings calendar remains dense, with Comfort Systems USA (Feb 19), Walmart, and several other names reporting. The February 20 PCE inflation report will be closely watched as the Fed’s preferred inflation gauge, potentially reinforcing or challenging the dovish narrative established by the CPI report.

Near-term direction hinges on three variables: whether the VIX can retreat from the 20+ level that has signaled elevated institutional hedging activity; whether the small-cap and mid-cap outperformance trend sustains as a durable rotation rather than a fleeting safety trade; and whether pre-Nvidia earnings positioning drives a rebound in semiconductor names or further selling pressure as expectations build. Sentiment remains firmly in “Fear” territory (CNN Fear & Greed Index at 37), but this level has historically coincided with tactical buying opportunities in fundamentally strong names.

Positioning favors AI infrastructure hardware and physical-layer providers (NVDA, VRT, AVGO) over software and services companies facing AI substitution risk; cybersecurity leaders (CRWD, PANW) that benefit from expanding attack surfaces; defensive sectors and quality cyclicals benefiting from the rotation away from mega-cap tech; and selectively undervalued small/mid-cap names in defense, energy infrastructure, and data center construction. Maintain elevated cash buffers to deploy ahead of Nvidia’s February 25 earnings and into any further AI disruption-driven dislocations.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Stock markets carry substantial risk, including the potential loss of principal. Past performance does not guarantee future results. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions.